Fund structuring: Change at the margins

While the Cayman Islands remains the go-to jurisdiction for PE firms seeking a domicile for Asia-focused funds, investor demand and regulatory remit mean structures are now more carefully considered

The fallout from Lone Star Funds' investment in Korea Exchange Bank (KEB) has been protracted and messy. What started out as a turnaround story in 2003 descended into accusations of stock price manipulation, the private equity firm being ordered to relinquish control of the bank, and its former Korea head receiving a prison sentence (it was appealed).

Lone Star exited to Hana Financial in 2011, but felt that "illegal" interference by the government – including a refusal to approve a string of prospective buyers for the KEB stake – had resulted in billions of dollars in damages to fund investors. The GP initiated arbitration proceedings against the Korean government in 2012 and against Hana in 2016.

One part of Lone Star's complaint is that 10% of proceeds of the KEB sale were withheld to cover capital gains taxes. The authorities decreed that the Belgium-based entity through which the investment was made would not be exempted under the South Korea-Belgium double taxation agreement (DTA). They looked through the Belgium entity to the Cayman Islands-domiciled fund behind it, which had no DTA protection.

Last December, another Lone Star investment routed through Belgium was afforded the same treatment by Korea's Supreme Court, and although rulings made by different bodies have at times been conflicting, the uncertainty has set off alarm bells. Some pan-Asian private equity players have opted to domicile their latest funds in Canada rather than Cayman, with "Korea risk" cited as one of the contributing factors.

"I've advised on at least two pan-Asian funds recently that decided to replace Cayman with Canadian and Delaware partnerships," says Adam Williams, a partner for financial services tax at EY. "Apart from a general perception of LP preferences, this has provided a more robust structure for certain investment jurisdictions. For example, some fund managers have taken the view that a Canadian limited partnership is more transparent under Korean law and therefore, the Korean tax authorities may be more likely to look through to the ultimate investors."

Not the norm

The switch to Canada by no means represents a collective decision. Mark Cummings, a Hong Kong-based partner at Walkers, notes that several clients managing funds with Korean exposure have reassessed their tax structuring in the wake of the Lone Star cases, but almost all opted to remain with Cayman. "It's mainly due to investor familiarity," he says. "They accept they may have to take a tax hit and calculate that against the gains they may make in certain markets."

Familiarity comes up repeatedly when discussing Cayman as a fund domicile. Investors typically want zero tax at the fund level, flexibility and ease of use when seeking out a jurisdiction for this purpose, as well as a strong network of local service providers who can be relied upon to get structures right. Cayman delivers on all these fronts, and has done so for years.

However, broader tax and regulatory developments – notably that anti-avoidance mechanisms already impacting the choice of jurisdiction for downstream investment structure could extend upwards to the fund level – are prompting GPs to consider their options. Even if it doesn't drive Asian managers away from Cayman, offshore structuring is becoming more nuanced.

"A lot more attention is being paid to the governance and operational protocols of a fund – not just by GPs but by LPs as well," says Darren Bowdern, a tax partner with KPMG China. "They are looking at how the investment committee reviews material and makes decisions, ensuring that a manager doesn't trip up in a jurisdiction by doing more than it should be doing."

The strength of Cayman's competitive position in the international funds market should not be underestimated. There were more than 20,100 active limited partnerships in Cayman as of the end of 2016, more than double the number from seven years ago, according to the government general registry. Closed-end funds are unregulated so there is no way of knowing how many are involved in private equity, but the total far exceeds that of other jurisdictions.

"For Asia-based managers, going anywhere other than Cayman, or possibly Luxembourg, would be a long shot," says Lorna Chen, a partner at Shearman & Sterling. "Starting a few years ago, people began to question the reputation of Cayman but from a business perspective it is still the best choice. Until there is a viable replacement, the suggestion to switch fund jurisdiction away from Cayman may not be considered mainstream."

Luxembourg appears on the radar for reasons of distribution and LP comfort. First, the introduction of the EU's Alternative Investment Fund Managers' Directive (AIFMD) has made it more difficult to market funds in Europe. The easiest option is to establish a fund entity within the EU – Luxembourg and Ireland being the most popular jurisdictions – and either manage it directly or appoint a third party to perform this function. Cost appears to be the major barrier to this catching on in Asia.

As for LP comfort, some investors in Europe are fundamentally opposed to entering Cayman funds for reputational reasons – or in certain countries they might be penalized by their local regulators for having exposure to the jurisdiction.

For example, when L Capital Asia launched its second fund in 2013, LVMH was a significant LP and expressed concerns that using a Cayman vehicle would look bad. As a result, it and some other European investors went into the fund through a parallel Singapore limited partnership, according to a source familiar with the situation. More recently, one fund formation lawyer recalls using a Singapore entity for an Asia fund because the LP base was dominated by European development finance institutions and they insisted on using an OECD country.

Singapore is increasingly seen as a viable option for Southeast Asia and India-focused managers, although not necessarily as the sole jurisdiction. An assortment of parallel or feeder structures might be employed based on the needs of different investors, with the likes of Jersey, Guernsey and Delaware joining Luxembourg, Ireland, Canada and Singapore in the mix. However, the unifying element is often still Cayman – and that is where all the negotiation about economics takes place.

"Singapore master funds remain popular amongst managers in Southeast Asia looking to tap into the tax treaty network, particularly where there is an Indonesia or India investment focus, but we are still seeing Cayman dominate at the investor facing feeder fund level. Cayman enjoys a significant amount of investor trust, particularly if managers are looking for distribution into north Asia and the US, and it continues to raise the least number of jurisdictional red flags amongst investors," says Thomas Granger, a partner at Walkers.

The BEPS factor

A key consideration in the enduring popularity of this arrangement is likely to be the BEPS initiative, conceived to stop investors exploiting gaps in the tax system to artificially shift profits to low or no-tax jurisdictions. Areas of focus include treaty shopping, or the use of offshore structures purely to take advantage of the tax breaks offered under DTAs. If a principal purpose test finds that a structure has been set up to obtain a tax benefit, DTA benefits would be denied.

One of the key questions is whether a fund established in Cayman that invests through special purpose vehicles (SPVs) in another jurisdiction would pass the principal purpose test. It is generally accepted that the more substance – people and operations on the ground – an investor has in this jurisdiction, the better the chances of passing, i.e. authorities would not look through the SPV to the fund structure, allowing DTA benefits to be retained. But what constitutes enough substance?

The OECD published a consultation paper on this issue in 2016 and followed up this year with case studies intended to illustrate its position. Several tax advisors argue that the situation remains vague – but they don't necessarily agree on whether there are grounds for altering structures at the fund level as well as the SPV level.

"There has been a lot of discussion in recent years about looking to the regional holding company level or looking through to the fund or through to where the ultimate investors are located," says EY's Williams. "The OECD hasn't come to a definitive conclusion as to which was the preferred approach for PE funds. But, big picture, if you have your fund, regional holding company and advisor in one location, that's a pretty good defense against treaty-shopping claims."

KPMG's Bowdern, meanwhile, doesn't believe the impact of BEPS will be so far-reaching. "The fund vehicle is a collective investment scheme, and from a fund perspective, apart from the issue of substance when attempting to access treaty benefits, BEPS is a transfer pricing issue – it is about aligning revenue and profit with where the value is being created," he explains. "BEPS is very relevant with respect to allocating management fees to where services are being performed, but it is also relevant to the issue of substance at structures underneath the fund."

In short, neither advisor suggests that the combination of a fund structure in Cayman and an SPV elsewhere would undermine DTA access, but they have different views on the future regulatory risk and whether it warrants a considered response from managers right now.

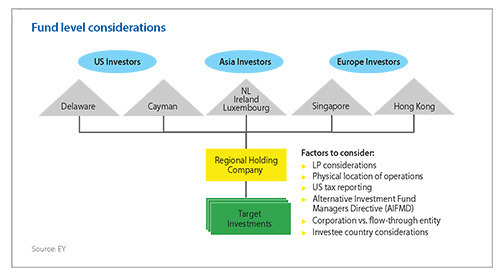

What's beyond dispute is that the traditional approach of establishing a Cayman limited partnership and then setting up SPVs in Mauritius, the Netherlands and Hong Kong to make investments in India, Korea and China, respectively, is no longer fit for purpose. A single regional holding platform in a jurisdiction with an extensive DTA network and a solid financial services infrastructure is increasingly seen as the preferred model. Singapore and Hong Kong are the obvious destinations.

Singapore has positioned itself to benefit from this development. Managers are able to set up a structure that sits below the Cayman vehicle and there are set criteria – minimum annual local business expenditure and having investment professionals on the payroll locally – to qualify for tax residency. There is also the option of domiciling the fund itself in Singapore.

"The world is now being more driven to substance-based structures and in Singapore you have genuine fund managers as well as genuine service providers and bankers and other institutions supporting the fund itself. If everything supporting the fund vehicle is in Singapore or more substantive than in Mauritius and Cayman, then managers will ask why not have the fund itself in Singapore," says Anuj Kagalwala, asset and wealth management tax leader at PwC Singapore.

By all accounts, while these questions might be asked, PE firms have yet to embrace the structure in significant numbers. They still might, particularly if it becomes clear that integrating tax structuring into the fund itself is better from a regulatory compliance standpoint than doing it on the levels below, but advisors observe that this is not the only consideration.

Familiarity once again comes to the fore. The Singapore fund structure isn't surrounded by a lot of case law and jurisprudence, and hasn't been tried and tested through the highs and the lows of the market. "If you are a manager and you have 30 minutes with an LP, you want to spend that time explaining why your fund will be successful. You don't want to spend the first 15 minutes discussing the merits of a particular jurisdiction," says Paul Christopher, a partner at Mourant Ozannes.

Another factor is consistency of treatment across downstream investment jurisdictions. While there is a sense that a Singapore-based fund has a better chance of securing treaty benefits, the question of substance varies country by country within Asia. "If you have people on the ground in several countries in Asia, you might have substance, but it depends what they are doing and where you are investing," adds KPMG's Bowdern.

Size matters

Complexity of structure is ultimately a function of size. A China mid-market manager doesn't have the resources to invest in multi-jurisdictional structures and that's fine: most, if not all, of its portfolio companies are based in a single market, while its LP base is likely to be reasonably concentrated. Cayman and Hong Kong may therefore suffice, because it simply doesn't make economic sense to use parallel structures given the size of the fund.

By contrast, a pan-Asian player operates in multiple markets and is probably willing to look far and wide for prospective investors in a multi-billion-dollar fund. It is not unreasonable to envisage a structure that encompasses Cayman, Delaware, Ireland and Luxembourg, plus a Singapore regional holding company that acts as conduit for deals struck across the region. Another consideration is the role played by sophisticated LPs that write large checks and want special treatment.

"We are seeing larger investors being more proactive and involved in terms of fund structuring. If it's a Singapore-based manager, targeting US investors making investments in Indonesia or Malaysia, we are seeing Cayman remain the default choice albeit probably with a with a Singapore master fund," says Granger of Walkers. "But if you start reducing the number of multi-jurisdictional aspects in terms of fundraising and downstream deployment, anchor and strategic investors will have more say in terms of the structure and terms."

These investors understand their tax positions far better than the GP and assured lobbying for a Canada over a Cayman fund structure, for example, is not the only result. Justin Dolling, a partner at Kirkland & Ellis, notes that some large investors have been looking at whether it makes more sense for them to go into the local fund vehicle for a single country manager – and is primarily intended for local investors – rather than the offshore feeder structure.

"The rationale for certain of these investors is that they feel tax authorities are more likely to scrutinize offshore vehicles and if the only downside is making a few filings and its more administrative than substantive, they would be prepared to go into the local vehicle," Dolling explains.

This approach doesn't come without risk. Much like opting for a Canadian limited partnership, an investor would typically be exposing itself to fully taxable and regulated jurisdictions. If the investor is relying on a DTA between its home country and the target jurisdiction, there is no guarantee that legislation will remain the same. And, as Shearman's Chen adds, the arbitration systems in less proven jurisdictions might not be suited to resolving shareholder disputes.

It is very much a strategy for sophisticated investors, and as such, any change is taking place at the margins. This reflects the broader dynamic in selecting a fund domicile: Cayman remains the jurisdiction of choice and there would need to be sound reasoning for going against the norm.

Piers Alexander, a partner at Conyers, warns against tracking a small movement in the market and extrapolating it too far into the future as an indication of a seismic shift. This tallies with observations from other advisors about making predictions in a fast-moving regulatory environment. However, the fact that greater attention is being paid to fund structuring does point to a longer-term evolution in industry best practice. Cayman will continue to play a significant role in this, but for many managers, it will be part of an increasingly intricate web.

"Investors will start seeing funds that are more complexly structured at the fund level itself and ask their manager, who is using a straight Cayman fund, why they aren't using what would seem to be the latest technology. That will make everyone think more about tax structuring," says Andrew Ostrognai, a partner at Debevoise & Plimpton. "We've seen a lot more discussion around these issues, even if the structure ultimate doesn't change, but we have also seen new structures adopted, so there may be real traction here."

More on Southeast Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.