ASEAN integration: Gathering momentum

Continued economic integration with Southeast Asia could open the way for transformative investment opportunities, but private equity players must believe in the region’s potential before they take the plunge.

For Rodney Muse, co-managing partner of Navis Capital Partners, the recently established ASEAN Economic Community (AEC) represents the opening of a door that the firm has had its foot in for years. The agreement's efforts to promote regional economic integration by lowering barriers to trade has the potential to create significant investment opportunities.

"That opportunity has always been there, but it has always come at a cost. It was only companies with unique capabilities that were able to build regional businesses, but we've done it in a few industries," says Muse. "Now with these reduced borders, if you could identify similar companies with that capability set, I think that's a real possibility and it's something that we should seek to pursue."

At the same time, however, he and other investors are aware of the challenges that still need to be overcome. Considerable disparities still exist among the ASEAN member states, and trade agreements can only go so far in papering over those divides. Despite dreams of a united economy big enough to rival China and India, ASEAN integration will take some time to realize its full potential. And investors hoping to bank substantial returns will need to temper their ambitions as the region develops.

Inbound flows

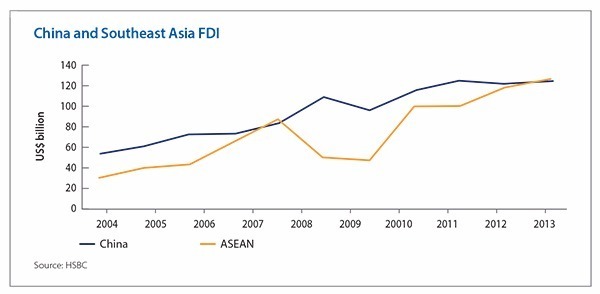

Interest in Southeast Asia as an investment destination was growing long before the establishment of the AEC last year. Data from HSBC show that while foreign direct investment (FDI) in Greater China eclipsed that of ASEAN countries around 1992, FDI for both regions grew at the same rate starting in 2002, with ASEAN overtaking China briefly just before the global financial crisis, then again in 2013.

The growth in FDI has been attributed in part to rising costs of workers in China, prompting multinational companies to relocate production facilities to countries with cheaper labor in nearby Asian regions. A survey of Japanese firms with overseas operations showed that between 2006 and 2014 the amount of firms planning to locate their production facilities in the ASEAN region grew from 30% to 48%, while the companies planning to locate in China dropped from 50% to 18%.

With the expected lowering of trade barriers within the ASEAN bloc, economists expect the appeal of the region as a destination for FDI to continue to grow, as companies realize the advantage to be gained by leveraging the strengths of the various member countries.

"You're looking at production synergies as well. For instance, you can see the cheap labor in Myanmar, Laos, and Cambodia, being complemented with the production sophistication in Malaysia and Singapore," says Weiwen Ng, economist for South and Southeast Asia at ANZ. "So effectively even though we're in a secular trade slowdown globally, within ASEAN itself you can see some rise in traditional trade."

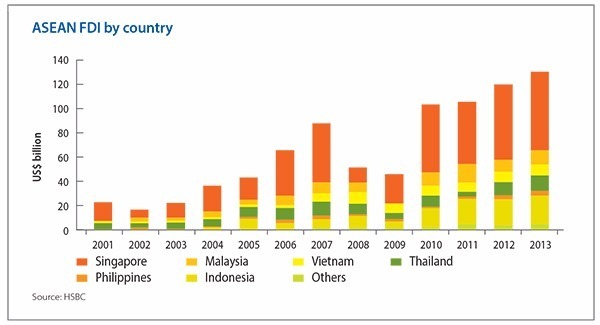

Along with growth in foreign investment among the various ASEAN countries, FDI has also diversified as the region advances. The leading recipient of inbound capital continues to be Singapore; it accounted for 53% of the cumulative FDI into ASEAN between 2001 and 2013. Even in 2013, Singapore received over $60 billion of the total $125 billion invested, almost as much as every other ASEAN member combined.

However, despite the dominance of Singapore, other countries have emerged as attractive destinations as well. Investment in Indonesia, almost nonexistent in the early years of the century, had risen to more than $20 billion by 2013, and Thailand received about $10 billion the same year.

While cross-border cooperation is expected to create substantial opportunities as ASEAN opens up, investors also expect intraregional competition to offer up openings for capital. Most players are watching the field for industries that exhibit strong potential in particular countries, and can take a dominant position in a market where many barriers to access have been dismantled.

"I think automotive, for example, will create significant opportunities in a market like Thailand, that already has quite a bit of critical mass, technology partnerships with Japan and Germany, and some real scale operations," says Navis' Muse. "That would likely be at the expense of other countries, which have always been a little bit subscale and largely reliant on the local automotive brands."

This regional awareness has always been a strong component of Southeast Asia investment, even before the move to liberalize trading barriers within the region. Andrew Thompson, head of Asia Pacific private equity at KPMG, notes this has mainly been due to the relative weakness of the individual countries; the region itself was what attracted investors.

"Very few countries within ASEAN individually are of enough scale that they become global-focused destinations themselves," he says. "Therefore what a lot of people are attempting to do is build ASEAN or Southeast Asian hubs and regionalized businesses. That is currently very difficult, because of the different laws, regulations and all the rest, and some of the historical trading difficulties, challenges and everything that goes with it."

Easing these restrictions has been one of the main goals of the AEC. The community's plans include the removal of tariffs - though this may have limited practical effect since a number of industries are exempt, including agriculture.

But tariffs are only part of the story. Multiple additional trade barriers still exist, from official policies like regulations to those that are harder to define, such as cultural misunderstandings. Diplomats can handle some of these issues - for example, customs clearance for most countries have been simplified in the interest of speeding up cross-border trade - but others will take time and considerable work to resolve.

Barriers to trade

Some industry participants in Southeast Asia are relatively unperturbed about this issue; Muse believes that "the non-tariff barriers will have to erode, because they're hard to defend over long periods of time. Eventually logic will prevail and the best producer with the best price and the best service will win."

However, investors also acknowledge that cultural differences between the various member countries could indicate bigger problems with the acceptance of the community as an economic and political reality. Despite the potential economic benefits of greater integration, political issues could prove to be a significant barrier to the AEC's progress.

When discussing the future of the region, the recent turmoil around the UK's recent decision to exit the EU inevitably arises. Industry players acknowledge that the same forces that led British voters to favor leaving the trading bloc could come into play in Southeast Asia, particularly fears of economic exploitation by a dominant partner or by outsiders. Differences in language and culture are also seen as a significant challenge to overcome.

However, participants note that the two cases are also dissimilar in many ways. While ASEAN and the EU have surface similarities, the motivation behind them is significantly different; the EU grew out of a desire to regulate arms production and prevent another regional war, a motivation that was absent in Southeast Asia. According to this thinking, ASEAN's less ambitious goals could turn out to be a source of strength.

"ASEAN is not really like the EU. ASEAN was born of pragmatism to fulfill a common economic interest," says ANZ's Ng. "There's a good chance that the rise of isolationist policies and protectionism would actually impede the AEC. But as long as there are mutual economic benefits to be gained, I think there's a good chance that this community will still succeed over the next decade or so."

Also a factor in this cautious optimism is the difference in administration between the EU and the AEC. Unlike the European partnership, the AEC has no central government for local citizens to rebel against. The bloc also has no unified currency to be exploited by weaker members of the organization. Overall, there is much less reason for concern over loss of sovereignty under ASEAN and the various trade agreements both within the region and between ASEAN members and other countries.

One of those agreements, the Trans-Pacific Partnership, has drawn concern; the treaty will include giant regional competitors such as China and the US, along with several members of ASEAN, and some worry that it could supersede the earlier agreement or render it irrelevant. However, most industry watchers dismiss these fears, pointing to the TPP's protracted negotiating timeline and fierce political opposition in the US as signs that its effects will almost certainly be limited.

"It's much easier for smaller groupings of like-minded economies that share a common vested interest or a common culture, like the AEC or the Regional Comprehensive Economic Partnership, to negotiate trade outcomes, than a full multilateral trade round like the TPP," says ANZ's Ng.

A PE boost?

Despite the positive outlook for Southeast Asia, however, ASEAN integration has yet to deliver a substantial uplift in private equity investment. While there is considerable activity in member countries, industry watchers say it tends to be generated by the same funds that have operated there for years, with GPs that are not already active in the region exhibiting little interest in increasing their participation.

Those GPs that do operate in Southeast Asia tend to share a pragmatic outlook. ASEAN integration has proven a considerable driver of investment opportunities, but openings have also been seen in companies that operate on a global or local scale. Regional integration therefore necessarily plays a part in their considerations, but investment levels are not high enough for it to be the centerpiece of a strategy.

"Our thesis is to invest in companies that are selling within Southeast Asia or that benefit from being based in Southeast Asia," says Eugene Lai, managing director and co-managing partner at Southern Capital Group. "All our portfolio companies sell within Southeast Asia except for one business that is based in Malaysia but sells globally. We have also helped some companies expand into new markets in Southeast Asia. It's a theme we like, but it's not the only theme; we also have purely domestic companies."

Though the current crop of GPs continues to find opportunities in Southeast Asia, the reluctance of other firms to dip a toe in the water is seen as a sign that the region has yet to mature and reach the level of Asian rivals such as China and India. Further integration could change this - if companies were able to operate across multiple markets and achieve scale, they would become viable targets for pan-Asian and global PE funds - and there is generational optimism that it will happen.

Muse notes that Navis' strategy revolves around finding assets that are not necessarily irresistible now, but that will be by the time the firm looks to sell. "We wouldn't factor AEC into an investment that we'd make today," he says. "But our approach is to buy businesses that strategics will want to acquire, so it is something that will be relevant five years from now after the dropping of some of the tariffs and duties across the various countries. So we're expecting it to be delayed, but in most scenarios to end up being largely implemented."

More on Southeast Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.