Vietnam IPOs: A bigger bourse

A string of large-cap IPOs has brought international investors and credibility to Vietnam public equities. Despite a few local peculiarities, the market is on a path towards modernization

When Warburg Pincus paid $200 million for 20% of shopping mall operator Vincom Retail in 2013, a listing on the Ho Chi Minh Stock Exchange (HOSE) did not feature prominently among the likely exit scenarios.

"You want to have multiple exit options and one was an IPO, but I would have wagered there was a greater chance of it being an international listing than a domestic listing. For the first two years that was probably still the right mindset," says Jeffrey Perlman, head of Southeast Asia at Warburg Pincus. "People started to wake up to the Vietnam story in 2016 and the momentum followed. By the time VietJet listed we knew the domestic route was the best option."

Low-cost airline VietJet raised $167 million in February 2017, a record for a domestic listing. That record has since been broken several times, including twice by Warburg Pincus portfolio companies. First Vincom Retail raised $740 million, then Vietnam Technological & Commercial Joint Stock Bank (Techcombank) reeled in $1.28 billion, including the sale of treasury shares. Top spot is now occupied by Vinhomes, the country's largest residential property developer, on $1.35 billion.

The IPO-friendly markets have prompted various PE investors to consider their options. PENM Partners, for example, has already listed one company and has indirect exposure to Techcombank. Mekong Capital is assessing the prospects for Ben Thanh Jewelry and pawn shop chain F88, both of which are capital hungry and might benefit from access to debt capital markets.

The longer-term payoff is for the HOSE – its reputation among investors, particularly foreign institutional players, as a market that can make things happen. "It is becoming a proper modern stock market," says Bill Stoops, CIO at Dragon Capital. "It has long since outgrown its frontier designation, just look at the market capitalization to GDP and trading volumes. It is playing in the same league as Malaysia, Thailand and Indonesia."

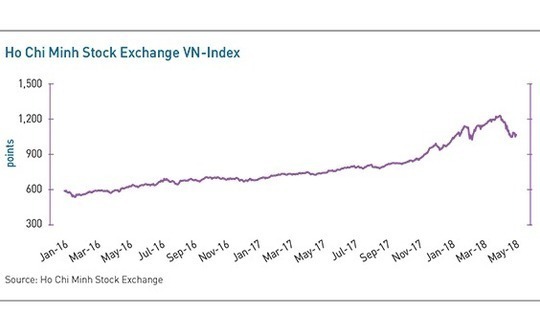

Riding the wave

Needless to say, the wave of listings has coincided with public market valuations reaching new highs. The Hose VN-Index began 2016 at approximately 570 points. Twelve months later it had surpassed 1,000 points and was on its way to a peak of 1,200 in early April. There followed a correction of around 15%, which some industry participants put down to the market digesting the new supply that has come online. Others argue that the current pricing levels are unsustainable.

"It is totally disconnected from how companies have been valued in Vietnam generally," says Chris Freund, a partner at Mekong. "With the exception of 2007-2008, I've never seen anything like it. Deals are being done at 40x P/E [price to earnings], normally by strategic investors from elsewhere in Asia, and they are investing in companies that are growing 10% a year. There's more downside than upside in that. The average P/E is Asia used to be 14x and Vietnam traded at a discount to it."

No one wants to call a top to the market and there are reasons for investors to be optimistic, albeit perhaps not to the extent that current valuations suggest. Vietnam's economy is stable and healthy, while its banking and real estate sectors, which are responsible for the bumper listings, are both looking strong. On top of that, the government has a clear privatization agenda.

Indeed, the IPOs were supposed to be dominated by SOE equitizations. Dragon Capital manages nearly $4 billion in listed equities in Vietnam, regularly backing new listings as a cornerstone investor and subscribing to share placements. It felt that more could be done in these two areas and so established a $300 million co-investment platform through which clients could deploy capital alongside the funds.

"We started out looking at SOE IPOs because that was the great hope of the market, the government was going to privatize like crazy and that was how the market would broaden and deepen," explains Stoops of Dragon Capital.

At the end of 2016, the government moved to encourage SOE listings by ending the practice of companies completing over-the-counter IPOs where there was no obligation to list shares. It instructed SOEs to begin trading on the Unlisted Public Company Market (UPCoM) – essentially a halfway house to a full listing with reporting requirements but minimal liquidity – within three months of their IPOs. Main board debuts would come a year later.

There were three big SOE listings at the beginning of 2017, with Binh Son Refining & Petrochemical, Petro Vietnam Power Corporation, and PetroVietnam Oil Corporation. However, the private sector has since taken over, led by Techcombank and Vinhomes, and these deals have proved most lucrative for Dragon Capital. By the end of April, the co-investment platform had an IRR of 165% and there are plans for another fundraise because it is running out of money.

In the case of Techcombank, Dragon Capital, GIC Private and Fidelity Investments were part of a cornerstone investor group that covered three-quarters of the offering, which underlines the significance of the role played by concentrated pools of foreign capital in these large IPOs. It is necessary given domestic institutional participation in public equities is still relatively limited.

IPOs and IEOs

However, foreign involvement is not restricted to the IPO process itself. Duc Tran, a partner with Allen & Overy who has worked on numerous listings, draws a distinction between IPOs and what he describes as initial equity offerings (IEO). "When new shares are issued in an IPO there's a lock-up of up to one year," he says. "Many overseas investors don't like that, so we structure it in a way that they buy secondary shares before the IPO. As a result, the lock-up does not apply."

Avoiding the lock-up is just one aspect of the IEO. From the target company's perspective, it is also a means of raising expansion capital. The proceeds from the share placement to foreign investors are used by the sellers to subscribe to new equity. These shares are subject to the lock-up, but the existing investors who participate in these transactions often already have sizeable positions in the company, so restrictions on a small portion of their holdings are less of an issue.

For example, VinaCapital and Dragon Capital together acquired 30% of FPT Retail, operator of Vietnam's second-largest mobile phone retail chain, in August of last year. The company listed in April and the stock is trading at a premium to the IPO price. VinaCapital's position is worth about twice what it paid for it, and unencumbered by a lock-up, the private equity firm started paring its stake last week.

"A pre-IPO placement that takes place six months before a listing is common," observes Hans Christian Jacobsen, a managing partner at PENM Partners. "It is normally existing shareholders and one or two new financial investors who want to get a foothold before the company floats. A lot of companies do it to raise capital for expansion purposes. The way IPOs work here, not a lot of money is raised from new issues – it is existing shares that are traded."

Techcombank topped up its IPO by selling $362 million in treasury shares, but apart from that, all the mega listings have been purely secondary share sales. The reality is that companies coming to the exchange, big or small, are not looking to raise new equity capital: either they have already met their needs through a pre-IPO placement, or they are in strong financial health.

Industry participants say this is a result of a regime that means it is far easier to list existing shares than issue new ones. "This quirk in the market exists because the regulations on book-building don't exist so if you do a genuine public offering you have to do it through an uncontrolled public auction process" says Foster of Freshfields. "They are planning to change it, but things work slowly."

It serves as a reminder that, even as international investors target Vietnam public equities in greater numbers, the market is still adjusting. VietJet became the first domestic offering to achieve an international syndication because disclosure policies were altered to meet international standards. Another item on foreign investors' wish lists is the 45-day settlement period for IPOs, which they would like to see shortened in line with other markets in the region.

"Each of the last two IPOs is now a top-10 listed company and investors will jump through hoops to get exposure to them," says Perlman of Warburg Pincus. "When you start bringing through the next wave of companies, which might include the 50th largest in the country, maybe investors will look at the structure, take a pause, and that could accelerate reforms like shortening the listing period."

More on Southeast Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.