Indonesia exits: Unmet expectations?

Indonesia has become a source of frustration for LPs that want to see more exits. A weak currency, slower growth and rising competition aren’t helping GPs as they seek to deliver the required returns

The fortunes of Multistrada Arah Sarana, Indonesia's leading tire manufacturer, are linked to those of the rupiah. In 2011, with the currency trading below IDR9,000 to the US dollar, Multistrada generated $325.9 million in revenue and booked a profit of $6.9 million. Over the next three years, the rupiah plunged more than 50%, ending 2015 close to IDR14,000. Multistrada's revenue fell by more than 25% and its profits evaporated. The company, which operates in US dollars, bemoaned the role of the exchange rate in pushing up input costs and constraining sales value in the local market.

By 2017, a turnaround was underway. The currency situation hadn't improved, but Multistrada was helped by a more stable economy and a focus on building market share. Revenue rebounded and the company returned to profitability in the first nine months of 2018. Its stock has gained 135% since last September. In January, Michelin bought an 80% stake in Multistrada for $439 million in cash.

This facilitated an exit for Northstar Group – but there is no escaping the impact of a depreciating rupiah. The GP received IDR1.15 trillion ($81.7 million) for its 14.91% interest, having acquired a 20% position in October 2011 for IDR691.6 billion. Its cost of capital was $78.6 million in US dollar terms, based on an exchange rate of IDR8,800. If the rupiah was still at that level, rather than IDR14,100, Northstar would have made $131 million. That equates to a 1.7x return versus a 1x return.

"The decline in the rupiah means managers must run a lot faster just to stay on the treadmill," says Marc Lau, a managing partner with fund-of-funds Axiom Asia. "But if the fundamentals are good and managers are picking companies that are creating value for customers, taking market share, and growing in local currency terms, investors who stick with those guys will be rewarded."

Indonesia has faced strong headwinds in the past few years, ever since the end of the commodity super-cycle and talk of US quantitative easing in 2013 conspired to peg back a booming economy. Beneath all that, GDP growth is still above 5%, consumption is robust, demographics are favorable, and much is expected of an emerging middle class. But some LPs are losing patience.

"You are getting the same consumption upgrade story in other markets, why go to Indonesia? There is no proof of concept," asks one institutional investor, who has exposure to Indonesia through pan-regional and single-country managers and describes it as the worst performing geography in his portfolio. "There are no proven managers. There are hardly any exits. The rupiah is worse than the rupee in terms of volatility. It doesn't make sense – it's like diversification for the sake of it."

The community of local private equity managers has already shrunk. Northstar Group and Saratoga Capital are the sole survivors from before the 2011 watershed when interest in Indonesia took off; and only Northstar currently has a fund with capacity for new investments. The two GPs that closed their debut funds post-2011, Falcon House Partners and Capsquare Asia Partners, both have little to show so far in terms of realizations. Investors want them to demonstrate that the consumer story pays out.

Big versus small

Exits are not impossible in Indonesia and their scarcity partly reflects the fact that relatively few initial investments are being made in the traditional private equity space. According to AVCJ Research, only a handful of realizations take place each year and they tend to be dominated by intermittent large-cap transactions that invariably take place in the capital markets.

The ramp-up in Multistrada's stock price over the past six months reflects a broader revival in public equities. CVC Capital Partners took advantage of the upswing last week, realizing proceeds of IDR4.1 trillion by offloading the bulk of its stake in sports retailer MAP Aktif Adiperskasa. The GP is shortly expected to tap the capital markets yet again, having invited applications from investment banks to run an IPO process for personal care products manufacturer Softex Indonesia.

The Softex offering will likely follow the same format as MAP Aktif and another CVC portfolio company, broadband and cable TV provider Link Net. When Link Net and MAP Aktif listed in 2014 and 2018, respectively, the initial public free float was tiny because limited liquidity on the Jakarta Stock Exchange makes it difficult to raise significant amounts of capital in one go. In each case, the PE firm's major exit event was delayed until the stock was stable and foreign institutional investors were ready to come in. A similar approach was taken for Matahari Department Store, although it was listed before CVC invested.

Smaller companies are not afforded the luxury of these so-called re-IPOs. The consensus view is that an offering of at least $100 million is required to get institutional investors interested, but some industry participants say the bar is being raised.

"Investment bankers are talking higher numbers – you need to be a $700 million company with over $200 million of liquidity in the stock for foreign long-only fund managers to participate meaningfully. They want to be able to put in a $30 million order and believe they can get out when they need to get out," says one local GP. "Historically, a lot of Indonesian IPOs haven't been successful because of this liquidity issue. PE investors thought the minimum size for an IPO was at a lot less."

Link Net has a market capitalization of IDR12.9 trillion and its 30-day average trading volume exceeds 627,000 shares. Kino Indonesia, a fast-moving consumer goods company, raised approximately $62 million in its offering in 2015 and is now valued at IDR3.5 trillion with a trading volume of 167,660 shares. Northstar made a pre-IPO investment and still holds 153 million shares. There are doubts as to whether the market is deep enough for GPs in this kind of position to divest their holdings.

This does not necessarily mean investors are stranded. Sunata Tjiterosampurno, Northstar's co-CIO, notes that IPOs present two routes to exit. While some companies can grow their market capitalizations to the point that share placements to global institutional fund managers are a realistic goal, others use the public markets as a platform for trade sales because it is more tax efficient. He didn't comment on Kino specifically.

Any capital gain on the sale of unlisted assets by a non-resident investor is subject to a withholding tax of 5% unless there is tax treaty coverage. For resident investors, capital gains are treated as ordinary income and taxed at 25%. Once a company is listed, share sales are subject to a tax of 0.1% of the transaction value, with founders paying an additional 0.5%. "That's why many small companies, if there is an intent to divest shares, do a listing first and equity investors come in later," adds Larry Sutikno, CEO of Indonesia-based boutique investment bank Avantgarde Capital.

Who's buying?

Trade sales, in a public or a private markets context, attract reasonable strategic interest; whether it is local or foreign depends on the sector. Saratoga Capital's energy and infrastructure assets – Baskhara Utama Sedaya and Paiton Energy, operators of toll roads and power plants respectively, have both been sold in the last 24 months – went to Indonesian buyers. Consumer or industrial businesses tend to end up in foreign hands, as evidenced by Northstar's recent exits from Multistrata and BFI Finance.

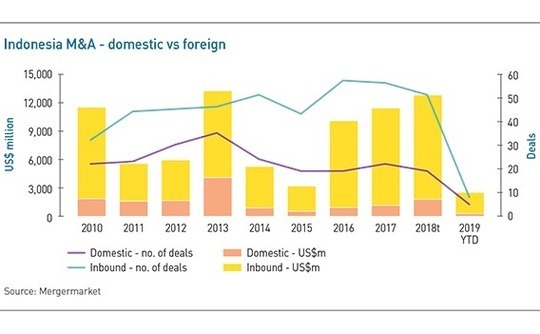

If private equity follows broader M&A trends, foreign investment activity easily outstrips domestic. Last year, inbound capital was responsible for $10.9 billion out of the $12.7 billion transacted in Indonesia-based assets. It is a similar story in terms of deal volume, with foreign investors announcing 51 transactions in 2018 compared to 19 for their local counterparts. On both counts, the percentage split has been largely consistent over the past eight years.

Larger managers agree it is a case of when, not if, these transactions take hold, but they stress the evolution will be gradual. "The whole theme of secondaries in Asia, and especially Southeast Asia, has not been strong, and that's reflective of the lack of market maturity. Today we see the odd one, but it's not a major source of deal flow" says Terence Lee, a director at KKR. "As time goes on, as we see more sponsor activity and as sponsor investments mature, there will be more of this. It is a positive development, both in terms of giving us another way to make investments and to exit investments."

For now, though, pricing remains the biggest obstacle to getting deals done. While the classic situation involves the patriarch of a family-owned enterprise refusing to countenance a sale below a certain price point because he remains so attached to the business, the deadlock extends to PE-to-PE transactions as well. "A PE firm will be looking to execute due diligence and we often hear, ‘Get ready, we have a hard start,' and then there is silence for two months. It turns out that, one way or another, deal negotiations fell over on pricing expectations," says David East, a deal advisory partner with KPMG in Jakarta.

In some cases, it is a dilemma around timing in which the rupiah features strongly. One LP expresses his frustration at being told by local managers that there are offers on the table for companies, but they want to hold on a bit longer because they feel there is more value to be extracted from the portfolio. The GP perspective is why sell in a sub-optimal environment if a company's revenue and EBITDA are still growing at a fast clip. In this way, Indonesia's prolonged macroeconomic difficulties could be blamed for pushing out holding periods.

"The structural dislocation in the currency, particularly last year, caused people to pause. But the fundamentals are still strong – a low debt-to-GDP ratio, low external debt levels, great demographics, a current account deficit moving in the right direction. Why not wait it out and let the currency stabilize?" a local manager asks.

Operational angle

Private equity firms have their own methods for addressing currency risk – and hedging generally isn't one of them, given it is neither easy nor cheap. Capsquare, for example, is said to aim for a 30% local currency return on each investment and factors in a 5% per annum depreciation assumption. This is not unreasonable. Even though the rupiah fell to IDR15,228 against the dollar in October 2018 – a 10-year low – by year-end it had recovered sufficiently that depreciation on a 12-month basis was just 7%. But the best way to deliver performance is to ensure portfolio companies grow faster than the rupiah falls.

The challenge for GPs is that the market dynamics have changed significantly in the last eight years. With Indonesia still gripped by the aftereffects of the Asian financial crisis, between 1998 and 2006 there was hardly any investment in the economy. Industries stood still. When the first private investors returned, they found themselves in wide open spaces. By 2011, with regional funds reengaging and a host of country funds looking to launch, the easy days were long gone.

"What helped characterize the success of many of the early deals was they were made at a time when capital was scarce, and valuations were structurally lower," says Brian O'Connor, a managing partner at Falcon House. "It's a lot harder now. Private equity firms are not only competing against each other, but can also be up against banks, the credit markets, the IPO market, and other forms of local liquidity."

In a climate of abundant liquidity, investors that entered at higher valuations than in the previous cycle must do more with their portfolio companies. Moreover, the macro tailwinds they once relied on are no longer blowing consistently. "If you were buying things in the vintage that was expensive, when everyone was falling in love with the Indonesia story, then you could be in difficulty, given the slowdown in consumption and rupiah depreciation," says Brian Lim, a partner with Pantheon. "Managers might have a fair amount of running to do just to wash their faces."

This might explain the renewed emphasis on operational support, on top of the oft-repeated mantra that private equity investors must select the right industries, companies, and management teams. "You cannot just rely on having 30% topline growth," says Tjiterosampurno of Northstar. "You must also make sure companies are efficient on unit costs and improve productivity because the landscape is becoming more competitive."

This view is echoed by other local managers. Capsquare, for its part, seconds team members to portfolio companies on a full-time basis in C-suite roles. One of its food and beverage holdings has more than doubled its store count over the past five years. However, Ridwan Budijono, Capsquare's co-founder, notes that the geographical footprint is not the only thing to have grown. EBITDA margins have also increased on the back of efficiency initiatives.

"A lot of the time in emerging markets you have gaps in the skillsets of management teams. It takes time to find new people, and once they are in place, for them to get going. By having our people involved daily as part of the executive management team, we are trying to shorten the time in which value creation occurs," he says.

Judgment day

If this is Indonesia private equity 2.0, then managers will be judged on it. The issue is when. One GP, talking up the possibility of an impending stream of exits, suggested AVCJ wait nine months and then run this story. The jaundiced LP response is we've heard that before. When asked to explain why they feel Indonesia has underperformed, several institutional investors question the viability of middle-market strategies. Can smaller companies, especially in the consumer space, be scaled up fast enough to appeal to trade buyers? Are larger businesses better positioned to weather external economic pressure?

While unwilling to write off Indonesia completely, they are unsure whether it warrants a place in their portfolios, short of an allocation to a pan-Asian manager. For some, this uncertainty extends to Southeast Asia as a whole. Axiom's Lau takes a different view, arguing that allocations to emerging markets offer different risk-reward trade-offs and it is possible to arrive at a regional balance that includes Indonesia. He warns against ignoring the long-term perspective in favor of interim snapshots.

"I remember from the Asian financial crisis, it is easy for people to call it quits. Sticking with something when the macro winds are against you and returning capital takes a phenomenal amount of effort that needs to be recognized," Lau adds. "I often ask people if they are the pig or the hen in the breakfast. These country managers are the bacon, committing their own skin rather than just laying eggs. They live and breathe Indonesia, and they have to make it work."

More on Southeast Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.