Hong Kong PE: Institutional outpost

Hong Kong's regulatory approach can cause headaches for GPs, but the territory offers investors a number of advantages as well

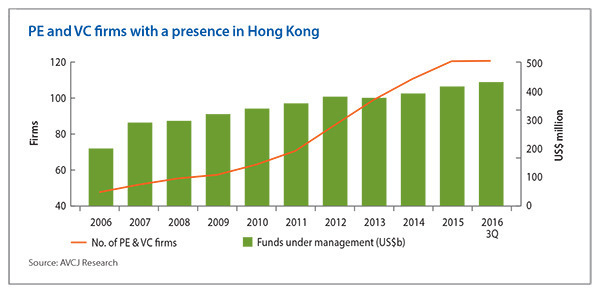

The Hong Kong government's approach to private equity has come in for a fair amount of criticism in recent weeks and months, not least in AVCJ.

The industry's two primary concerns arise from regulatory guidance notes issued by the Inland Revenue Department (IRD). First, the extension of the local profits tax exemption to include offshore PE funds - which would mean PE firms would no longer have to set up structures designed to avoid becoming liable for local tax - has been rendered largely unusable by the restrictive nature of the guidelines.

Second, the IRD broke with international precedent in planning to tax carried interest as income rather than capital gain, at the corporate or individual level. Some sort of unofficial compromise could still be reached, but the situation does little to promote Hong Kong as Asia's preeminent private equity staging post.

It is therefore worth noting that in the past fortnight two GPs have opened Hong Kong offices. Actis established a presence primarily for investor relations and client services activities in Asia. Then Australia's IFM Investors set up shop, emphasizing its need to globalize investment capabilities and the desire of its clients to seek opportunities in the region.

These moves emphasize Hong Kong's near-term strategic advantages best reflected through its convenient location and ready supply of human capital. In the case of IFM, it appears the office will be a platform for its investment capabilities and relationships across Asia. Actis, meanwhile, sees Hong Kong as a base for investor relations from China to New Zealand.

The Asia Pacific region accounts for 16% of the firm's investor base, yet is 30% of the global capital pool. Actis expects the capital sourced from Asia to increase significantly based on the volume of institutional funds available and increasing appetite for exposure to alternatives.

Hong Kong's relevance in this context is not just relatively short flights to the region's major cities. It is also likely to become an important, though indirect, capital source in its own right. In October, Abu Dhabi Investment Authority (ADIA) became the latest large institutional investor to enter Hong Kong.

The territory is also a logical base for China's institutional investors. Wealth management players such as Noah Holdings and CreditEase offer offshore fund-of-fund and co-investment products, and Hong Kong is the headquarters for their international operations. The likes of insurance companies may do the same.

The prevailing regulatory uncertainty should not be an obstacle for these groups - unless they set up fund management-type entities for direct investments and raising third-party capital.

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.