Fund finance: Filling Asia's SVB void

Silicon Valley Bank’s collapse has prompted Asia-based GPs to review their relationships with lenders, for fund finance and general banking. Smaller managers may find the process challenging

Asian PE and VC customers of Silicon Valley Bank (SVB) are generally happy with the level of service received. The specialist technology and healthcare lender, which was placed into receivership earlier this month, is praised for being accessible, efficient, and in tune with the needs of the industry.

"One of the main reasons for using them is they are straightforward in terms of account opening. They ask for all the KYC [know your customer] documents, but once that's done, the account can be opened within a week. It's important because when we do deals, we need to set up specific entities to ringfence the risk and segregate cash flows," said one China-focused manager.

"We have 60 accounts with SVB. I can open the app, log in, and see them all. I can also assign different levels of authority to finance team members in terms of what they can do. The online service and the phone banking service are both good."

Due diligence provider Castle Hall identified nearly 6,000 private funds that use SVB, excluding those managed by pureplay VCs that do not register with US regulators. Over 40 Asian GPs are included, most of them Chinese – from VCs like Joy Capital and Gaorong Capital to PE players CMC Capital and FountainVest Partners. Nexus Venture Partners is one of the few Indian representatives.

About a dozen of those contacted by AVCJ offered details of their relationship with SVB, emphasizing not only ease of use but also the availability of fund-level financing facilities. A couple were willing to go on the record, and they broadly echoed sentiments expressed by many of their US peers.

"We have been banking with them since day one," said David Wei, founder of Vision Knight Capital, another China manager, which has transferred all its deposits to accounts with other lenders. "Once we see the situation improve, we would be very interested in continuing to bank with SVB."

The Federal Reserve Bank and Federal Deposit Insurance Corporation moved to avert financial contagion by guaranteeing SVB deposits; First Citizens Bank has since agreed to buy the loan book. Asian GPs that are customers will be made whole, but SVB's implosion has far-reaching implications.

First, private equity firms are scrutinising the financial health of their partner banks, fearing one of them might be the next domino to fall. Many are instituting new best practices such as working with more lenders, sweeping cash into assets held off-balance sheet, and accelerating distributions.

Second, it is unclear who will replace SVB in Asia; not just for day-to-day services but also for fund finance, which became a key part of the bank's business. By allowing PE and VC firms to borrow against uncalled LP commitments and unrealised fee streams, SVB bound itself closer to clients, with one eye on securing additional business with the managers and with their portfolio companies.

Asia's nascent fund finance market – dominated by subscription lines, or loans secured against uncalled capital – was already adapting to a world in which rising interest rates have made products more expensive. Now managers are asking for reassurances about the solidity of supply.

"The queries we are fielding from managers and their advisors range from which bank to open bank accounts with, to the ability to remove a bank from a banking syndicate, to releasing collateral posted to a non-cooperative bank and moving liquidity lines to other banks," said Soumitro Mukerji, a Singapore-based partner in the banking and finance practice at Mayer Brown.

"This is a serious issue for managers which poses both immediate and practical issues on current financings but also broader and bigger picture issues around who will fill the liquidity gap."

Lines of sight

SVB entered Asia in the early 1990s and gained traction through a combination of onshore and offshore services, largely aimed at managers in China and India. Subscription lines, effectively used by GPs to delay capital calls made to LPs in the interests of investment flexibility and improved IRRs, were not the first product offered but they became the preeminent one.

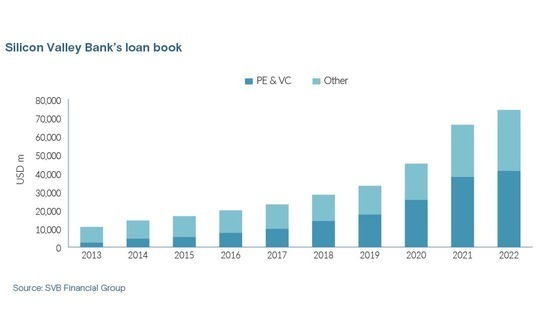

Ten years ago, loans to private equity and venture capital firms – the vast majority of which are subscription lines – accounted for USD 2.4bn of a USD 10.9bn global loan book. By 2017, this had become USD 17.7bn, or 53% of the book. Over the next three years, the business more than doubled in size; SVB had USD 74.3bn in outstanding loans, USD 41.3bn of them to PE and VC firms.

"It's a very low-risk credit line and it ensures there is more stickiness in the relationship with investors and offers some insight into the capital flows," said Vinod Murali, co-founder and managing director of India-based Alteria Capital, which spun out from SVB's India venture debt unit not long after the business was acquired by Temasek Holdings and United Overseas Bank (UOB).

"Subscription lines were a means to an end, a way for SVB to wrap its arms around VC firms, while deploying some capital and making a sedate return. It was a plain vanilla product, not a big earner."

AVCJ approached SVB's regional head of global fund banking - the division responsible for lending to PE and VC firms - for comment and received no response.

Rising interest rates have since pushed SOFR from 20 basis points above zero to 4-5% territory, while the pricing margin has shifted up to 180-210 basis points. Uday Krishna, an executive director at Affirma Capital, observes that the cost of a subscription line is nearly at par with the 8% hurdle rate above which managers receive carried interest on their funds, negating the use of leverage to boost IRR.

"A manager may take a different view on the higher interest rate environment depending on why they are looking at the liquidity line," said Mayer Brown's Mukerji. "If they were approaching it from an IRR enhancing lens versus gaining an advantage over competitors in a bid situation or solving for a sub-optimal asset sale, the analysis of the increased funding cost would be quite different."

Most subscription line providers say they have seen little change in demand at the top end of the market, although the pace of utilisation may drop in tandem with a slowdown in private equity deal flow. Managers are already finding workarounds to rising interest rates, for example by opting for zero-fee uncommitted subscription lines or committed lines that can be switched on and off.

Paul Aherne, a partner in the global finance and corporate group at Walkers Global in Asia, is not alone in regarding market volatility as the bigger concern. Capacity is constrained by lenders becoming more selective as well as some notable withdrawals – last year, Citi backed away from subscription lines globally while SVB's future is uncertain.

Feast to famine

The likes of SVB and East West Bank (EWB) differ from the mainstream by targeting venture capital and growth equity managers. The sweet spot is USD 30m-USD 50m compared to USD 100m and above for global banks. Moreover, they will lend against commitments from LPs beyond the top-tier pension plans, endowments, and sovereign wealth funds.

"Their pricing was good, not a lot better than the others, but they were user-friendly. Most lenders want to see blue-chip LPs, and some have a lot of soft conditions, like requiring you to have at least five qualifying LPs. SVB was by far the most lenient. They would include certain LPs in the borrowing base that others would not include," said a second China-focused manager.

SVB turned its familiarity with the LP community into an advantage. Family offices and high net worth individuals (HNWIs) represent a higher risk than institutional investors, but SVB might have tracked them across multiple funds and have records of previous commitments. Industry participants note that most commercial banks in Asia would struggle to make such distinctions.

What proved to be SVB's weakness had nothing to do with credit quality. The surge in loans during the post-pandemic technology boom was matched by a surge in deposits – they reached USD 189bn in 2021, a threefold increase on 2019 – and SVB invested heavily in long-dated Treasury bonds.

Rising interest rates caused these bonds to fall in value and the bank was left with large unrealised losses at a time when client withdrawals increased as other financing channels tightened. Emergency capital-raising measures couldn't abate the pace of withdrawals. SVB was arguably a casualty of a protracted period of lax regulation; it was certainly a casualty of poor treasury management.

"If a bank offers you an attractive deposit rate and an attractive lending rate, you must ask how it is making money. Is your deposit really in a savings account on the balance sheet or has it been swept into a securities account overnight? That's what happened to SVB's deposits, and it brings exposure to a different level of risk," said an investor who previously worked for a bank involved in this area.

Direct exposure to SVB among Asia-based GPs is limited because balances tend to be small. For example, if the bank holds accounts for individual funds, there are continuous inflows and outflows as capital is called from LPs and proceeds are distributed to LPs. Some subscription line providers insist the fund banks with them so they can take security over the assets they are lending against.

The first China-focused manager noted that, without the government guarantee, his firm could have been out of pocket. At the time, more capital than usual was sitting in the fund account having been called ahead of an investment. In addition, the GP management company also banked with SVB, so unused fees had accrued there. A third manager said he had distributions pending when SVB failed.

"Normally, on selling a company, a chunk of money spends a week or two in the fund account while you do the confirmations. You email every LP to check that their account is still active, they email back saying this is correct, and then a third party from outside the finance team confirms it," said Marc Lau, a managing partner at fund-of-funds Axiom Asia, which is not the manager in question.

Question time

The risk of getting caught on the wrong side of insolvency has put private equity firms on the defensive. One fund finance professional with an Australian bank observed that, in the last three weeks, "the scrutiny normally applied from a lender's perspective to GPs and LPs has done a 180-turn and it's the GPs who are questioning bank balance sheets."

Inevitably, treasury management is on the agenda as managers map out the implications for their holdings under different scenarios. Some lines of inquiry have uncovered previously unforeseen obstacles, with Alan Davies, a UK-based finance partner at Debevoise & Plimpton, highlighting specific provisions in subscription line documentation.

In most deals he has worked on, the GP is not required to maintain accounts with the provider – a charge over the account taking distributions is sufficient. However, in certain cases, GPs have been told they cannot move the fund account without permission from the lender. "Most people don't move accounts, so we weren't focused on the flexibility to do so," he said.

Nevertheless, numerous managers in Asia are moving money between banks, and opening more accounts, in the name of relationship diversification. Several GPs also said they had been advised to set up mechanisms to routinely sweep cash from bank accounts into money market products so that in the event of a bank failure, their assets would not be found on the balance sheet.

Another course of action involves routing distributions to an array of separate accounts across different banks to spread out the risk. "The key is to not use one account for all purposes," said Grace Lee, CFO of Chinese VC firm Qiming Venture Partners, who notes that the SVB incident is an opportunity for revisiting back-office management, fund finance, and managing counterparty risk.

Qiming wants to increase distribution frequency as well. When exiting a listed company through a series of small sell-downs over several weeks, standard procedure was to make a distribution to LPs at the end of the process. Qiming is now making several smaller distributions during this period.

In addition, Lee advocates leveraging financial markets to stay ahead of events. Recognising that gathering information in an uncertain economic environment can be a hit-and-miss exercise, Qiming turned to the credit default swap (CDS) index as a more scientific base. Any change in the credit ratings could indicate impending difficulty for a bank.

Flight to quality

A fund finance professional with a Japan-based institution claims to be receiving plenty of inbound inquiries from managers seeking the stability of a Japanese bank. This tallies with an account shared by Albert Tan, a partner and co-chair in the fund finance practice group at Haynes & Boone, of "a flight to safety mentality" among fund sponsors globally with tier-one banks the main beneficiaries.

For these banks, now operating in selective mode, there is greater emphasis on what they can get from sponsors franchise-wide. This appears to accentuate what Davies of Debevoise describes as a relationship-driven Asian market, where there is little European-style broad syndication of facilities and lenders are happy to work with sponsors they know and steer clear of those they don't.

It is unclear how the typical small to mid-cap SVB customer fits into this landscape. "Will the big global banks recalibrate what they are willing to do if there is more demand for smaller deals?" said Aherne of Walkers. "I wonder whether they would have the appetite for that in the current market."

While new lenders have entered the market and some existing players have stepped up from taking positions in syndicated transactions to leading deals, they often pursue specific angles. Chinese banks tend to target Chinese sponsors and Singaporean lenders are said to prefer real estate to PE. Conservatism is the key theme, which counts against GPs with concentrated strategies and LP bases.

Mayer Brown's Mukerji adds that taking on new clients is not a priority for any banks right now because they are preoccupied with assessments of existing portfolio exposure. Half the deals he is working on are proceeding as usual; the other half are slowing down. Some banks are pushing back on timelines imposed by managers, and a fair number of deals are being repriced.

One of SVB's Asia-based private equity clients admitted that a solution to the firm's banking problems is still being sought. Another chose to delay a decision on moving accounts elsewhere. The manager noted that SVB's international transfer business has resumed operations following a short suspension, adding wryly that SVB is now "the safest in the world" thanks to the backstop.

The concern is that smaller, less proven managers will struggle to find workable alternatives. "It depends on how strong your banking relationships are. Most banks want to reduce their account numbers, they don't want to go through all these KYC procedures," said the second China-focused manager. "If you are a younger firm, it could be difficult."

Even when new relationships can be forged, the full range of SVB's services – in a private equity-friendly wrapper – would be difficult to replicate. Chinese banks are pitching managers for business, but they don't always have the resources or will to provide day-to-day banking as well as cross-border and fund finance solutions. Absent a rejuvenated SVB, the future is uncertain.

"There will be a huge void for servicing that lower end of the funds market," the fund finance professional with an Australian bank reflected. "I'm not sure who will take that up – maybe some new credit funds will emerge – but the pricing won't be what people have become used to."

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.