2023 preview: Japan middle market

Confidence in Japan’s middle market is whipping up new deal flow, new funds, and new exit channels that will play out in 2023. This includes the possible reanimation of a dormant IPO market

Integral Corporation is bullish about post-pandemic Japan. The firm cites familiar deal-driving trends such as younger business owners seeking succession solutions and growing interest in corporate divestments. But it has also gone as far as to invest in two companies that provide physical office supplies and, even more bravely, attempt an IPO.

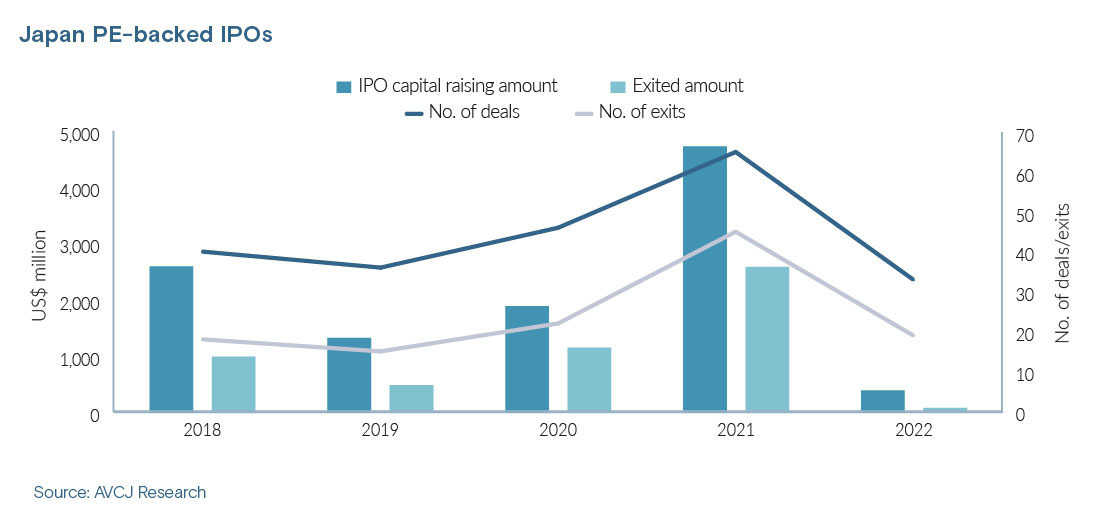

Offerings by PE-backed companies have generated proceeds of USD 78.9m so far this year, compared to USD 2.6bn in 2021 and USD 1.1bn in 2020. The 2022 total has come from 19 IPOs, all on the Tokyo Stock Exchange's start-up boards. Last year there were nine liquidity events via IPO across the main and JASDAQ boards. There were 36 on the start-up board.

Snapping the drought late, Integral realised at least a partial exit from local air carrier Skymark Airlines – another show of confidence in a post-pandemic rebound – in a JPY 32.5bn (USD 237m) IPO this week. It acquired a 50.1% stake in the company in 2015 for JPY 9bn.

"We didn't see any private equity buyout shops doing IPOs this year, but the market is gradually recovering," said Tsuyoshi Yamazaki, a partner at Integral. "Skymark got hit by COVID-19, but it recovered. Domestic travel is increasing."

Integral is in position to act on its confidence; the firm's fourth vintage closed on JPY 123.8bn in December 2020. The fund is the firm's largest to date and highlights the mountain of dry powder expected to keep the middle market humming in 2023.

Polaris Capital Group's latest fund closed on JPY 150bn in late 2020, while The Carlyle Group – which has recently venture more often into more mid-cap territory – raised JPY 258bn for its fourth Japan fund earlier that year.

Meanwhile, a host of corporate PE firms, quasi-strategic joint ventures, and independent spinouts have come online in recent years. The newest of these is D Capital, a digital transformation specialist led by former Unison Capital staff that hit a third close of JPY 27bn on a target of JPY 30bn in October for its debut fund.

Competitive dynamics

PE investment is reflective of recent fundraising action. Total deployments across growth and buyout strategies have reached USD 18.5bn year-to-date, down from the USD 27.3bn put to work in 2021 but well above the annual average of USD 11.2bn for the five years from 2016 to 2020.

The most recent activity also highlights an increasing cross-pollination of large-cap investors in the middle market and vice versa.

Of the 68 deals in 2022 so far, only 16 were USD 200m or more, including a USD 379m acquisition of real estate developer Shinoken by the traditionally midcap-focused Integral. Meanwhile, Bain Capital, architect of Asia's largest buyout to date with Kioxia, acquired advertising consultancy Tri-Stage in April for only USD 89m.

Investors in this space insist that valuations remain stable, however, and will continue to do so next year. This is in spite of a growing number of US dollar-denominated funds targeting the local middle market to exploit a favourable exchange rate. Foreign investors are expected to be even more aggressive in 2023.

Other tailwinds include reasonable availability of mezzanine capital from banks and a recently re-opened border. What happens when China more fully opens up is the incalculable X factor.

Traction in corporate divestments is easier to forecast. Toshiba alone is viewed as a significant potential deal driver next year, but newcomers to the trend appear to be multiplying. For example, Toppan, a 122-year-old printing company, executed its first divestment to PE in April, selling a semiconductor components subsidiary to Integral. More first-timers are expected next year.

"The market will continue growing and there is competition there, but it's not fierce in terms of valuations, which we think have been very stable and reasonable for a few years," said Shinichiro Kita, a senior partner at Advantage Partners, which did at least two carve-outs this year.

"We expect to see some good opportunities in exits, but the IPO market is a concern. We will probably see more secondary deals, including GP-to-GP situations."

Sponsor-to-sponsor exits appear to be a snowballing theme to watch. Activity in recent months includes two sales by Carlyle Japan: construction materials company Senqcia (acquired by Lone Star Funds) and snack maker Oyatsu (acquired by D Capital). Deal sizes were not disclosed, but a source close to the situation said the assets fetched a relatively rich price.

Sponsor-to-sponsor deals in the coming year are expected to be expensive as well if for no other reason than the influx of new funds under pressure to make their mark. Lone Star was said to be motivated in part because it had been unusually quiet for a couple of years. For players such as D Capital, there will be even more pressure to deploy.

"The unfortunate truth and reality is, as a new fund, you're not going to get a lot of love from sellers or the FAs [financial advisors] on the sell side in terms of getting calls for good deals. You have to take what you're given," said one Tokyo-based PE and M&A advisor.

"If there's a deal out there and you have to pay up a bit more than everyone else, you're going to chase it. So, I think a lot of these new funds will be aggressive in chasing these assets that have been held by other funds."

More on North Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.