Vietnam renewables: Good vibrations

A palpable new enthusiasm has permeated Vietnam’s sluggish renewable energy sector as rising electricity demand prompts regulatory reform. Private equity is one of the key players

The Vietnam government has a reputation for being tight-fisted when it comes to power project concessions and electricity off-take incentives. As a result, energy investors in the country don't ask for much and tend to perk up expectantly when the glacier of bureaucracy shows any sign of cracking.

The latest crack has been particularly encouraging for the renewables space. After several years of limited tangible progress, the government has issued a decision on the roll-out of solar project regulations. The new guidance is vague but generally regarded as conservative and predictable – a warmly accepted combination among investors keen to exploit even the slightest of openings.

"There can and will be investments structured on the back of this decision. A power purchase agreement (PPA) still needs to be made available, but I don't see any reason why it wouldn't be similar to PPAs that have already been formulated for wind and hydro," says David Harrison, a partner with Mayer Brown JSM in Ho Chi Minh City. "Whilst the structure may not be the way you would ideally draw it up, the existence of a skeleton framework with more detailed implementation regulations is expected shortly."

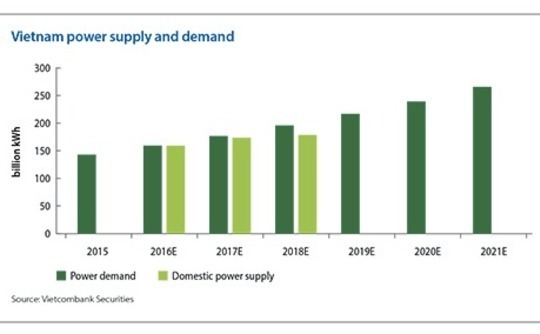

As the fundamental supply-demand dynamics of Vietnam's evolving energy space place increasing pressure on the government to take more action, enthusiasm for the new solar rules is bleeding into other renewables segments as well. However, investors are reminded to remain vigilant about a number of entrenched systemic and social headwinds.

Vietnam is commonly regarded as the most efficient power market in Southeast Asia, with an ample supply of low-cost indigenous resources including abundant hydro, domestic coal and a reasonable contribution of offshore gas. Historically, no energy has been imported and 99% of the population has been grid-connected.

Political and environmental sensitivities around coal have set up potential for improved market conditions in renewables through accelerated regulatory changes. The government's Master Plan VII aims for 10% of electricity to come from green sources by 2020 and the need to meet this target underpins the recent decision to outline basic development parameters for solar.

Renewed optimism

Importantly, the improving sentiment for renewables rests on a regulatory backdrop that places no foreign ownership limits on power projects. A wide spectrum of investors is gearing up to participate, including private equity firms taking both minority and majority positions in various projects. Feedback from players on the ground points to an uptick in conference activity and a sense that industry contractors expect to benefit from economies of scale that come with a development boom.

"If you asked me two years ago about Vietnam, I would have said forget it – it's the promised land that never happens," says Edgare Kerkwijk, managing director at Asia Green Capital. "But now the government is finally taking real steps to progress the renewable energy sector, and we're looking at potential sites to start developing."

Asia Green has been active in Vietnam since 2013 at its Hirondelles wind farm, an operation aiming to generate 60 megawatts of power but currently comprising only a block of land and a wind speed measuring device known as a met mast. Like many wind hopefuls in Vietnam, Asia Green has effectively put the project on hold due to an unworkably low off-take tariff from the government of $0.078 per kilowatt-hour.

The firm is now looking to revisit the site in anticipation that the solar decision – which promotes an off-take tariff of $0.093 per kWh – will soon be echoed in new wind regulations. The outlook is further buoyed by advancements in low wind speed turbine technology that allow for more flexibility in project site selection. The country's main wind development corridor – on the gusty but relatively unpopulated central coast – suffers from a lack of infrastructure and grid connection potential.

"We expect the wind tariff to be increased to somewhere around $0.09 in the next three to six months," Kerkwijk adds. "That still may not be great, but you can make it work if you don't have an expensive site and you are able to get competitive installation costs."

The view that off-take prices for renewables will be lifted is linked to the inherent economics of the energy sector's diversification. As imported coal and other expensive new energy sources raise the overall cost of power, the higher tariffs needed by wind and solar are increasingly justifiable. Hydro may also benefit from diversification, even if the trend means it loses its historically dominant place in the overall power mix.

Hopes for hydro

Private equity is expected to continue to be able to exploit this space because even as the role of hydro declines, existing plants will still require professionalization – as a number of recent environmental scandals have demonstrated. GPs active in this space include Denham Capital, Armstrong Asset Management, Saigon Asset Management, and UOB Venture Management.

"Hydropower has significantly lower production costs than coal and gas power but is limited by the availability of greenfield sites for the construction of new plants," says Seah Kian Wee, UOB's CEO. "As such, existing hydropower plants are particularly attractive to investors."

Last year, UOB agreed to invest $50 million alongside Orix Corporation in Bitexco Power, the largest privately owned hydro company in Vietnam with a portfolio of 18 plants generating 3,500 gigawatt-hours of energy a year. "Coupled with higher electricity prices arising from the liberalization of Vietnam's power sector, hydropower plant operators in the country can look forward to better margins," Seah says.

Most outlooks insist, however, that hydro will be a significantly smaller part of Vietnam's energy future in decades to come. Although it represented more than 50% of total electricity production as recently as the early 2000s, it is expected to slide to around 20% by 2020 with total energy demand outstripping the river system's natural potential for increasing supply. As of 2015, hydro accounted for 38% of power generation, according to government data.

Hydro investors are nevertheless continuing to find small but economically viable growth areas. Schemes include "pumped storage" technology whereby coal-fired electricity forces used hydro plant water back to the top of a hill during low-demand hours at night. The water is then allowed to flow downhill once again to power turbines during peak daytime hours. Another intermittent sourcing option is run-of-river technology, which exploits seasonal currents without the use of a reservoir.

Coc San, the country's newest hydro plant, began operations last year using a run-of-river system and is now said to be performing above initial expectations. The 30 MW station was acquired by Nexif Energy, a Southeast Asia-based energy investment platform backed by Denham, and Infraco Asia Development, a Singapore-based developer that catalyzes private sector investment by de-risking distressed assets.

"We believe hydro is still going to be an important part of the mix," says Allard Nooy, Infraco Asia's CEO. "In the north, there are still river systems where you can build additional capacity. They're going to be run-of-the-river in a range of 30-70 MW, but there are definitely more than 10 of those projects that are either under study or already past the pre-feasibility stage."

The high level of knowhow and integration that comes with the well-established presence of hydro in Vietnam makes such ambitions possible, but it is a unique advantage in the local renewables scene. Investors in wind and solar development, by contrast, will have to navigate a host of touchy land acquisition issues including the resettlement of farming communities and negotiations with provincial authorities.

"Getting land clearance is the biggest risk for foreign investors because disputes with the land users could delay projects for several years," says Tuan Nguyen, managing director at ANT Consulting, a professional advisory firm that is active in the domestic energy sector. "When the government gives its green light, the investor will get the land most of the time, but after that, clashes with the local people can drag on the timing of project development."

Investors with experience in the country warn there is little chance of sidestepping this issue by targeting unused real estate. Almost all land in Vietnam is either being put to some kind of artisanal economic use or would require the relocation of a large number of people.

Onshore wind, which typically requires beachfront property, is often considered particularly vulnerable to land sourcing challenges. But solar developers may be most affected, given the large areas required to spread out an economically viable array of panels.

"Land compensation and clearance processes will definitely delay some projects, and I do worry that there are many new investors coming into Vietnam interested in the solar market who have never actually experienced that here before," says Gavin Smith, director of clean development at Dragon Capital, which has been investing in the region since 1994. "They could have an unpleasant surprise because it's not as easy as it looks."

Dragon's current portfolio in the country is mostly in hydro, although it has established 30 MW of solar operations in Thailand and hopes to quickly replicate the achievement in Vietnam leveraging its local experience. The plan is considered possible within two years, which will be a necessity since the sector's new regulatory guidance will only be in effect until June 2019.

The narrow window of opportunity for setting up the required PPA will be particularly challenging for companies without existing relationships in the country. Indeed, difficulties around the learning curve for first-time solar developers in Vietnam could be a deal-breaking factor in the near term.

State-owned obstacle

This sticking point is complicated by the fact that all terms around power pricing and contract structure are effectively dictated by state-owned utility Vietnam Electricity (EVN), the only legal off-taker. The three primary concerns with EVN point to a need for international-quality contract standards, complaints by some investors that the company attempts to modify previously agreed guarantees, and poor overall business performance.

The latter of these issues has resulted in EVN being considered an un-creditworthy company by international lenders. Vietnamese banks will lend against an EVN off-take deal, but domestic sources are considered largely insufficient to meet the estimated $10 billion of financing demand represented by the country's existing pre-licensed energy projects.

Expectations are high, however, that Vietnam will follow the example of the Philippines, where a relatively liberalized regime now allows for non-government PPAs. It is rumored that the country's first bilateral, non-EVN off-take deal is being initiated for rooftop solar installations at airports. Meanwhile, renewable energy players are sensing traction that EVN could improve its creditworthiness, either through internal pressure to meet the energy gap or external intervention from a group like the World Bank.

While the optimism behind these outlooks has been recently punctuated by the regulatory momentum in solar, it remains rooted in far firmer macro drivers. As confidence grows around the idea that a looming energy supply shortfall will press government to continue opening up renewables, investors look at the market with an increasing sense of urgency.

"You will see some investors moving straight forward with their solar investments here in Vietnam because these problems need to be solved now, not in a year's time," says Dragon's Smith. "I don't think the projects being started will be even a large fraction of the 10 GW required, but there will be some investors here for sure – and we intend to be one of them."

More on Southeast Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.