Japan buyouts: Bucking the trend

Japan remains a private equity hotspot despite muted buyout activity elsewhere in Asia. Take-private and sponsor-to-sponsor opportunities make for a more textured local market

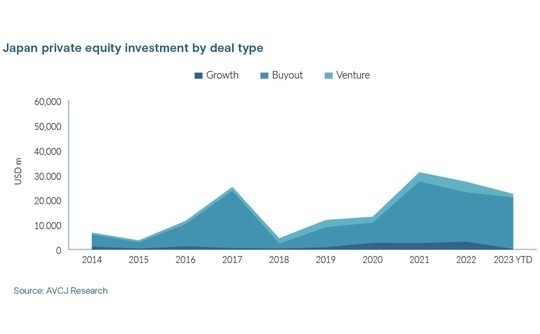

Nearly USD 20.7bn has been committed to Japan buyouts so far this year, beating the 12-month total for 2022 in less than half the time. However, 90% of the capital went to two deals: Toshiba Corporation and Works Human Intelligence, at JPY 2trn (USD 15.9) and JPY 350bn, respectively.

Japan has proved a lumpy market in recent years, with a handful of supposedly idiosyncratic buyouts underpinning headline investment numbers. Five USD 1bn-plus mega deals accounted for 70% of the buyout total in 2022, while four were responsible for 61% in 2021, according to AVCJ Research. Years of feast are interspersed with years of fallow. In 2018, no buyout crossed the USD 1bn threshold.

At the same time, Japan has confounded the sharp decline experienced region-wide from the record high of 2021. Investment in Asia – across all private equity strategies – fell by more than one-third in 2022; Japan was down 12%. Toshiba casts a shadow over 2023, but the middle market is humming: 119 buyouts were announced in 2022, up from 87 in 2022; 43 have been logged in 2023 to date.

"What's changed is the relative positioning of Japan in the global markets. Previously, people appreciated fast-growing, start-up-style businesses. The way the world is shifting now, there is a recognition that growth in Japan might be slower, but it's stable and delivers attractive risk-adjusted returns," said Takanobu Hara, a partner at BPEA EQT. "You could say we are less cyclical."

This faith in Japan's innate resilience – investors point to an economy driven by a conservative, over-equitized consumer base rather than more volatile investment and export flows – dovetails with structural trends. Corporate carve-outs and founder-succession remain the private equity mainstays, and there are expectations of more public-to-private and sponsor-to-sponsor transactions.

Paul Ford, a Japan-based partner at KPMG, endorsed the notion of a flight to stability, whether that constitutes a pullback from emerging markets from investors in risk-off mode or a geopolitics-driven avoidance of China specifically. He recalls investors saying they have slowed down in other markets "but not in Japan, with a clear message from the mothership back home to deploy as much capital here as possible."

Representatives of most private equity firms that spoke to AVCJ claimed that deal flow is at, or close to, record levels, although feedback was mixed as to how much of this activity translates into agreed transactions. Ford is of a similar mind. His team is fully booked up with private equity work for the next six months yet notes that the first few months of the year have been relatively slow.

AVCJ Research has records of just two USD 1bn-plus buyouts – Toshiba Corporation and Works Human Intelligence – and only one in the USD 500m-USD 999m category. The five USD 1bn deals across the whole of 2022 were accompanied by four in the USD 500m-USD 999m bracket. This compares to seven in 2021 and four in 2020.

Auction angst?

Pent-up deal flow at the large end of the market includes two carve-outs apiece from Fujitsu and Mitsubishi: air conditioner manufacturer Fujitsu General and semiconductor packaging specialist Shinko Electric Industries (the former is more advanced than the latter); and Mitsubishi Chemical Group's Qualicaps capsule division and Mitsubishi Electric's automotive equipment business.

Progress on deals such as these has been sluggish because of an unbridgeable gap in seller and buyer expectations on pricing, according to sources familiar with the situation.

Toshiba moved forward only after the Japan Industrial Partners-led consortium cut the price by 16% between submitting an initial offer last September and agreeing on a deal in March. A downward revision in Toshiba's projected earnings, a fall in the value of the company's stake in flash memory business Kioxia, and reduced availability of debt financing were given as reasons.

"The wave of carve-outs is continuing, although at this point in the economic cycle, there can be valuation gaps between buyer and seller. Japanese companies like to price off the public markets and when they own chunks of public companies, the pricing is out there," said David Gross-Loh, a managing director at Bain Capital.

"Japan's stock market is trading at attractive levels with the depreciation of the yen and low interest rates driven by the central bank's easy money policy. This is leading to high price expectations at a time when some companies' earnings prospects are weakening with global economic pressures."

Should the deadlock break later in the year, there is appetite and capacity to complete these deals. T.J. Kono, a partner at Unison Capital, is one of several local investors claiming to see increased interest from overseas in the last 6-12 months following the end of Japan's pandemic restrictions. And, unlike Western markets, there is plenty of debt available to support leveraged transactions.

"Financing is still attractive from our perspective. Interest rates went up around 0.3% but the spread hasn't really changed. LBO financing is an important revenue source for the big banks – they want to carry on providing loans at 2%-2.5% upfront fees," said Atsushi Akaike, co-head of Japan at CVC Capital Partners.

Akaike has noted a slowdown in large-cap deal flow, which is attributed to pricing for some of the carve-outs. However, CVC is working on several founder-succession transactions – including situations where it is trying to find a solution that meets the needs of all family members, some of whom want to cash out while others want to remain – and a take-private.

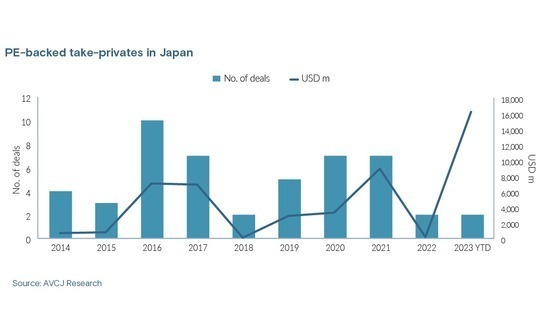

Off the exchange

Japan has delivered a steady stream of public-to-private opportunities in recent years, although they are often succession or carve-out deals in disguise: the founder who wants to sell a large, relatively illiquid position in a public company; the conglomerate divesting a listed subsidiary in which it holds a minority stake. PE investors agree to buy these positions and launch tender offers for the rest.

Reforms introduced by the Tokyo Stock Exchange (TSE) may lead to another take-private angle. Companies that trade below book value have been instructed to disclose steps taken to remedy the situation and TSE is effectively encouraging shareholders to take management to task on it.

This follows a reorganisation of TSE's market segments as prime, standard, and growth, and more stringent qualification criteria for each one. For example, a place in the prime segment for an already listed company is conditional on maintaining a liquid market capitalisation of at least JPY 10bn. Newly listed companies must achieve minimum revenue and profit thresholds as well.

"There is a recovery period, but those that still don't meet the criteria will be delisted or move into the standard section. A lot of institutional investors can only invest in the prime section, so companies on the outside might see their stock prices go down. They are likely to be candidates for take-privates," said Tsuyoshi Yamazaki, a partner at Integral Corporation.

TSE's recent initiatives represent another means of holding companies accountable for their performance. Toshiba is also wound into this compounding effect, given the role activist investors played in exposing poor governance, facing down management, and securing an outcome deemed more beneficial to shareholders. Activists are now a feature of the Japan investment landscape.

Even if more take-private opportunities emerge – and it is expected to take several years for the impact of the reforms to be felt – they might be difficult to execute. Ford of KPMG highlights the need for strong relationships with the target's management and major shareholders if these deals are to proceed in a friendly fashion. There could also be disruptions along the way.

Asked to list the principal challenges of take-privates, Kazuhiro Yamada, head of Japan at The Carlyle Group, identified the need to pay a premium that might not be justifiable. He added activists exploiting diversified shareholder bases to oppose offers in the hope of securing a higher price, and the risk of information leaks, and subsequent stock price booms, when a parent sells a listed subsidiary.

This is largely endorsed by Bain Capital's Gross-Loh, who warned against underestimating bottom-up resistance to deals, despite a general openness to private equity support in Japan. "In cases where companies have distributed ownership or multiple stakeholders, creating consensus is more challenging," he said.

The Longreach Group's tender offer for Japan Systems in 2021 is a case in point. On learning that DXC Technology, the US parent of Japan Systems, had agreed to exit through the process, the Japan Systems CEO sought third-party support for a counterbid, according to a source close to the situation. He didn't get anywhere because DXC insisted it would only sell to Longreach.

Pass the parcel

T Capital Partners has never done a take-private before, but the mid-market firm is among those now meeting with CEOs about potential deals, driven in part by inbound enquiries.

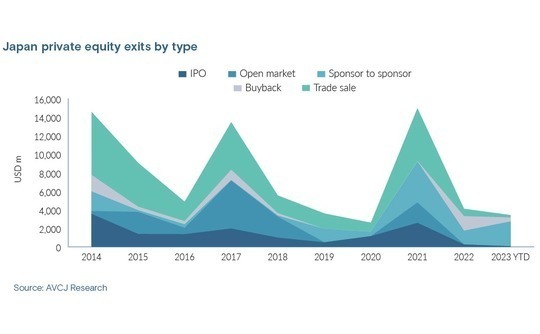

The priority, however, is securing exits. T Capital has made four investments – not including bolt-on acquisitions – since the start of 2020 but its most recent exit was before the pandemic. Koji Sasaki, the firm's managing partner, noted that the number of portfolio companies has swollen to 10 – normally it's five or six – because Japanese strategics have been selling rather than buying assets.

Unison is in the same position, having deployed nearly half its latest fund within 18 months of the final close while exits have been scarce. "Especially during COVID, when restrictions were stringent, there were very few exits, so there has been a build-up in inventory that needs to be cleared. I don't think we are exceptional in that regard," said Kono.

Bain & Company highlighted the issue in its 2023 Japan private equity report, noting that average investment transaction value has doubled on a five-year trailing basis while exits are on the slide. Approximately 80% of deals from the 2017 vintage are still held in funds. Will this pressure on liquidity lead to a surge in sponsor-to-sponsor deals in the absence of other exit options?

"Normally, we would have seen more exits from 2017, 2018, and 2019, but people are sitting on them," said Jim Verbeeten, a partner at Bain & Company. "If you cannot do an IPO, a secondary becomes progressively more interesting. There are also global investors that are new to Japan and want to do something here. As a de-risked asset, a secondary can be an attractive first step."

This reflects not only greater willingness and resources to compete for assets but also deeper private equity penetration of corporate Japan. More GPs are active at different levels of the market, creating opportunities for one manager to fulfil its investment thesis and then exit to a second manager with an agenda that is tailored to the next stage in the portfolio company's development.

It doesn't necessarily follow that businesses pass from local to global GPs. Jewellery retailer Primo Japan is onto its fourth consecutive PE owner: the three most recent are BPEA EQT (then pan-regional), Longreach (North Asia), and now Integral (local). Carlyle and CVC have both exited assets to local GPs, while various companies have travelled through the tiers of Japan's middle market.

According to Koichi Tamura, an associate partner at EY, most private equity firms active in Japan have teams on the ground. As such, it's not so much about local versus global as what is the best fit. "Which house has the most value-add capability or insight into the target industry or has another portfolio company where there might be synergies? That's how they look at it," he said.

Koichi Kibata, a co-founder and partner at D Capital, which acquired snacks maker Oyatsu from Carlyle at the end of last year, emphasised fundamental differences in the investment theses. While Carlyle supported overseas expansion by Oyatsu, D Capital's agenda includes digitalisation and the rollout of protein-based snacks. The local GP positions itself as a digitalisation specialist.

Budding bona fides

Developing a business to the point where it appeals to a large-cap sponsor can be challenging in low-growth Japan. Unison's Kono noted that it means tripling enterprise value on the back of a concerted transformation effort, while T Capital's Sasaki added that he would expect to be looking at a 10x return after scaling up a company to a relevant size.

A broader question is whether the management of a portfolio company wants to continue under private equity ownership. Yamada said that Carlyle holds discussions with management teams regarding the most appropriate exit route and they tend to favour an IPO or sometimes a trade sale if they want to expand their capabilities.

"We explore all options, but we work with management to meet their needs," he explained. "Some management teams don't like exits to other sponsors because they want to seek growth opportunities without a heavy debt burden."

In this context, a manager's internal resources are heavily scrutinized. They might draw on value-creation credentials to sell an expansion story to management and other stakeholders or dip into their networks to find professionals who can augment or replace those running the target business.

Private equity investors in Japan have always struggled with a talent bottleneck at the portfolio level, while C-suite imports often fail to overcome language and culture barriers. As the asset class has become more established and proven, there is a small corps of local executives who are attuned to the PE model of relatively concentrated bursts of intense, incentive-driven transformation.

"We have brought people from past portfolio companies to help run current portfolio companies, if they are suitable and available," said Toshitaka Shimizu, an Asia-based partner at L Catterton. "Are there many of them in Japan? No. But there are cases where those who have worked with private equity firms before go from one portfolio company to another."

Akaike of CVC adds that competition for CEOs with private equity experience is fierce, so there is a need to invest in youth. In a career that spans Advantage Partners and CVC, he has worked with the CEO of massage salon chain Riraku – which has been owned by both GPs – four times.

The gradual emergence of more management talent, the still lumpy large-cap deal flow, and the mainstreaming of new investment themes that sit alongside carve-outs and founder-succession are emblematic of an industry that is maturing. Yet the shift from explaining how private equity works to demonstrating the value it can bring requires some heavy lifting.

"It is necessary to do more work prior to consummating a transaction in Japan compared to Western Europe and North America. Japanese organisations tend to be more consensus-driven, so they require more convincing," said Hara of BPEA EQT. "You need to show you have the right platform and angle to be the next owner."

More on North Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.