Asia fintech: Platform plays

Expansion is the dominant theme in financial technology as start-ups leverage existing assets to enter new verticals, typically in lending. Which ones will become Asia’s preeminent platforms?

An ambitious and expansive Southeast Asia growth story lurks behind the $30.4 billion valuation placed on Grab, an as-yet unprofitable ride-hailing and local services platform that is set to go public through a merger with a US-listed special purpose acquisition company (SPAC).

Grab operates an ecosystem that spans eight countries and includes 25 million monthly transacting users, five million registered driver partners, and two million merchant partners. Gross merchandise value (GMV) hit $12.5 billion last year.

The company expects its total addressable market to grow from around $52 billion in 2020 to more than $180 billion by 2025. But ride-hailing and food delivery, the foundation stones of Grab's business, are projected to account for about one-quarter of this expanded GMV. The rest will come from digital wallets and the myriad financial services that could be bolted on.

It underlines a conviction shared by many investors in Southeast Asia: financial services are the key technology battleground. Moreover, Grab's projections represent an ambition of dominance, not a realized position. While platforms exist in payments and lending, the ability to leapfrog a generation of legacy systems and go straight to mobile means there is much to play for – whether start-ups are pursuing wallet share, serving the disrupters, or selling to incumbents trying to offset disruption.

"In most mature markets, there is established infrastructure that's hard to disrupt or will take a long time to disrupt. In Southeast Asia, it's much easier because two-thirds of the population is unbanked, 95% don't have credit cards, and 98% don't have insurance, yet everyone has a smart phone," says Jeffrey Perlman, a managing director and head of Southeast Asia at Warburg Pincus. "And then the pandemic has been a huge accelerant in pushing more folks to leverage technology platforms."

China redux?

China is the logical reference point when mapping out the future of fintech in Southeast Asia or India, the region's other two preeminent emerging markets. Yet the template is of dubious applicability. Alibaba Group's Ant Group and Tencent Holdings-owned WeChat Pay moved faster in building fintech powerbases on top of their core e-commerce and social networking and gaming businesses than the regulators could in issuing licenses and creating standardized frameworks.

Ant Group's IPO prospectus boasted of establishing "the ‘capillaries' of the financial system to complement the ‘arteries' operated by major financial institutions," with interests in lending, investment services, and insurance, as well as payments. Since the IPO was halted last November, regulators have curbed the fintech ambitions of internet companies. This includes forcing them to finance a larger portion of loans off balance sheet rather than shifting exposure to third parties.

The same scenario is not expected to play out in Southeast Asia and India. First, these markets are several years behind China, which allows regulators more time to plan and respond. Beyond that, there are all manner of local nuances, from the cultural, linguistic, and regulatory diversity of Southeast Asia to the steps India has taken to create a level playing field.

"In Indonesia, there are large platforms that want to be all-encompassing digital commerce and fintech platforms, but I don't think the business model quality is strong enough to build a dominance like Alibaba or Tencent. Even though large platforms have lots of capital and can dominate from a talent and discount perspective, independent players can become market leaders," says Ganesh Rengaswamy, a managing partner at specialist emerging markets fintech investor Quona Capital.

As for India, he highlights the complexity of the market. There are strong payment platforms – such as Paytm and PhonePe, which both have ties to e-commerce – but "payment dominance doesn't necessarily mean you can provide a broader suite of services with the same level of dominance."

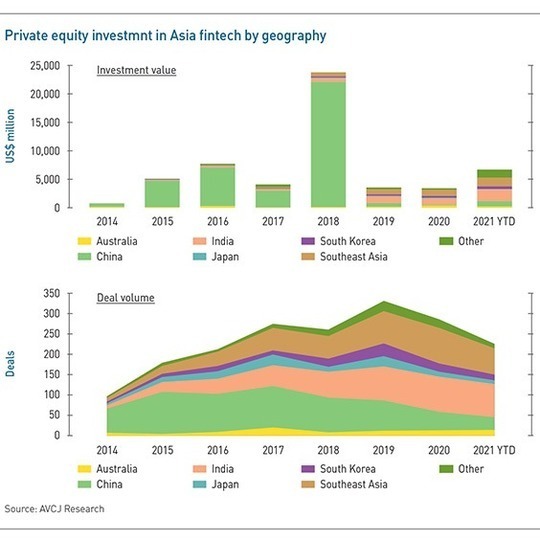

Over the next three years, $35 billion was deployed, nearly all of it in China. Nine companies – Ant Group and three peers, four P2P lenders, and an online insurer – received over $26 billion between them. Ant Group's $14 billion Series C was the high point. Viable platform plays were always few, and then within a year, P2P lenders were ordered to pivot or fold. The more recent regulatory upheavals have made fintech toxic to investors, unless accessed via another sector like healthcare.

Since 2019, $1.7 billion has been committed to China fintech players, out of $13.6 billion region-wide. Meanwhile, India and Southeast Asia have gone from strength to strength, receiving $4.3 billion and $3.4 billion, respectively. These totals do not include investments in the likes of Grab and GoTo, where fintech represents an ever-larger portion of mobility and delivery-oriented offerings.

Expansion plans

The notion of horizontal expansion is not limited to large consumer-facing internet platforms, nor is it fashioned around payments. Chee-Yann Wong, a managing director at Northstar Group, observes that five years ago, e-wallet and payment providers were aligned with ecosystems in Southeast Asia.

More recently, the fintech landscape has proliferated as adoption rates have accelerated. Specialized fintech players have emerged and are either trying to align with ecosystems or forge their own paths – across digital lending, insurtech, and enterprise software-as-a-service (SaaS).

"Companies want to build auxiliary recurring revenue – fintech companies are going into software and services, so they can get more data and have more customer relationships, while non-fintech players are trying to build fintech revenue streams using their data," adds Khailee Ng, a Southeast Asia-focused managing partner at 500 Startups.

"We see P2P lenders building accounting software for companies to track payables and receivables, so they can become digital banks for SMEs. We see start-ups that are in cash management and financial literacy offering loans and insurance because they know a lot about their customers."

The overarching question is whether size is a panacea. Large platforms may ultimately make their customer insights count. Multiple touchpoints with users offer insights into behavior that potentially enable platforms to not only improve profiling and credit decision making, but also offer financial services to users before they know they need them, pushing down the cost of customer acquisition.

It is not unfeasible that flywheels emerge whereby better customer loyalty supports capital raising, which in turn facilitates investment in customer acquisition and product development. These platforms could leverage their power to push through the consumer-facing layer into the technology service provider and banking layers below, taking full ownership of the ecosystem.

This possibility already makes investors mindful of where and how they commit capital. Northstar, for example, revamped its approach to financial services in 2019 by participating in the acquisition of Indonesia-listed Bank Artos with a view to creating a digital lender. There are two key strategic partners: Bank Tabungan Pensiunan Nasional, a former portfolio company, reflects Northstar's longstanding sector expertise; and GoTo, an existing portfolio company, represents the future.

Rather than launch its own bank, GoTo is integrating its app with Bank Artos – now known as Bank Jago – as a regulated beachhead for customers that want to open accounts and access related services. Bank Jago's app has been downloaded nearly 700,000 times since integration began earlier this year, with 150,000 deposit-holding users signing up each month. The bank has a market capitalization of IDR216 trillion ($15 billion), having seen its stock rise 348% year-to-date.

"There are several large ecosystems in Indonesia, so fintech players must think about how they align themselves with these ecosystems to scale," says Sunata Tjiterosampurno, co-CIO of Northstar. "There are natural transitions from lending to wealth management to insurance. You are targeting the same set of customers, so it's a question of how you increase your wallet share in terms of financial services."

How defensible?

It remains to be seen how defensible other segments are to platform encroachment. Kredivo, which recently agreed a SPAC merger at a valuation of $2 billion, established itself as Indonesia's leading BNPL lender at a time when cash-on-delivery dominated in the absence of credit cards and reliable bank transfer technology. Partnerships with eight of the country's 10 e-commerce platforms, including Bukalapak and Shopee, were crucial to the company's emergence.

"Some players have done a great job to get scale and serve horizontal e-commerce players. But as these large platforms look for new monetization methods, will they continue to partner to offer that service or do it themselves? Or will it be a combination of both?" asks Louis Casey, a principal in KKR's growth-stage technology team. "Given the volumes these e-commerce platforms are pushing through, if they choose to do it themselves, that's a scary proposition for an embedded credit provider."

Kredivo's response is to pursue its own diversification agenda. The company already provides credit financing for offline purchases and has branched into other lending categories such as personal loans. It also wants to launch a digital bank.

Amit Anand, a founding partner at Jungle Ventures, which is an investor in Kredivo, believes the company has staying power. Prior to investing in 2016, Jungle examined similar business models across the US, China, and India, and concluded that – for transaction finance – product quality is more important than ecosystem alignment.

"The Kredivos of the world are scaling because they are agnostic and can be used across multiple platforms, and they are product-first companies," he says. "Its core business is BNPL, whereas for Shopee it's one of 50 product priorities. Some of these large platforms have BNPL, but it hasn't killed Kredivo, it has expanded the customer base. So independent platforms will continue to succeed."

And then the point about Southeast Asian platforms lacking the power of their Chinese peers is reiterated. A Chinese consumer might use WeChat multiple times each day, creating ample opportunity to influence behavior; for Grab or GoTo in Southeast Asia, it might only be two or three times. Jungle's feedback from portfolio companies that partner with such platforms is that the additional transaction flow is helpful but not transformative.

These dynamics may change when the merger that formed GoTo – between transportation, food delivery, and financial services super app Gojek and e-commerce player Tokopedia – is fully baked in.

Inside India Stack

The platform debate in India is shaped by India Stack, an ambitious government-led initiative to create unified, interoperable digital infrastructure. It covers biometric identification, paperless documentation, data security, and a unified payments interface (UPI) to facilitate cashless transactions. While Alibaba and Tencent stole a march in China and created closed-loop ecosystems anchored by their own digital wallets, India effectively prevented anyone from doing the same.

"UPI was designed to reduce the frictional cost of making payments and enable more people to access the digital economy," says Udayan Goyal, a managing partner at Apis Partners, another emerging markets fintech investor. "Traditionally, for a payment of $100, the $2 charge levied on the merchant would be split between the payment provider, the scheme [or wallet], and the bank, with the bank getting the lion's share. With UPI, the charge is $0.10 rather than $2."

Consequently, India discovered – faster than anyone else – that the payments space is no cash cow. For payment start-ups, it is the mode of customer acquisition but not the means of monetization. That's why Paytm, the country's preeminent consumer wallet, has pushed aggressively into value-added services like banking, insurance, wealth management, and e-commerce and lifestyle services.

Meanwhile, point-of-sale terminal providers continue to roll out UPI-compatible QR code systems, but these are offered in tandem with pre-paid gift cards, loyalty programs, BNPL, and other lending services. BharatPe is arguably the poster child of the push into lending. Working with a non-banking financial company (NBFC), it has won approval to create a small finance bank and plans to merge that entity with a distressed local lender. The goal is to offer merchant-focused credit and savings products.

Some industry participants are skeptical of this strategy. Quona's Rengaswamy notes that expansion from payments into value-added services has yet to be proven, and those pursuing it are better known for how quickly they became unicorns than for the robustness of their business models.

"Whatever monetization BharatPe had in alternate payment acceptance, it moved away from that. It is bearing the infrastructure cost of running these payment operations without charging for them in the hope of capturing enough data to be able to offer other services," he says. "It is a long-winded approach. Once you drive the price of something down to zero, you are on the back foot. You are under pressure to make the other business model work, and we are still in the early days for that."

The fundamental concern is that platforms are raising capital to last out the competition, but neglecting to develop capabilities in underwriting, risk assessment, and pricing required to be sustainable lenders in the long term. This resonates across the region, where generic P2P lenders – typically offering unsecured products – have been through waves of exuberance followed by waves of defaults. Southeast Asia is no exception.

"Plenty of platforms in Southeast Asia had been risk-on, rushing in and messing up their books in the process. With unsecured lending products, it is critical to have the right foundation for underwriting risk," says Sandeep Naik, a managing director and head of India and Southeast Asia at General Atlantic.

"If underwriting were as easy as looking at social media posts or mobile phone usage, everyone would be in the lending business. It's hard to build a sustainable differentiated underwriting capability."

Marketplace mechanics

Numerous platforms saw their vulnerabilities exposed during the initial economic fallout from COVID-19. At the same time, this did highlight the virtues of the survivors. According to Rengaswamy, they are – inevitably – specialists that combine core underwriting skills with domain expertise. BNPL and small and medium-sized enterprise (SME) financing are cited as examples; so too are B2B platforms that layer lending on top of specific industry needs or use cases.

These businesses are typically marketplaces that help SMEs negotiate opaque supply chains, sourcing raw materials more cheaply and efficiently or selling finished goods to distributors on more attractive terms. Financing is a logical next step because the platform can leverage its knowledge of a customer's commercial activities to underwrite transactions far more accurately than any other lender. Credit lines can even be issued against materials acquired through the marketplace.

Lending spurs economics as well. OfBusiness, one of a host of India-based B2B platforms, established a NBFC to provide financing to its core base of SME manufacturers in 2017. Since then, gross merchandise value has grown 12-fold, while financing is responsible for 40% of revenue and 60% of profit. It has been integral to the company reaching overall net profitability for the last three years.

In these limited ecosystems, investors see many of the same advantages – customer insights that translate into customer stickiness – that the larger platforms hope to achieve through scale. Ng of 500 Startups notes that closed-loop, data-driven lending makes for a more resilient portfolio. He sees similar businesses emerging in Southeast Asia, including eFishery, an Indonesian provider of smart feeding systems to fish farmers that offers fish futures based on data coming out of the ponds.

Use cases even stretch to financial management systems for families, whereby debit cards are issued to children, and parents can track spending activity via an app. There is scope for offering insurance and financial education products on top. "Will some of the general wallets build these features? Yes, but the fintech company is so entrenched, providing a fuller solution to the customer, to the point that it makes no sense to use anything else," Ng says.

For all the broad applicability, supply chain finance is regarded by most industry participants as the major near-term opportunity. Once again, success is conditional on building a deep moat by having a compelling value proposition underpinned by knowledge, underwriting skills, and competitive rates. Then it's a matter of how big the platform can become, and over what timeframe.

"Sitting in the middle of the high-quality data flow, there is a strong case to be made that you can really turn on lending. It's an interesting value proposition, but we have yet to come across companies, which we think can really scale on the lending slide," says Naik of General Atlantic. "This is a second iteration of digital lending, embedding financial products into a broader offering for merchants, and it has yet to fully play out."

SIDEBAR: Wallet share - Closed loop vs open loop

Indonesia has launched a national payment gateway and a universal QR code system to support the shift to a digital economy and make payments affordable. Merchants no longer need accommodate multiple wallets – the likes of GoPay, Ovo, and LinkAja are interoperable. But do they know that?

"QRIS is the switching technology between banks and wallets, but if I go to a merchant and ask to pay by QRIS, they say no. If I ask to pay by GoPay, they give me a code – and it's a QRIS code. Even my local supermarket has a printed QR code labeled BCA [Bank Central Asia] QRIS, but they just happen to call it GoPay. There is a branding issue," says Donald Wihardja, CEO of MDI Ventures.

MDI is the corporate VC arm of telecom carrier Telkom, which last year sought to create a default national e-wallet – LinkAja – by combining its existing offering with those of four state-owned banks. Wihardja notes that LinkAja's progress is shaped by its mandate to offer universal access. It has the largest transacting value and active customer base by virtue of a strong rural presence, but it ranks fourth nationally because commercial rivals harvest low-hanging fruit in the cities.

GoPay, which is controlled by local mobile on-demand services and payments giant GoTo, might be reluctant to destabilize the status quo. "It is not in their interest to publicly proclaim there is interoperable acceptance. They are trying to build closed-loop businesses where everything happens through them," says Ganesh Rengaswamy, a managing partner at Quona Capital.

Closed-loop ecosystems are criticized by some industry participants for introducing an additional source of friction – the wallet – in the payments process, whereas open-loop QR codes usually allow consumers to pay merchants directly from their bank accounts. They add that open loop is less likely to be disrupted by regulation, while the payoff in terms of usage and volumes is ultimately much greater.

Yet closed loop makes it easier for wallet operators to transition consumers to value-added services within their ecosystems. This is a critical issue because start-ups survive on tiny commissions from payments – while committing resources to QR code network rollouts and subsidies that encourage uptake – as they work towards the critical mass required to make value-added services viable.

Nevertheless, private equity investors have got comfortable with the economics of open-loop by carefully picking providers with profitable merchant-facing sidelines that offset costs elsewhere.

VNLife, which recently received a $250 million Series B round led by General Atlantic and Dragoneer Investment Group, runs Vietnam's largest interoperable cashless payment network. Its main revenue generator is a business that builds mobile apps for banks. Similarly, Philippines-based open-loop payments player Voyager Innovations is also the national leader in providing embedded financial technology solutions – typically payment gateways for online stores – to merchants.

In addition, these merchants can support the consumer wallet, notes Yong Yi Tan, a principal at KKR, which is an investor in Voyager. In this way, being open-loop helps because merchants place more value on propositions that work with Visa and Mastercard, as opposed to focusing on a QR code.

"We can leverage these relationships to strengthen the consumer wallet, so we do not end up burning as much cash," Tan explains. "For example, if we can convince our merchants to do a co-branded marketing campaign for our consumers, we can co-fund it and create a product that is relevant to the user base. On top of that, Voyager's offline network means it has touchpoints that many others don't have."

More on Southeast Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.