The billion-dollar club: Asia's tech unicorns

Asia accounts for one fifth of the global tech sector’s unicorn population as companies raise larger rounds at ever higher valuations. But as investor sentiment weakens, some of these behemoths should be concerned

Don't fancy cooking? Shaoshaofan will send a chef to your home who will serve up a meal for you. This was how the Chinese online-to-offline (O2O) start-up positioned itself when opening for business last year. Within a few months, the company claimed to have more than 200,000 users and over seven million chefs registered on its platform. IDG Capital Partners and Shunwei Capital Partners duly invested.

Last week Shaofanfan closed down. "After 11 months, regrettably we haven't figured out a sustainable business model," Zhijian Zhang, the company's founder, said in a WeChat message to users. "We tried to separate ourselves from all the craziness in the industry over internet-plus and O2O, and focus on what we really wanted to do. But the private chef model is just so inefficient."

One of several private chef platforms to receive VC backing, Shaofanfan failed to gain traction in a competitive market despite altering its strategy several times, one investor says.

A few weeks earlier, Meituan, a leading O2O services player with five years of history and millions in private funding behind it, experienced its own wobble. The company approached investors about raising more capital at a higher valuation but the response was lukewarm. This triggered a flurry of negotiations and Meituan announced a merger with rival platform Dianping, in the expectation that investors will look more favorably on an outright market leader.

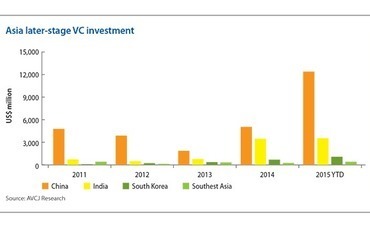

Two companies of contrasting size and two very different outcomes, but a common driving factor: weaker sentiment in the tech space in China, and every chance that it will spread to India and Southeast Asia as well. For the unicorns in these markets - companies like Meituan that have valuations of $1 billion or more - once solid prospects now appear less certain. Investors are beginning to ask when, and how, they are going to get their money back.

"The VC market has cooled compared to earlier in the year. Some later-stage financing is taking longer and some companies are adjusting their valuations," says James Mi, co-founder at Lightspeed China. "Companies that are consuming a lot of money are under much more pressure. Instead of burning cash, they need to figure out how to grow their businesses on a limited capital basis."

Myth to reality

The term of unicorn emerged in the US about three years ago. They were a rare species to begin with but have grown in number as companies in the past 18 months. According to CB Insights data, there are currently 140 unicorns globally with a total accumulative valuation of $506 million, although given the nature of private markets this could be a low estimate.

Asia is home to 32 unicorns worth a combined $132 billion, having raised more than $18 billion. Chinese smart phone brand Xiaomi leads the way, occupying second place in the global rankings with a purported worth of $46 billion, just behind Uber on $51 billion. These companies are largely concentrated in O2O services, e-commerce, financial technology and hardware. China has 21 unicorns and at least one representative in each category, while India has seven, mostly in e-commerce and O2O services. South Korea and Southeast Asia have two unicorns apiece.

The e-commerce space is packed with companies looking to emulate the success of China's Alibaba Group and JD.com, both of which went public in the US last year. India's Flipkart and Snapdeal and South Korea's Coupang sit near the top of the valuation rankings. Ride-hailing platforms are represented by Didi Kuaidi, Ola and GrabTaxi, from China, India and Southeast Asia, respectively, while China alone boasts several lifestyle-oriented local services unicorns, led by Meituan and Dianping.

Sectors such as healthcare and financial technology - rich unicorn territory in the US - are also getting traction in China. Ant Financial, Alibaba's online finance affiliate, is said to be valued at more than $40 billion, although it is missing from the CB Insights rankings. There are places for peer-to-peer (P2P) lending platform Lufax and healthcare information portal Guahao.

These valuations are more about projection than reality: investors calculate an expected market size for a particular vertical and attribute valuations to companies based on their market share, even though in most cases the capital being raised goes towards subsidies used to attract customers and maintain or increase market share. As such, several companies are not only valued in excess of $1 billion, but have also raised more than $1 billion in fresh capital. So what does it actually mean to be a unicorn?

"Unicorn status is less meaningful than a couple years ago. In the past when you had valuation of more than $1 billion in theory this meant you were safe - no one could beat you. Now I don't think being a unicorn is enough to ensure a successful IPO. We will see unicorns die. Right now there are a lot of inflated unicorns because of the valuation bubble," says David Wei, co-founder of Vision Knight Capital.

Competitive spirit

The first generation of Chinese internet giants - Baidu, Alibaba and Tencent Holdings (the BAT) - has contributed to the current state of affairs. Keen to differentiate their business models or at least create traction for their ecosystems, these companies used capital to secure strategic alignments in each new vertical.

Prior to their merger earlier this year, Kuaidi Dache was backed by Alibaba while Didi Dache counted Tencent among its investors. Passengers could make payments through Alipay or Tenpay and enjoy free rides if they used Alipay or WeChat. Similar synergies were behind Alibaba and Tecent's decision to support Meituan and Dianping, respectively. The O2O services players were encouraged to broaden their scope and compete for business not only in group buying but in a host of other segments as well.

Other verticals such as mobile healthcare platforms that connect doctors and patients appear to be following suit. Tencent invested $394 million in that Guahao and industry peers including Spring Rain and Xingren responded by raising large rounds from the likes of FountainVest Partners and Yunfeng Capital, which was co-founded by Jack Ma, executive chairman of Alibaba. The proceeds are being used to wage a marketing war.

"We are seeing unicorns in our space. A lot of people are putting in money to provide subsidies and accumulate market share. Some companies offer free consultations, even though they don't have enough doctors; and others are paying doctors RMB50-100 ($8-15) a time to download apps. We're the only start-up not giving money away because it isn't going to work," says Martin Shen, founder and CEO of Xingren. "Patients recover and will leave the platform, and subsidies don't work with doctors as they are highly skilled professionals."

This competitive dynamic is a product relentless ambition. Every founder envisages becoming the dominant player in his space and potential long-term pay-off is so great they are willing to whatever it takes to maximize their chances of success. "A lot of these founders think several years ahead and ask ‘What must I do to become a significant player?' They are willing to sacrifice profits today for a bigger market share and profitability in the future," says John Lindfors, managing partner at DST Global.

Subsidies are therefore seen as a necessary part of the expansion phase. The company builds market share, gets users comfortable with its service, and then weans them off the subsidies. It is hoped that customers will have developed sufficient loyalty to the platform that they are willing to pay a higher take rate.

Not all investors are happy with this approach. "We're hyper-aware of cash burn and any company that has an asymmetry in cash burn I walk away from. It is very important they maintain a low cost burn and have at least a 3-5 year horizon in terms of cash on hand to run with before doing another raise," says Ozi Amanat, founder of K2 Global, which makes pre-IPO investments in technology companies.

In the US, Top Tier Capital Partners currently has more than 50 unicorns in its portfolio and another 40 publicly-listed companies worth over $1 billion in which its portfolio VC funds still hold shares. The fund-of-funds only tracks the top 1% of these unicorns for which the average valuation is $6.3 billion.

Top Tier's findings indicate that these companies are generating average revenue of around $500 million and seeing year-on-year growth of 142%. These revenue numbers are a source of comfort: though valuations are high, the companies' performance suggests they are not inflated.

"Our biggest concern is the motivation for these unicorns to go public is small," says Jessica Archibald, managing director at Top Tier. "There have been several ‘private IPO' financing rounds by large mutual funds and hedge funds, but that does not necessarily solve the problem for venture capitalists. These ‘private IPOs' are more of an exit risk for VCs than an opportunity, but it is too early to call it a real concern."

The recent experiences of US-based document-sharing software provider Dropbox illustrate the difficulties that arise when private market valuations become unjustifiably high. Dropbox raised a $350 million Series C round last year at a valuation of $10 billion. However, industry peer Box then went public at a valuation $1.6 billion, despite its revenues being no more than 50% lower than those of Dropbox. Investment bankers told the company it would struggle to hit a $10 billion valuation on IPO.

BlackRock and other investors wrote down the value of the asset on their books, reportedly to around $6-7 billion, and Dropbox shelved the IPO plan. According to PitchBook, US companies are now waiting a median of 7.7 years to go public, up from 5.8 years in 2011.

The classic example of a successful Asian unicorn IPO is JD.com - it went public at a valuation of $26 billion and now trades at close to $40 billion, representing significant upside for even the later-stage investors. But the private market valuations commanded by arguably less impressive companies, coupled with questions as to how many Chinese unicorns US markets can accommodate, is giving pause for thought.

Dianping was preparing for an A-share listing earlier this year before public markets crashed, the offering was postponed, and the Meituan merger was agreed. The combined entity is said to be looking to raise capital at a valuation of $17 billion - more than the two companies were worth as independents - but would the public markets value it so highly?

"Dianping probably does over RMB2-5 billion a month in transaction value, while Meituan has about RMB 5-6 billion. That is more than RMB10 billion worth of transactions in one month," says J.P. Gan, managing partner at Qiming Venture Partners and an investor in Dianping. "Commissions are 5-10% so the company is generating around $500 million in annual income and growing 30-50% year-on-year. Why don't you think they can't be worth billions of dollars?"

The merger of Dianping and Meituan is a cost-saving exercise. They will no longer pump capital into subsidies intended to win market share off each other, and as the single dominant player in the market, there are no other rivals. The earlier merger of Didi Dache and Kuaidi Dache served a similar purpose and the now-combined entity has ended subsidies and is looking to create a pricing system based on data generated before the relentless undercutting set in.

"They are making money from premium car services and there is still a lot they can do to improve service quality. It's like Alibaba, which took 14 years to go IPO. The need for Didi Kuaidi to list isn't as high as before, because there is a private market for them to raise money," says Jixun Foo, a managing partner at GGV Capital. "Third, there is liquidity. If I wanted to sell my stake in Didi Kuaidi today, there will be people who want to buy in the private market."

Winners and losers

The mergers also reflect an acceptance on the part of Alibaba and Tencent that the market opportunity is best addressed through collaboration rather than cutthroat competition. Investors may to participate for longer than originally envisaged - and perhaps invest more as the company continues to expand - but it is expected to deliver economic sustainability.

However, it is unlikely to work out well for everyone. Industry participants point to earlier developments in the e-commerce space. More than 1,000 companies have raised capital over the last 10 years but only a handful has achieved significant size - the hit ratio is said to be 5%.

"Everyone has to figure out how to build a sustainable business model. When the investing environment changes those that are slowest in finding an answer are the first go," says James Lu, a partner at law firm Cooley. "You have already seen a lot of the companies start to have operational issues, because their overhead is so big, and the competition is so fierce."

One more recent development in the market is a growth in M&A activity and it is inevitable that larger players will pick of their weaker counterparts. These moves will also support continued expansion into new growth areas, as already evidenced in the strategies of Baidu, Alibaba and Tencent. Increasingly, this is likely to see Chinese companies establish footholds in other emerging markets.

Similar patterns are emerging in Southeast Asia and India. GrabTaxi and Ola have both launched delivery services, while Snapdeal and Flipkart are also making tech investments. These companies are not as acquisitive as their Chinese peers and reasons are given for this: the logistical and cultural challenges presented by Southeast Asia's multiple markets are a hindrance to expansion; and in India the middle class is still comparatively small. At the same time, the unicorns in these markets are simply younger than the Chinese.

"In India, it may be too early to say, because none of the truly large internet companies in this cycle have gone through exits. My sense is, once some of the largest unicorns have go through this, it will have an impact on downstream funding for the next batch. I think over the next 18-24 months there will be exits, at least for the largest companies," says Gourav Bhattacharya, vice president at Matrix Partners India.

If valuations cool as many industry participants expect, there will be more casualties like Shaofanfan in China. Some unicorns may also run into difficulty, particularly if they have not been able to use their funding to establish leadership positions.

"Category leaders will always find it is possible to raise funds at a certain valuation. If you aren't one of the superstar companies, it is a lot more difficult to raise money in a challenging market," says DST's Lindfors. "That's what happens when a market is hot - a rising tide lifts all boats. When the markets face a tough time, investors will be more selective."

SIDEBAR: The unicorns

There are 140 tech start-ups globally currently valued at $1 billion or more, according to CB Insights. These are Asia's 32 (although there could be quite a few more)...

Xiaomi

China

Valuation (US$b): 46.0

Total funding (US$m): 1,540

Consumer electronics

Flipkart

India

Valuation (US$b): 15.0

Total funding (US$m): 3,150

Online marketplace

Didi Kuaidi

China

Valuation (US$b): 15.0

Total funding (US$m): 4,420

Car-hailing apps

Lufax

China

Valuation (US$b): 10.0

Total funding (US$m): 483

Online P2P lending

DJI

China

Valuation (US$b): 10.0

Total funding (US$m): 105

Consumer drones

Meituan

China

Valuation (US$b): 7.0

Total funding (US$m): 1,070

O2O services

Coupang

South Korea

Valuation (US$b): 5.0

Total funding (US$m): 1,420

Online marketplace

Dianping

China

Valuation (US$b): 4.1

Total funding (US$m): 1,440

O2O services

Paytm

India

Valuation (US$b): 3.4

Total funding (US$m): 1,270

Online payment

Atlassian

Australia

Valuation (US$b): 3.3

Total funding (US$m): 210

Security software

Ele.me

China

Valuation (US$b): 3.0

Total funding (US$m): 1,090

O2O services

Snapdeal

India

Valuation (US$b): 2.5

Total funding (US$m): 1,540

Online marketplace

Olacabs

India

Valuation (US$b): 2.4

Total funding (US$m): 905

Car-hailing apps

GrabTaxi

Southeast Asia

Valuation (US$b): 1.8

Total funding (US$m): 690

Car-hailing apps

Ucar

China

Valuation (US$b): 1.8

Total funding (US$m): 800

Car-hailing service

Lakala

China

Valuation (US$b): 1.6

Total funding (US$m): 274

Online payment & services

Mu Sigma

India

Valuation (US$b): 1.5

Total funding (US$m): 178

Data analytics

Guahao

China

Valuation (US$b): 1.5

Total funding (US$m): 516

Online healthcare

Koudai

China

Valuation (US$b): 1.4

Total funding (US$m): 362

Online marketplace

Lazada

Southeast Asia

Valuation (US$b): 1.3

Total funding (US$m): 735

Online marketplace

Tujia

China

Valuation (US$b): 1.0

Total funding (US$m): 464

Online vacation rentals

Quikr

India

Valuation (US$b): 1.0

Total funding (US$m): 350

Online classifieds

Zomato

India

Valuation (US$b): 1.0

Total funding (US$m): 223

Online restaurant listings

InMobi

Southeast Asia

Valuation (US$b): 1.0

Total funding (US$m): 221

Mobile advertising

Yello Mobile

South Korea

Valuation (US$b): 1.0

Total funding (US$m): 129

Mobile services

Apus Group

China

Valuation (US$b): 1.0

Total funding (US$m): 116

App developer

Fanli

China

Valuation (US$b): 1.0

Total funding (US$m): 130

Online marketplace

Mogujie

China

Valuation (US$b): 1.0

Total funding (US$m): 230

Social commerce

Beibei

China

Valuation (US$b): 1.0

Total funding (US$m): 134

Online marketplace

Panshi

China

Valuation (US$b): 1.0

Total funding (US$m): 220

Mobile advertising

Aiwujiwu

China

Valuation (US$b): 1.0

Total funding (US$m): 200

Online property listings

China Rapid Finance

China

Valuation (US$b): 1.0

Total funding (US$m): 56

Online P2P lending

More on Technology

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.