Southeast Asia VC: Waiting for the breakout

Fundraising has accelerated in Southeast Asia’s venture capital space in recent years, but the ecosystem remains fragile. Expansion will be difficult until GPs can prove the viability of the market to LPs

The close of Openspace Ventures' second fund last August at $135 million represented a validation of sorts. The firm had recently ended its affiliation with Indonesia's Northstar Group – changing its name from NSI Ventures to mark this newfound independence – and the fund close showed that it could inspire LP confidence without the backing of a major regional player.

For the GP's management team, the fundraise also showed that its Southeast Asia-focused strategy was gaining traction among investors. Returning LPs such as Temasek Holdings and StepStone Group were joined by new arrivals from Europe, Australia, Japan, and South Korea – markets where it was previously tough to source commitments for VC funds focused on the region.

"We're now at a point where we don't have any major geographical gaps in where we source our money, and the frequency of queries has picked up across the board," says Shane Chesson, co-founder of Openspace. "I was in Europe last week, and there are a lot more people keeping an eye on Southeast Asia VC, both from the perspective of returns and in terms of the impact it's having on the ground in many sectors."

Openspace is not alone in this regard. Several of its peers tell a similar story of growing appetite for Southeast Asia venture among a wider range of global LPs, for which the region promises attractive returns while representing less of a gamble than in years past. Managers are keen to convert this interest into commitments for larger funds – or dedicated growth vehicles – that will enable them to continue backing portfolio companies through mid to later-stage rounds.

Nevertheless, Southeast Asia remains a challenging market in many ways, particularly given the still-unproven exit thesis. In addition, the region is dominated by early-stage funds, and institutional investors remain unconvinced by growth funds. While the region's VC market is on a positive trajectory, tapping the opportunity requires clear lines of communication between GPs and LPs.

"There are managers that I have known through several funds and cycles, and that I feel comfortable underwriting even if the world gets difficult," says a managing partner at a European family office. "But with Southeast Asia venture it's such a new asset class that there aren't many managers I've been following in as detailed a way as I'd like, so it takes a while to pull the trigger."

The next big thing

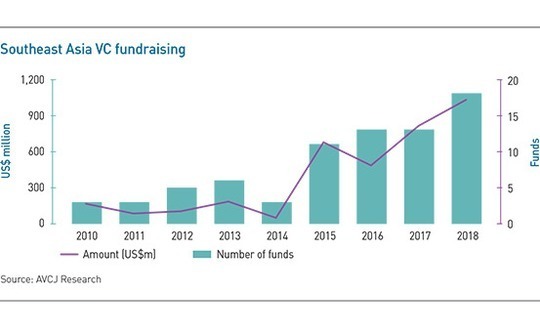

For many VC investors, the story of Southeast Asia fundraising was for years predominantly a struggle to overcome skepticism from LPs. According to AVCJ Research, from 2010-2014 just 20 VC funds reached a final close in the region, raising less than $700 million in all.

This narrative began to change in 2015, when 11 funds closed, including vehicles from such local managers as NSI, Beenext, and Venturra Capital, along with Southeast Asian branches of US-based 500 Startups and Japan's Cyberagent Ventures. The momentum continued to build in the following years; in all, since 2015 55 funds have reached a final close, raising nearly $3 billion.

Almost a third of this total was raised in 2018, with a significant portion for follow-on funds from Openspace, Venturra, and other established regional players such as Golden Gate Ventures and Cocoon Capital. So far this year $450 million has been committed across four final closes. A number of GPs are in the market, including Asia Partners, which reached a first close of around $70 million for its debut fund last month. It will focus on Series B and C rounds for technology companies in the region.

Fund managers report an expanding LP base across the board, but investors from North Asia have been particularly active in recent years. A number of Korean and Japanese investors have taken positions in Southeast Asian VC funds, looking toward the region's growing middle-class population in hopes of high-growth companies that are increasingly hard to find at home.

"In Indonesia, for example, more than 60% of GDP is domestic consumption – it's really the backbone of the economy. And the middle class is growing beyond fast," says Eddy Chan, co-founder of Indonesia-focused Intudo Ventures. "Meanwhile, Korean and Japanese investors are finding that assets in-country are being bid on very expensively. In the quest for growth, Southeast Asia is naturally going to stand out in their eyes."

Some North Asian investors have gone beyond standard LP commitment in search of deeper relationships. Over the past year Korea's Hanwha Asset Management, InterVest, and Korea Investment Partners (KIP) have either launched or closed funds alongside Golden Gate, Kejora Ventures, and Golden Equator Capital, respectively. In addition, EV Growth, a joint venture between East Ventures, Sinar Mas Digital Ventures, and YJ Capital, Yahoo Japan's venture arm, closed its debut fund at $200 million last month.

A common theme underlying these funds is the desire to invest in a burgeoning entrepreneurial ecosystem in partnership with a local operator who, it is hoped, can mitigate the risks of an unfamiliar environment. For corporate venture arms like YJ Capital, investing in Southeast Asia start-ups offers the additional benefit of potentially gaining access to innovative technology that can help the parent stay ahead of its domestic rivals.

"Two or three years ago when we were raising Fund V, there was very little appetite in places like Korea and Japan for any VC investments outside the domestic market," says Kevin Pereira, head of investor relations at Vickers Venture Partners. "Now we're seeing them come out of their own countries with a shopping list and going into Southeast Asian markets, where they're performing the same function as venture capital, and sometimes working with venture capital."

These vehicles are also seen as helping to meet a growing need in Southeast Asia's VC market: the absence of dedicated funds providing Series B and C round for start-ups that need support to reach the next stage of growth. EV Growth is specifically targeting this opportunity, as are the Hanwha, KIP, and InterVest partnerships.

JinA Bae, head of corporate venture at Hanwha, told the AVCJ Indonesia Forum in April that 180-200 start-ups will likely be seeking B and C funding in the next two years. This assumes that only 10% of those that raised seed and Series A rounds in 2016-2018 make it through to the next level. Only a handful of regional funds currently capable of meeting this demand.

Other players targeting the later-stage funding demand include Burda Principal Investments, the investment arm of European technology and media company Hubert Burda Media that established its Singapore office in 2017. The firm's strategy includes LP commitments to early-stage funds such as Kejora, Golden Gate, and Jungle Ventures that can provide it a pipeline of potential future deals, along with direct investments in companies such as e-commerce platform operator Zilingo.

"Southeast Asia was still in the early stages of its ecosystem development, and while there was a good amount of activity in seed and Series A rounds, there was still a gap in terms of funds that were looking at later-stage investments," says Albert Shyy, who joined Burda from Gree Ventures to head the Singapore office. "We felt that we could be a relatively early mover in that space."

Questionable remits

However, developing the late-stage opportunity may be more difficult than expected. Though several fund managers have made the case for later-stage vehicles, LPs express doubts about backing them for a market like Southeast Asia. Many investors feel that the utility of these funds is questionable in a region that is still seen as lacking a viable exit pipeline, and where expectations for financial returns are driven more by comparisons with other markets than by on-the-ground experience.

"In Europe 10-15 years ago, several early-stage managers were raising growth funds, and that was mostly driven by the GPs," says the family office managing partner. "I don't think as LPs we thought we would really like a growth fund; it was more the GPs saying, ‘We've got these companies now that we know are pretty good, and yet we can't carry on investing in the follow-on rounds.'"

This skepticism is frustrating for GPs, both those seeking to raise growth funds and those that remain focused on the early stage. For the latter group, the development of more local growth funds could help them focus on supporting start-ups at the stage to which they are best suited. While it is possible to cobble together a consortium of early-stage funds to back follow-on rounds, these investments tend to lack a clear leader. Moreover, GPs that take part can find themselves stretched to provide a level of support for which they didn't originally plan.

LPs largely remain sanguine about the scarcity of dedicated growth vehicles, pointing out that entrepreneurs without access to dedicated late-stage vehicles can find other ways to support their continued growth – as some of the region's most successful start-ups have already demonstrated.

"Just because there's a relative lack of later-stage VC funds doesn't necessarily mean there's a lack of later-stage venture capital – we've seen other types of investors, particularly strategic investors, quite happy to be supplying that support," says Wen Tan, co-head of Asian private equity at Aberdeen Standard Investments. "At the extreme you're seeing it with the likes of Go-Jek and Grab, which have a pretty diverse global set of investors, not many of which you would classify as late-stage VC funds."

In addition to strategic investors, later-stage private equity firms may occasionally fill the gap as well. For example, Warburg Pincus has backed several Southeast Asian start-ups at various stages of development, from giants like Go-Jek to Indonesian tax compliance business OnlinePajak and Singapore-based visual technology developer Trax.

"Once you're at that stage with a quality company, the global capital pools will start to pay attention," says Openspace's Chesson, an early investor in Go-Jek. "Go-Jek was a classic case, where at Series C and D we had DST, KKR, Warburg Pincus, and a lot of other investors with seriously deep capital wanting to put that money to work in a great company."

Growth imperative

While PE funds and strategic investors can help to fill the gap temporarily, most members of Southeast Asia's VC community believe there is ultimately no substitute for dedicated growth investors. Strategic players are considered more focused on benefiting their parents than ensuring the optimal financial returns for earlier investors, while private equity firms may not understand the needs of a company that is still at a relatively early stage of development.

Without support from LPs for later-stage funds, there is a danger that the region's nascent venture capital ecosystem could stagnate. Market observers largely dismiss this concern, however, pointing out that the market has expanded to fill shortfalls before.

"While I would still argue that we could use more capital at the Series C stage and later, we have seen the gap in the market narrowing over time," says Burda's Shyy. "When I started at Gree there was actually a Series A gap in Southeast Asia, and Gree was considered one of the relatively few investors that were able to write Series A checks."

Most fund managers believe institutional investors will be more willing accommodate later-stage vehicles once they are comfortable with prospects for portfolio companies, particularly from an exit perspective. GPs can appeal to investors by promoting their experience in this regard. For example, the founders of Asia Partners include Nick Nash, who oversaw Sea's 2017 IPO, and Oliver Rippel, who previously worked at Naspers when it sold India's Flipkart to Walmart last year.

"I think that moving forward, LPs and entrepreneurs will look more at experienced GPs that can not only help businesses scale, but also lead to a successful liquidity event," says Rippel. "We're going to see that story repeat in Southeast Asia, as it already has in the US, China, and other markets."

More on Southeast Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.