Asia distress: Landslides on hold?

Investors are witnessing an uptick in turnaround opportunities based on delayed pandemic effects and a poor macro outlook. The trend remains anecdotal, but some markets could see a surge

In most of Australia, pandemic-shuttered schools didn't return to normal until the first quarter of 2022. Ostensibly, this was a time of recovery and momentum for companies such as afterschool care provider Camp Australia. But navigating industry disruption at this scale isn't child's play.

Camp Australia enjoyed leniency from banks during the darkest days of COVID-19. The company, still reeling from the lockdowns, held a significant amount of debt when interest rates began to rise from a record low base last year. Some lenders wanted to repatriate capital back to their home markets, while others simply lost patience. Both groups decided to trade their debt.

Last November, local turnaround specialist Allegro Funds led several investors in a restructuring process that saw nine out of 11 debt holders sell their positions in Camp Australia. The deal also facilitated an exit for Bain Capital, the owner since late 2016. Allegro, which first backed the company in late 2021, is now the largest shareholder and debtholder.

Johan Krynauw, a managing director at Allegro, sees the transaction as signaling a post-pandemic inflection point for turnaround opportunities. It marks a moment when, for the first time in a decade, there is widespread activity in trading company debt. As of mid-2022, lenders have had to make decisions about companies emerging from COVID-19 limbo, and conservative instincts are often winning.

"The banks were fantastic in the way they behaved [during the pandemic], but as things started to recover with a healthier M&A environment and interest rates ticking up, you could see which companies had the right cap structure and which didn't," Krynauw said.

"Where companies are too over-geared, lenders have to ask what the debt is worth in this market with a deteriorating macro outlook. Do they take a certain outcome now or try to recover a better but more uncertain outcome down the line? That's a trade-off they're looking at."

Macro to micro

Australia has its own nuances in this theme, including a cashed-up consumer base, skills shortages, and supply chain disruptions – the latter two exacerbated by border closures. But much of the perceived post-pandemic special situations opportunity suggested by Camp Australia is based on more universal factors.

Reduced government stimulus and less leniency from lenders amidst rising interest rates and stubbornly high inflation have proven a feature across developed and developing markets. This has put pressure on discretionary consumption and the budgets of indebted companies.

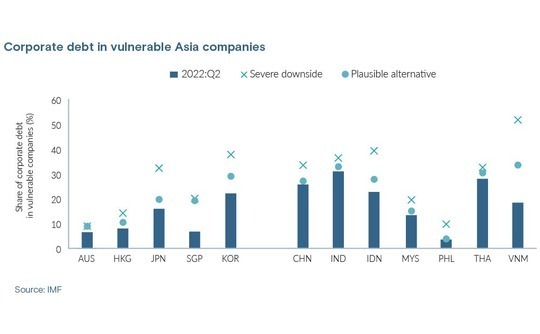

The percentage of overall corporate debt held by companies deemed as having low ability to service debt was more than 20% in Korea, China, India, and Indonesia as of mid-2022, according to the International Monetary Fund (IMF).

In Singapore, that figure was just under 10% but at risk of doubling even in a scenario of moderate additional credit tightening. In Korea and Indonesia, up to 40% of corporate debt could be in the hands of vulnerable companies if a severe credit crunch materialises. In Vietnam, it could hit 50%.

The most at-risk sub-segments are said to be those that experienced a pandemic bounce, such as pet food and pet care. Much depends on local market dynamics, however. In Korea, Jason Shin, a managing partner at VIG Partners, sees dining and travel as recovering strongly, although cosmetics is languishing, and theoretically recovering cinemas are under pressure from streaming services.

"We have to have conviction that the industry is rebounding and that the factors dragging down the target company are mostly solvable along with such industry rebound," Shin said.

"Now with COVID out of the way, with our injection of capital and the right management, will it turn around or are there other macro factors dragging it down that we didn't think of? That's the number one thing to keep in mind in these situations. Our due diligence on that has to be airtight."

VIG is emblematic of the idea that turnaround opportunities are expanding for non-turnaround specialists that have nevertheless found inroads to participate. In January, the firm acquired Korean low-cost airline Eastar Jet for USD 117m, predicting the company would gain market share as the industry consolidates and passenger volumes return to pre-pandemic levels.

Chinese nuances

Shin cautions that, due to hidden business liabilities and macro factors complicating post-pandemic recoveries, openings in this vein are not as common as they appear. This may be true nowhere more than in China, where consumer and internet businesses are experiencing corrected valuations but have not emerged as a significant – or at least widely accessible – distress investment opportunity.

Victor Jong, PwC's Greater China restructuring and insolvency leader, describes a landscape where high-profile distress in real estate permeates the broader economy but does not poison it. He sees the current restructuring activity in China as tidying up from the last major credit expansion. With no new credit expansion on the horizon, the expected wave of distress situations may never come.

"There are fears that the economy will further weaken, affecting small-scale developers, but we don't expect that at the moment because those companies' balance sheets are still quite strong," Jong said.

"There might be some mom-and-pop businesses or chains that get a bit more distress, but not to the extent that people have projected. Geopolitics has some impact, but that has stabilised a bit, with some investment flowing back into the mainland and Hong Kong."

Additional government stimulus is the most likely driver of another credit expansion in China, but this is not expected. Still, there will not be a lot of opportunities for foreign private special situations investors to feed local demand.

"Foreign private equity is not targeting China distress due to decoupling, the trickiness of cross-border enforcement, and the fact that it is subordinate to onshore debt," Jong added. "I'm currently quite pessimistic that kind of investment will go back to the level it reached in the past few years."

Special situations in China have therefore proven most viable at the larger end of the market, where infrastructure-style deals can be framed as part of the fabric of an inevitable economic march. Bain Capital Special Situations demonstrated this opportunity earlier this week by setting up a USD 250m advanced manufacturing investment platform with Chinese industrial park developer DNE Group.

The investment, which did not include any debt or distress component, reflects Bain's mostly expansion-oriented philosophy about special situations. This includes bespoke capital structures featuring equity upside with credit-like downside protection, as well as pre-emptively approaching opportunities before they become distress situations.

Since closing its second Asia special situations fund mid-last year on USD 2bn, Bain has grown its team for the strategy in the region from about 90 to more than 100. These hires span Hong Kong, Japan, Australia, and India. There is now more than USD 4bn for special situations in the region, including separately managed accounts.

Bain deployed more than USD 1.5bn under the strategy in Asia during the 12 months to September, which does not include the DNE deal or a USD 200m convertible shares commitment earlier this month to Vietnamese conglomerate Masan Group. That rate of investment is expected to increase in the years to come.

"We're open for business and continue to be constructive on China, which a lot of firms are deemphasising these days as many GPs and LPs shift focus," said Kei Chua, a partner at Bain.

"Deal volumes dropped in the country in the past year because a lot of companies were not willing to accept market pricing and deal terms as rates increased overseas, but locally stimulus measures continued to create unrealistic benchmarks. There's still a little of that going on, but companies are now more accepting that they need to raise capital and be more flexible as their loans and bonds mature and stimulus measures continue to abate."

Heavy lifting

The Bain approach, emphasizing industry expertise and ample resources, is a reminder that despite the notion that distressed companies will effortlessly recover in rebounding industries such as afterschool care and air travel, robust operational capability remains indispensable.

Much of this work will be more relevant to existing portfolio companies than new turnaround opportunities. The most commonly cited areas of operational improvement that have come to the fore in the current environment include inventory, workforce and supply chain optimisations.

Inventory is often most relevant in retail, where supply chain uncertainty during the pandemic encouraged businesses to over-stock. Workforce issues span labour shortages in tech and healthcare to sub-optimal sales team deployment in retail showrooms. To some extent, private equity firms are using artificial intelligence to replan these rosters.

In addition to surplus inventory, supply chain challenges during COVID-19 led to excessive logistics footprints and now-unnecessarily expensive shipping arrangements. The fix here can be as simple as dropping ocean freight contracts signed during a mid-pandemic spike in pricing. The hard yards will be in diversifying geographic risk by establishing various in-market sourcing hubs.

Timo Schmid, a managing director with Alvarez & Marsal's private equity performance improvement practice in Australia, has also observed a significant amount of turnaround work being done in terms of marketing planning processes and more nuanced back-end operations.

"We've seen a lot of PE firms trying to make their portfolio companies more sophisticated in how they plan what they actually sell in terms of SKUs [stockkeeping units], how they're actually going to deliver it, and how they can countermeasure quickly when things go off the tracks," Schmid said.

"There's a wave or processes around getting smarter in that sales and operations planning, which does require a lot of intellectual heavy lifting."

One of the most novel aspects of the current environment is that, for the first time, distress situations in salvageable early-stage tech companies are part of the turnaround opportunity set.

While delayed pandemic aftershocks have tanked tech valuations globally, many of these overextended start-ups are fundamentally sound businesses. When their creditors finally come calling, they are not often seen as turnaround opportunities for incoming investors, but for existing investors, the operational fixes will be not unlike those playing out in more mature businesses.

Jason Kardachi, a Singapore-based managing director at Kroll with 27 years of experience in Asia restructuring, is seeing start-up deal flow for the first time in his career. Interest rate pressure in the wake of the Silicon Valley Bank collapse has created a small but growing new line of business, where bloated, loss-making companies can be stabilised and relaunched.

"We often restructure on behalf of lenders, so this is a slightly unusual and challenging environment for us. We can't magic these companies to be profitable, but we can add value by realigning to current market conditions," Kardachi said.

"One of the key things that's specific to these kinds of tech businesses is mindset change. Both the management and the investors need to be more realistic about the build-it-and-they-will-come growth model."

Happy ending

Kroll's first experience in this area is also its key success story and proof-of-concept. In mid-2022, the consulting firm was appointed as receiver for HappyFresh, an Indonesian grocery delivery platform that had received backing from the likes of STIC Investments, Grab Ventures, Line Ventures, Samena Capital, 500 Startups, Vertex Ventures, and Sinar Mas Digital Ventures, among others.

Kroll ended an overambitious expansion into Thailand and Malaysia, concentrating resources on core operations in Indonesia. An ancillary supermarket venture with significant upside but cumbersome and expensive logistics was nixed. Headcount was sharply reduced. Supplier contracts were optimised and technology R&D was curbed.

By the time a sale process was launched three months later, cash burn was less than USD 50,000 a year and on its way to positive territory. One new investor, albeit an existing shareholder, came in during this process. HappyFresh was back in business by September 2022.

There is a lesson for minority equity investors in this story. Only about 10% of the start-up's approximately USD 180m in private funding at the point of its cash crunch was debt, yet it was the creditors that put Kroll in charge.

When Kardachi came in, the app had been switched off for three weeks, a move he saw as a result of panic by a VC-heavy board. He immediately turned the app back on, reasoning that there is no value to preserve if there is no business.

"Private equity investors do not tend to be very good in these environments as board members," Kardachi said. "No one has control, there are concerns about personal liability, and it ends up with this real gridlock of nothing happening – which can be even more damaging for the business. A lot of what we do is common sense."

More on Australasia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.