GP profile: Samena Capital

Conservative yet contrarian, Samena Capital has carved its own path prioritizing patience, trust, and transparency. A younger generation of leadership is guiding entry into a new digital landscape

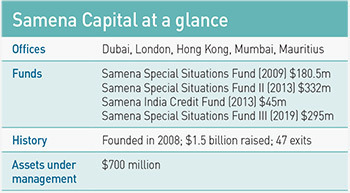

Who says the new Silk Road starts in China? Samena Capital, a private equity firm that has done things its own way since it emerged from the ashes of the global financial crisis, approaches the concept from West to East. Samena has raised about $1.5 billion of capital since its inception in London in 2008 for a thesis targeting the Subcontinent, Asia, Middle East, and North Africa, collectively the SAMENA region

Core operations were quickly relocated to Dubai to better organize an unconventional approach to fundraising and deal sourcing with a network of personal contacts in the Middle East. The push eastward saw bases in Hong Kong and Mumbai set up in due course. Assets under management (AUM) now stand at about $700 million, and some $707 million has been returned to investors over 47 full and partial exits. The focus is traditional business models in defensive sectors.

"We've not only seen our AUM grow over the years, but we've seen our capabilities grow in terms of hiring the right talent, making sure we have the right systems and processes in place, and that we're governed properly," says Chetan Gupta, a managing director at the firm. "Building an institutional structure was extremely important, especially from a DIFC [Dubai International Financial Centre] perspective. Today, we're one of the flagbearers of what can be achieved in this part of the world."

Samena was founded by Shirish Saraf, an Oman native who co-founded Abraaj Capital in 2002. He immediately brought in V-Nee Yeh, co-founder of Hong Kong hedge fund Value Partners, and Ramiz Hasan, founder of Japan-focused hedge fund Invicta, as co-founders. Gupta also joined at this time with a focus on private equity. There have been diversifications into various streams of asset management, notably an India-based credit business, but PE continues to represent more than 90% of AUM.

A unique approach to the asset class was evident as early as the establishment of Fund I in May 2009 with $180.5 million in commitments. This was supported by an uncommonly strong GP balance sheet of around $50 million, used to build different business lines and stage frequent networking retreats. High net worth LPs took stakes of 1-5% in the management structure. As Samena has grown, this structure has gradually conformed to industry standards. But the GP continues to position itself as a personal relationship-based principal management group.

Small beginnings

The initial drawdown for Fund I was only $40 million, and with the global financial crisis top of mind for LPs, the pressure was on not to make any mistakes in the opening moves. The first few transactions treaded lightly, with commitments in a range of $5-7 million.

"Our most important task was to be extremely certain of the kinds of investments we were making, not to deploy very large capital to those, and to have the opportunity to capture large upside," Gupta says. The plan was to wait and see how the first few investments unfolded before pressing any further. Luckily, one of them went on to be a contender for India's most successful consumer story of that decade.

The company in question was commercial vehicle and motorcycle maker Eicher Motors. Samena acquired an 8.5% stake in 2009 at around INR200 a share, paying $6 million in total. At the time, Eicher CEO Siddhartha Lal noted that Samena's structure and shareholders made it appealing as a preferred partner, especially in the context of pursuing cross-border synergies. The deal generated an IRR of 214% over a 23-month period and an absolute profit of $26.4 million.

In many ways, Eicher got the ball rolling for Samena. First, it validated a considerable focus on PIPE deals, based on the belief that many public companies across SAMENA are overlooked and have private-style shareholder ratios. Eicher was predominantly owned by its promoter and Volvo at the time of investment and hardly traded. Second, deep relationships and understanding of the investee team is crucial. The investor must know the operation as well if not better than the staff on the factory floor.

Early success also cemented a philosophy about relationship-driven deal sourcing and execution. Samena prefers to reference its circle of LPs, co-investors, and advisors over intermediaries chasing hot market trends. The firm claims that even as this network has institutionalized and subsequent vintages have dabbled in trendier sectors, the ethos has remained intact. Fund II closed in 2013 at $332 million and Fund III at $295 million in 2019, setting up what appears to be a new evolutionary chapter.

With the accelerating digitization of business models across industries – especially in the wake of COVID-19 – Samena has tentatively expanded into the technology and innovation space. The marquee investments here are Indonesian grocery delivery platform HappyFresh and Abu Dhabi-based music streaming provider Anghami.

Samena joined a Series B round for HappyFresh having sensed an undervalued opportunity. The company had raised $12 million for its Series A and the Series B would be a flat round due to some operational delays. Samena is now the largest shareholder with more than 20% and helped bring in the likes of Naver and Grab for a $30 million Series C in 2019. HappyFresh now claims to be the fastest-growing grocery platform in Southeast Asia.

Meanwhile, Anghami is set to reveal the Middle East as an overlooked start-up hub following an agreement to merge with a special purpose acquisition company (SPAC) sponsored by a group of Southeast Asian media professionals at a valuation of $220 million. Anghami, a freemium service with more than 70 million users, is set to become the first start-up from the Arab world to list on NASDAQ.

"They were validated, high-growth, and revenue-generating with clear paths to profitability and good management teams," Wassim Moukahhal, a managing director at Samena, says of the two investments. "We used the same methods of analyzing them as we would any traditional business, while understanding that technology models have different characteristics. They're actually the smallest checks we've ever written but given that they are going to be some of the better performers, we're clearly going to over-index on these sectors in the future."

A generalist first

The GP remains, however, a brick-and-mortar investor, a fact clearly reflected in its landmark transactions. The biggest of these to date is United Arab Emirates-based RAK Ceramics, the global leader in tile manufacturing. Samena took a 30% stake worth about $337 million at the time of acquisition in 2014. This was the first deal in a direct investment strategy, where balance sheet capital and fund deployments are blended with LP co-investment, targeting sizeable single-asset opportunities.

The most recent investment in this vein was India's Bloom Hotels in 2018. It was staggered, with the largest injection, a $50 million commitment, coming only months prior to the onset of the pandemic. The staggering of deployments is one of a number of risk mitigation methods that have been increasingly embedded into Samena protocol in recent years, along with strict oversight of how investment dollars are redeployed in portfolio company operations.

In the case of Bloom, growth spending during lockdowns and travel bans had to be cut to below income levels, so effectively no capital was lost. Money was also redirected into the back-end, a new CFO and chief information officer were hired, and a prestigious Mumbai hotel was acquired earlier this year at a favorable down-market price. The plan is to build out a technology-oriented, asset-light model that favors momentum in digital transformation over digital disruption.

"We're not an industry fund, a technology fund, or a VC fund – we will remain quite generalist. But as a traditional private equity fund, there are certain sectors you have to understand such as consumer and healthcare," says Moukahhal. "Technology has become like that, except technology applies to all industries in sectors like consumer and healthcare. If you're a traditional business without a technology platform, you're going to have issues."

Moukahhal and Gupta are the youngest members of senior management at Samena and effectively represent the future of the firm. In addition to being more technology-oriented, this future will also involve deeper roots in Asia. A Hong Kong presence was established in the early years with limited success. In 2016, a decision was made to restart with an experienced guiding hand in the form of Vincent Chan, founder of Spring Capital, who has made more than 50 investments in China.

Chan, who has taken the title of senior managing director and head of Asia, is not targeting mainland China, however. The focus is Southeast Asia and Hong Kong, especially where they can be plugged into broader regional themes. The standout deal to date is Vertus Medical, a private medical services provider in Hong Kong and Macau. Samena contributed $37.6 million to a $83 million round for the company in 2018.

The investment is perhaps most notable as Samena's best bet yet in terms of bridging the Middle East with Asia beyond the subcontinent. "Hong Kong is a bit too far, but Macau is a good stepping stone to Zhuhai and Zhongshan," Chan said, discussing Virtus' footprint. "With Hong Kong and Macau together, we can further strengthen how we penetrate the Greater Bay Area, which is part of Samena's whole Silk Road concept."

Social network

Virtus also hints at the intangible benefits of Samena's carefully developed networking tentacles. The company is led by Manson Fok, a medical doctor and son of Henry Fok, a longtime friend and business partner of Macau gambling magnate Stanley Ho. Pansy and Daisy Ho, daughters of Stanley Ho, were among the luminaries that frequented Samena's early board meetings.

The idea of such a convoluted connection might seem unlikely, but it is in keeping with Samena's family-style approach and would offer justification for the firm's apparently lavish general meetings.

Once held as often as 3-4 times a year, the strategic ownership group meetings (SOGMs) are now annual. The informal 3-4 day events can convene up to 300 people and cost around $500,000. Most importantly, the idea is to be transparent and candid with potential partners. The Bloom Hotels relationship was developed this way.

"It's an open platform, and we're not afraid that people are going to steal our relationships.," Chan says. "We believe the more open you are, the more deal flow you get. We bring in investors, family groups, and CEOs to meet our LPs. That's how we start relationships early. It can take 2-3 years to get to know each other, informally, before we do a deal. I was quite amazed when I joined because executing this idea is not easy – it takes a lot of courage to open yourself up."

The thinking here is to get the outsider's perspective; there would be no accounting for an insular approach to investment when the stakeholders span an expanse as vast as SAMENA. As Samena presses into its second decade of operation, there is added impetus to embrace this ideology to secure the long-term viability of the firm's lynchpin market: India.

In recent weeks, India has come to symbolize much about COVID-19's persistence as a social calamity and creator of rollercoaster market conditions. Statistics from the country's latest surge are dizzying. The total number of infections has passed the 20 million mark and the death toll has passed 222,000.

There's a risk of desensitization and a sense of being overwhelmed that comes with crises of this kind, which investors in India‘s long-term story must now confront. The question is whether that challenge will be handled only in consideration of immediate stakeholders and partners – or will a more inclusive and open style of investment help fulfill the promise of India and the rest of developing SAMENA.

"You will see a more accelerated convergence between urban and rural India simply because everyone is realizing that you can only progress when everyone progresses together," Gupta says. "I believe India will learn this lesson and move toward using technology and government platforms for the good of the larger community, at least incrementally. If this doesn't percolate down to who really needs it, the most impressive numbers about India's growth will be for nothing."

More on Southeast Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.