4Q analysis: Ending with a whimper

4Q analysis: Bain Capital and PAG shine in a difficult fundraising environment; large-ticket infrastructure and tech deals offer pointers for 2016; public market volatility continues to hamper PE exits

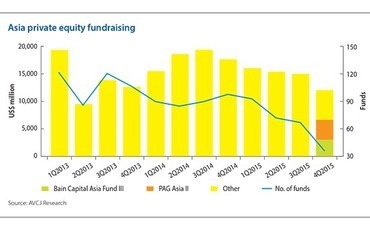

1) Fundraising: Strong finish to a weak quarter

Bain Capital and PAG ensured Asia private equity fundraising ended 2015 with a flourish, but their respective final closes added gloss to a shaky final three months of the year. According to provisional data from AVCJ Research, October-December represents the lowest quarterly fundraising total in two-and-a-half years.

For Bain and PAG it was a swift process: Bain took seven months to close its third Asian fund at the hard cap of $3 billion, plus a GP commitment of at least $250 million, while PAG reached a first and final close on its second regional vehicle of $3.66 billion within eight months. Both funds are larger than their predecessors.

It is yet another indication of the "flight to quality" that has been the defining characteristic of Asia PE fundraising in recent years. Bain and PAG accounted for just over half of the $12.1 billion raised in the fourth quarter of 2015 - while additional activity may come to light, one has to go back to the second quarter of 2013 for a smaller total. Even then, April-June 2013 saw close to 90 funds reach a final or partial close; for the most recent quarter it was fewer than 40.

Fundraising declined - in terms of capital raised and number of vehicles reaching a close - with each quarter of 2015. For the year as a whole, $58.8 billion was raised, the lowest since 2009. This is in part a function of who is in the market. Activity on the buyout front was minimal in 2009 and 2010 but in each of the four years after that the total increased as global firms raised their first regional funds since the global financial crisis. The series of closes ended in 2014, so the amount of capital entering buyout vehicles dropped last year.

Nearly 60% of the total raised for buyout funds in 2015 came in the final quarter. This was thanks to Bain, PAG and to a lesser extent Northstar Group, which closed its fourth Southeast Asia fund at $810 million. This was one of the more challenging fundraises - the vehicle launched in early 2014 - due to investor concerns about Indonesia. Much of the corpus was captured in AVCJ's 2014 statistics because Northstar reached a sizeable first close.

The spike in buyout activity was counterbalanced by one of the weakest quarters for growth capital fundraising on record. LPs committed less than $1 billion to growth vehicles, with South Korea-based Premier Partners recording the largest final close at $167 million. China has traditionally been the source of most growth funds but the fourth quarter was notably lackluster, likely due in no small part to uncertainty surrounding the country's economy.

China is also responsible for most of Asia's venture capital fundraising and this also dropped off substantially in the final three months of 2015. A total of $12.7 billion entered 183 VC vehicles region-wide in 2014. This fell to $10.6 billion and 136 funds last year, as the China share dropped from $7.6 billion to $5.6 billion. In the final quarter, a paltry $841 million was raised - compared to $2.4 billion for the previous three months - as the Asia total decreased from $3.3 billion to $1.7 billion.

Several GPs closed top-up vehicles with a view to re-upping in portfolio companies that are raising larger rounds as they stay under private ownership longer. There was still plenty of capital entering internet-related start-ups in the last three months of 2015, so it remains to be seen whether the slowdown in VC fundraising reflects anecdotal evidence of the technology bubble deflating. As with buyout funds, much depends on which GPs are in the market.

Of the 25 largest funds to reach a partial or final close in the final quarter, nine are VC vehicles. Four of those nine are healthcare-focused, led by Lyfe Capital, set up last year by former executives of Vivo Capital and IDG Capital Partners, which raised $298 million. Sector specialization, it appears, strikes a chord with LPs.

2) Investment: More tech, more infra

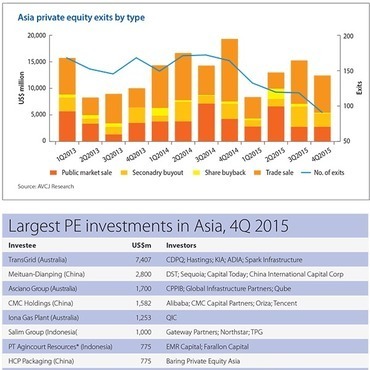

Two deals account for about one third of the $31.9 billion deployed by private equity firms in Asia during the final three months of 2015, down slightly on the previous quarter. It took investment for the year as a whole to $133.3 billion, the highest-ever annual total.

First, the New South Wales government privatized TransGrid, part of its electricity network, with Hastings Fund Management, Caisse de dépôt et placement du Québec, Kuwait Investment Authority, Abu Dhabi Investment Authority and Spark Infrastructure paying $7.4 billion. Then Tencent Holdings, DST Global, Sequoia Capital, Capital Today and China International Capital Corp. were among those that reportedly committed at least $2.8 billion to the recently merged Meituan and Dianping.

Both deals point to wider trends that could be felt in 2016 and beyond.

Infrastructure was responsible for one of Australia's biggest quarters in years, with $10.9 billion invested compared to $13 billion in the first nine months. Along with TransGrid, Canada Pension Plan Investment Board and Global Infrastructure Partners helped Qube Holdings to buy a minority stake in Asciano Group for $1.7 billion. QIC also led a consortium to buy the Iona Gas Storage Facility for $1.25 billion.

With the New South Wales government planning to privatize 49% of the state electricity network by the middle of this year, further deals of a similar nature appear inevitable. Other state governments are also likely to sell leases to existing assets in order to fund new infrastructure projects. Private markets investors are willing to pay a premium for operational brownfield assets but they are still wary of greenfield exposure.

Meituan and Dianping, meanwhile, are part of a growing number of companies in China's technology space that have concluded they will fare better as a single dominant player in a segment than as cutthroat rivals. Investors are also less willing to continue supporting businesses that pump most of the capital into subsidy programs that are ultimately unsustainable.

Ride-hailing apps Didi Dache and Kuaidi Dache came together earlier in 2015 and raised $3 billion at a higher valuation than the aggregated worth of the two companies when they operated independently of one another. Meituan-Dianping is a similar story: Dianping and Meituan, which closed their previous rounds at $4 billion and $7 billion, respectively, are said to have raised their first joint round at a valuation of $18 billion.

Early- and growth-stage investment in internet-related companies in Asia reached $9.5 billion in the final quarter of 2015, taking the annual total to $31.1 billion, more than twice the 2014 figure - and 70% of it went into Chinese companies. Growth-stage activity has been particularly frenetic, with $16.3 billion committed across more than 70 deals last year, compared to $2.8 billion across 24 transactions in 2014.

With 2016 barely two weeks old, tech sector consolidation is already emerging as a prevalent theme, with VC-backed Chinese online shopping and social networking platform Mogujie agreeing to acquire rival Meilishuo.com in a stock-swap deal worth around $3 billion. Activity is not confined to China. Southeast Asia e-commerce sites Moxy and Bilna are set to merge, while Indian classifieds site Quikr has bought property search website CommonFloor.

Elsewhere in Asia, the fourth quarter of 2015 was relatively quiet with India, Japan and South Korea seeing less deal flow than in the previous three months. Indonesia, like Australia, was an outlier. Thanks to a $1 billion structured transaction for local conglomerate Salim Group, led by Northstar Group, and an EMR Capital consortium buying a gold mine for $775 million, the country experienced its most active quarter on record.

3) Exits: IPOs up, exits down

Given the volatility experienced by public markets across the region in the wake of the China sell-off in mid-August, most major indices ended the fourth quarter of 2015 in a better condition than they started it. Nevertheless, investors remained nervy, as evidenced by another weak three months for public market sales by GPs. With another China-initiated plunge in early January, this caution seems justified.

Public market sales came to $2.7 billion, in line with the previous quarter, and the weakest total in two years. With trade sales also down at $7.1 billion from $8.3 billion, overall exits reached $12.5 billion compared to $15.4 billion in July-September 2015.

However, private equity-backed IPOs did rebound with 74 companies - nearly twice the number in the previous quarter - generating proceeds of $10.2 billion. Eight of the 20 largest offerings took place in Hong Kong, and accounted for roughly half of the region-wide proceeds between them. They included China Huarong Asset Management, Dali Foods Group, China International Capital Corp, and IMAX China.

The 12 biggest PE-backed IPOs of 2015 featured 10 Hong Kong entries, which were responsible for close to half of the $40.1 billion raised in total. This was well short of the $70.1 billion generated in 2014, but then there was nothing of the scale of Alibaba Group's US offering. Exits for the year as a whole were also down on the record return of 2014 - $49.4 billion compared to $65.1 billion - and this can be explained by the lack of bumper trade sales.

One area that did hold steady on a year-on-year basis was secondary sales. A total of $9.1 billion was transacted, compared to $9.2 billion in 2014 and $7.9 billion in 2013. The 2015 total included $2.6 billion in the final quarter, with a sizeable portion of that coming from two acquisitions by Baring Private Equity Asia.

Of the close to a dozen control deals Baring has disclosed since the start of 2013, eight have facilitated exits for existing private equity investors. In the final weeks of December it emerged that the firm had bought China-based HCP Packaging from TPG Capital for $775 million, while an agreement was struck to acquire Interplex Holdings from CVC Capital Partners and Standard Chartered Private Equity for around $318 million.

More on Buyouts

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.