GP profile: Falcon House Partners

Falcon House Partners is one of the few survivors in Indonesia’s promising but challenging middle-market private equity space. Being hands-on is part of the secret

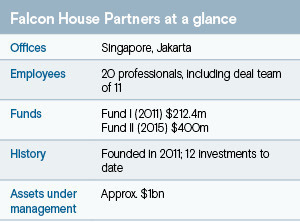

When Falcon House Partners set up with an exclusive focus on Indonesia's middle market in 2011, the idea of shifting investment attention from the country's historically commodities-focused economy toward an upwardly mobile consumer market was well established. By that point, consumer demand already represented 60% of the domestic economy.

The Singapore-headquartered private equity firm identified Indonesia as one of the few countries in the world with secularly high GDP growth and a low-debt-to-GDP ratio, which put it on track to outperform seemingly similar markets in the decades to come. Indeed, these advantages are credited with recent successes such as a current account surplus and a quick COVID-19 rebound.

"Highly responsible government with disciplined fiscal and monetary policy played a key role in the decision to, quite frankly, dedicate our careers to investing in Indonesia," said Brian O'Connor, a co-founder and managing partner at Falcon House.

"Indonesia has the lowest quarter-to-quarter GDP volatility of any major emerging market, and even compared to many developed markets. This provides a more predictable backdrop for investment."

Nevertheless, the challenges of practicing private equity in Indonesia are easy to infer. In the early years of Falcon House's history, a healthy crop of competitors emerged. Most were unable to raise funds and either vanished or returned to corporate advisory work. Even some of the pre-2011 incumbents no longer exist. Overall, the number of active middle-market GPs has reduced.

Falcon House attributes its longevity not to an ability to pivot but to a steady hand on the tiller. Consumer and healthcare, including B2B models, were the core areas of focus from the beginning, especially in categories where companies could enjoy a multiplier effect on rising GDP.

Core themes include scalable brands, millennials, healthcare transformation, digitisation, buy-and-build, and regional winners. Cheque sizes have ticked up slightly over the years; the range is currently USD 25m to USD 60m. There is a preference for control, but significant minority deals are considered.

"If you only do control deals, you're limiting yourself," said Samir Soota, a co-founder and managing partner. "There are a lot of good minority deals available, but you have to have the right structure and alignment with other shareholders."

Voices of experience

O'Connor and Soota have been colleagues and friends since the 1990s, when they also crossed paths with Glenn Yusuf, whose career in Indonesia extends to 1981 in Citibank's Jakarta office.

O'Connor's experience in the country is rooted in an 18-year stint with Lehman Brothers, while Soota has worked for various banking and consulting groups, as well as Principia Management Group, a private equity firm he established as the portfolio-servicing arm of Quvat Management in 2006.

Meanwhile, Yusuf was president-director of Danareska in the 1990s when the investment bank claimed a more than 50% share of local M&A coverage (Soota was a managing director at Danareska at this time). He moved on to the Ministry of Finance where in 1998, as head of financial institutions, he negotiated a landmark debt restructuring deal with the IMF called the Frankfurt Agreement.

Credibility was the key to early pipeline creation and fundraising. Falcon House's debut vehicle launched in March 2012 and reached a first close of USD 100m that August thanks largely to speedy commitments from development finance institutions (DFIs). The US-based Overseas Private Investment Corporation – now the Development Finance Corporation – contributed USD 60m, according to AVCJ Research.

A final close of USD 212.4m came the following year with support from Germany's DEG, Netherlands-based FMO, the International Finance Corporation (IFC), Swiss Investment Fund for Emerging Markets, and Asia-focused fund-of-funds Emerald Hill Capital Partners. Alexander McCloskey, Falcon House's head of investor relations, is a former partner at Emerald Hill.

Fund II launched in 2015, achieved a first close of USD 200m by year-end and a final close of USD 400m in November 2016. LPs included IFC, which invested USD 25m, FMO (USD 20m), and DEG (USD 16m), as well as fund-of-funds and other global institutional investors.

"All three partners have skin in the game with a significant GP commitment," Markus Bracht, a vice president at DEG observed, adding that the firm's operational abilities were also an important draw.

"We see Falcon House being actively involved in portfolio support, and in many cases, this goes beyond board representation, governance advice, HR support, regular interchange and brainstorming on strategic topics."

Value-add resources include a network of 10 operating advisors, offering expertise across areas such as hospital administration and fast-moving consumer goods. Third-party vendors are typically brought in to consult on areas such as legal structuring, licensing, branding, and environmental, social, and governance (ESG) compliance.

Up to 12 professionals can be deployed on a single deal at a given time, half of whom will be Falcon House employees who qualify for carried interest should the investment outperform and the fund achieves its hurdle rate. The staff currently includes 20 professionals. Of these, 11 are primarily focused on deals but regularly engage with the operations team.

There is also a significant in-house communications function, which entails twice-yearly workshops and ideation sessions with portfolio companies in addition to monthly board meetings and annual meetings. When COVID-19 hit, regular LP advisory committee meetings were augmented with quarterly update calls.

Pandemic resilience

The lockdowns of the early pandemic were Falcon House's biggest challenge to date, a showcase for its portfolio support processes, and a counterargument to the point that longevity in Indonesia is more about staying the course through cycles than emergency manoeuvres.

The biggest move in this vein was the raising of the USD 13m COVID-19 liquidity infusion plan, or CLIP, which included a USD 6m contribution from DEG, plus USD 6m from FMO and USD 1m from Falcon House. This was said to have preserved thousands of jobs and brought the portfolio back to its pre-pandemic valuation.

Mount Scopus, which operates a chain of brick-and-mortar bakeries under the Harvest brand, could have been one of the worst hit companies during lockdown had it not been modernised in the prior two years.

Falcon House acquired a controlling position in the company for USD 15m in 2017 and achieved little growth in the following year as it scouted for a replacement CEO. Retail and food industry veteran Edison Manalu was eventually recruited in 2019. As part of the interview process, he was asked to consider ways of turning around the business.

Manalu recognised Mount Scopus's critical bottlenecks involved inventory and logistics inefficiencies. With support from one of Falcon House's operating advisors, he devised a more centralised distribution and production process – which enhanced quality control – and added a surprisingly absent cold chain function.

Online sales jumped from 20% to 45% of revenue, and Manalu believes it can hit 55% in a few years. Since 2019, overall sales have climbed 22% a year while EBITDA has grown 35% a year. During this period, the company pushed deeper into lower-tier cities and the relatively sparsely populated island of Borneo.

"Falcon House accepted and supported my point of view. I was free to manifest the plan, and they only gave big-picture advice. That's the culture," Manalu said. "Chemistry is very important to me. I saw the culture was very open-minded with open communication. That's critical to the whole team. The company is a second family for me. Besides the strong brand of Harvest, that's why I joined."

Falcon House is in the midst of launching a sale process for Mount Scopus but declined to comment. The company is being well received by potential investors, according to a source close to the situation, with the new digital operational model doubtlessly a significant bargaining chip.

"We are seeing a convergence between online and offline, where businesses realise they need to be omnichannel," Soota said. "We've seen this happen in other markets, and we believe it's an area where we can work with companies."

Digitisation dynamics

It's worth noting that in addition to Gojek, Mount Scopus' sales and logistics network includes VC darlings the likes of Grab, Traveloka, Tokopedia, and Shopee. Although Indonesia's mid-market private equity players are thinner on the ground, their portfolios have been supported in recent years by a thriving start-up scene and generally higher rates of economic digitisation.

O'Connor sees local VCs as partners with the ability to build and develop young companies to a point where Falcon House can play a role in their further growth. He also regards the ecosystem as an invaluable resource for targeted marketing that dovetails with consumerism and productivity momentum related to urbanisation.

"It's really important to work with the senior management of companies to make sure that they're fully aware of the all the digital tools that are available to them," O'Connor said. "There's been an evolution of what it means to be a great CEO, CFO, and CMO [chief marketing officer] in Indonesia in the past five years. And we need to help make sure these C-level executives are staying competitive."

Falcon House's latest sizeable deal highlights another angle on VC support for the middle market. The firm led a USD 170m Series B round for transportation, warehousing, and fulfilment player Sicepat, taking a less than 10% stake. It claims the profitable company has graduated past start-up status.

The investment included support from DEG, Kejora Capital, MDI Ventures, Indies Capital, Pavilion Capital, Trihill Capital, and Daiwa Securities. The idea is to fortify what is already considered a leading position locally in the end-to-end logistics segment – including last-mile delivery – while exploring expansions into other Southeast Asian markets.

Sicepat has capacity to deliver more than 1.4m packages a day and is regarded as one of the few players that can service both traditional e-commerce and social commerce partners. It is banking on projections that Indonesia's e-commerce market will grow 21% a year over the next five years, hitting USD 82bn by 2025. About 25% of that market is expected to be defined as social commerce.

This was the first investment of its kind for Falcon House, which stresses it has no interest in early-stage exposure. But there is scope for more, especially as the lines blur between the VC and PE ends of the asset class locally. As a case in point, one of Falcon House's existing portfolio companies, lifestyle brand Isayama Group, received a USD 18.1m round last month led by East Ventures.

"We certainly see some VC-backed companies that have grown and matured to the point that they fit our strategy and value-add," Soota said. "On the other hand, we're also seeing some VCs doing more than start-ups, and they're interested in the growth and scale of some of our portfolio companies."

The notion of a maturing start-up ecosystem feeding a larger pool of modern, investable midcap businesses comes to Indonesia at the same time as several tectonic shifts in the macro. Most significant is the idea of industrial capacity and investment dollars moving away from China amidst closed borders and geopolitical friction in favour of Southeast Asia.

Falcon House could leverage this environment soon. The firm has not formally launched its third fund, but feelers are being put out. As part of its annual LP communications routine, the GP's leadership travels to the US and Europe during the northern hemisphere summer to touch base and update on performance.

"The feedback we're getting is that there's been quite a bifurcation in emerging markets in terms of performance," said O'Connor, who is currently in the US. "Dislocations and challenges in China are playing on people's minds. But Southeast Asia, and Indonesia in particular, has attracted attention."

More on Southeast Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.