China fundraising: Onshore vs offshore

Raising capital for China strategies is difficult right now, regardless of currency, but are geopolitical forces enabling the rise of renminbi-denominated funds at the expense of the US dollar?

China's private equity industry is unique in having two separate fund ecosystems, underpinned by different currencies and different investors. The popularity of US dollar and renminbi-denominated funds varies, often in response to shifting regulation, but most mainstream managers with a local presence recognise the value of having exposure to both.

This unusual dynamic creates an alignment of interest dilemma. LPs, especially on the US dollar side, want assurances that one pool of capital won't be favoured over the other. The standard GP response is that US dollar and renminbi funds target distinct opportunity sets, largely driven by foreign investment restrictions and divergent – offshore IPO vs onshore IPO – exit paths.

But US-China geopolitical tensions, and the prospect of economic decoupling, are redrawing the investment map. There is lingering uncertainty around offshore exits, particularly IPOs in the US, and whether foreign capital is welcome in certain high-growth industries. Some local investors believe the investment universe has narrowed for US dollar funds, with renminbi vehicles in the ascendency.

"Internal and external circulation in China are now relatively independent. The US dollar and the renminbi funds are moving further apart in terms of what they can do," said Frankie Fang, founding managing partner of Starquest Capital, which manages fund-of-funds and makes direct investments.

"It's got to the point where some US dollar investors have shifted their thesis from being ‘long on China' to being ‘long on Chinese entrepreneurs' launching start-ups in other emerging markets with similar characteristics."

Cooling on China

It is generally acknowledged that raising US dollar funds for China has become incredibly difficult. Doubts were sowed in the minds of LPs during 2021 as a regulatory blitz clipped the wings of platform internet companies, made online tuition un-investable, and threatened to complicate offshore IPOs. The ongoing flash lockdowns tied to China's "dynamic-zero" COVID-19 policy have done little to inspire confidence.

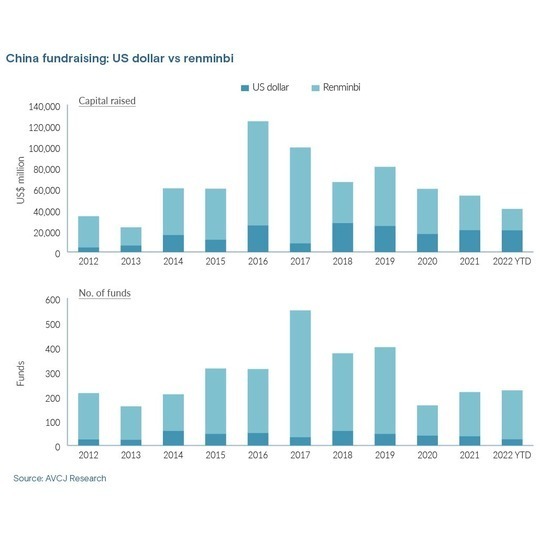

Commitments to US dollar funds amounted to USD 20.5bn as of mid-October, roughly on par with the 12-month total for 2021. However, more than half of that went to a couple of VC managers with strong enough brands to defy the odds: Sequoia Capital China and Qiming Venture Partners collected USD 8.8bn and USD 2.5bn, respectively, for their latest vintages.

It is worth noting that the number of fund closes for 2022 to date – 25, according to AVCJ Research – is the lowest in nine years. Evidence of managers struggling to raise capital abounds.

FountainVest Partners, having hit the hard cap on each of its three previous funds in a matter of months, took 20 months to close its fourth just above target on USD 2.9bn. Similarly, BAI Capital launched its debut China fund in 2020 with every expectation of hitting the USD 750m hard cap. The regulatory imbroglio led to fundraising being put on hold for six months and a final close of USD 700m came in July.

Genesis Capital went to market with its third US dollar fund last year, seeking USD 1.2bn, but progress has effectively ground to a halt, according to a source close to the situation. BA Capital raced to a first close of USD 100m – against a target of USD 150m – for its first US dollar vehicle in 2020. Now, the process has been suspended until next year, a second source close to the situation added.

Others are pre-empting challenges by tweaking strategies and curbing targets. Legend Capital sought to raise USD 500m for its latest technology fund – the same as last time – and then decided to exclude consumer tech and cut the target to USD 400m. Joy Capital's USD 300m target for Fund IV is lower than for Fund III and there is no sign of the accompanying growth vehicle present in the previous vintage.

While there is certainly interest in the renminbi space – KKR recently registered to raise a local currency fund – it is not translating into increased commitments. Fundraising for 2022 to date is USD 20.3bn and it seems unlikely to pass the USD 32.7bn raised in 2021.

The reality is that participation in PE by banks through wealth management products was severely restricted in 2018, prompting a 60% year-on-year drop in fundraising, and the market has yet to recover. Government agencies and state-owned enterprises (SOEs) account for over 70% of capital in renminbi funds. All funds of CNY 10bn (USD 1.4bn) or more are now run by GPs with state-owned backgrounds.

"The problems for China's VC industry are much more serious than in 2018. Market-oriented fundraising is in full retreat. Everyone, including many well-known groups, are having difficulty raising capital," said Yucai Jiang, a vice president of Shenzhen Venture Capital Group, told a conference in August. "The industry must endure 3-5 years of pain. We are just entering the night; we are far from dawn."

This is reflected in the language managers use to describe fundraising. Trustar Capital, previously known as CITIC Capital Partners, announced this month that it had signed contracts amounting to CNY 1.5bn with the first batch of investors in its fourth renminbi M&A fund. No reference was made to the target size or whether there had been a first close.

"Even after the contract is signed, LPs can pull out of a commitment at the last moment or reduce its size, saying that the quota has been exhausted and they must wait for a new one," one local GP explained. "This has a knock-on effect on commitments from other LPs. You never really know whether you can meet your target until the money is in."

Uncertainty over fund commitments from local government LPs has been exacerbated by dwindling land sales amid the property market correction and rising pandemic-related costs. Every major Chinese city saw revenue decline in the first six months of 2022, with Shanghai posting CNY 94bn compared to CNY 380bn in the first half of 2021.

It is also worth noting that 2012-2017 was the peak period for establishing government guidance funds. Many of these vehicles are now entering the exit phase but distributions have been slow to come, making it harder to justify new commitments.

LPs that can make allocations to private equity managers often prefer to back local managers rather than funds launched by international GPs. One local investor recalled being pitched by Morgan Stanley last year regarding a CNY 1bn renminbi fund. They declined and the fund never achieved traction.

"We felt that their strategy was similar to that of other renminbi funds, but they had a preference for star projects, and their localisation is not as deep as that of domestic managers," the LP said.

Servant of two masters

Several private equity firms have tried in the past to operate US dollar and renminbi funds in tandem – investing in the same assets on a pro-rata basis. This was the plan when CDH's rolled out its venture growth strategy in 2015, but it was rendered impractical by China tightening controls on capital outflows and failing to push ahead on smoother approvals process for foreign investment.

Similarly, Trustar's efforts to deploy the US dollar and renminbi tranches of its third fund in synch were complicated by a flurry of offshore investment activity and uncertainty over regulatory approvals for renminbi participation. Deployment from the US dollar tranche outpaced the renminbi tranche. There was no parallel local currency vehicle alongside Fund IV.

Some managers do draw capital from both pools for deals, but many industry participants see US dollar and renminbi strategies as fundamentally different. The former are internet platform backers that like to write large cheques for big stories, prioritising innovation and less sensitive to valuation; the latter have shorter investment cycles, which leads to an emphasis on mature companies, cash flow, and profitability.

These are highly generalised characterisations, but they feed perceptions that some small and medium-sized enterprises now favoured by China's policymakers for their role in addressing critical bottlenecks – often under the domestic substitution theme – wouldn't meet US dollar fund criteria in terms of addressable market or upside.

"After IPO, such projects could have market capitalisations of CNY 4bn-CNY 30bn, which might be too small for US dollar investors. But for us, entering at a valuation of CNY 200m-CNY 300m and exiting at CNY 7bn-CNY 8bn, that's a good fit. It translates into a ticket size of several tens of millions of renminbi," said Peter Yin, founding managing partner at Inspiration Capital.

Sensitive sectors

The impact of regulation on strategic divergence, meanwhile, is multi-faceted. Web3 and crypto start-ups have no option but to operate offshore, so they will take US dollar capital. Consumer-facing internet has faded, partly because of the regulatory upheaval last year, and so US dollar investors are looking at exporting these business models to other emerging markets.

Deep-tech plays like semiconductors are regarded as renminbi plays because offshore capital, while not excluded from this area, is less popular with founders. However, this is a point of contention, with some US dollar investors arguing that their access is uninhibited.

"As a dual currency GP, it's easier to answer the question of alignment of interest today because the two sides have clearly different roles," said Michael Yao, a partner at ZWC Partners.

Dual-currency GPs claim to use a single strategy for both currencies and break down investments by sector. However, certain sector teams are more likely to deploy renminbi than US dollars. "If you add a semiconductor investment, it's probably going to be on the renminbi side," observed Yipin Ng, a managing partner at Yunqi Partners.

Eric Gao, founder of semiconductor-focused financial advisor Winsoul Capital, endorses the view that companies in this sector are wary of taking US dollar capital. The potential impact on IPO prospects and market expansion are key considerations. The more sensitive the technology, the more heightened the concerns. Anything with military-industrial applications or government customers is for local investors only.

One Shanghai-based technology investor that recently led a funding round for a semiconductor specialist focused on 55-nanometre lithography used to make chips for the automotive industry recalls discussing with the founder whether US dollar investors should be included. They concluded that the technology was not too sensitive, but put a plan in place to remove these investors should regulatory issues emerge.

"Deep-tech players like semiconductor start-ups often dare not take US dollar funding and they don't need it. Many renminbi funds are willing to back them. When it comes to US sanctions and the likelihood of an onshore IPO, it's not only the company founder but also renminbi investors in the same round that will consider the various scenarios and share their views," the investor explained.

A Beijing-based LP active in the US dollar space confirmed that for sensitive areas like semiconductors, portfolio GPs tend to invest through renminbi funds. "At least, they don't need to force us out when US regulation tightens," the LP noted.

Despite the regulatory issues for the semiconductor industry emanating from both China and the US, some of the best-funded start-ups – such as Biren, Enflame, Moore Threads, and Iluvatar CoreX – have received capital from US dollar funds managed by the likes of Sequoia Capital China, Primavera Capital, IDG Capital, GGV Capital, and Centurium Capital. However, the largest deals tend to be in renminbi.

There are two ways for US dollar funds to participate in renminbi-denominated rounds. First, the start-up is asked to switch designation from a pure domestic entity to a joint venture that can accept onshore and offshore capital. Second, the GP converts US dollars into renminbi through the Qualified Foreign Limited Partnership (QFLP) scheme. Entrepreneurs wouldn't necessarily be able to tell the difference.

"There are indeed more and more people looking to use the QFLP channel, but few have exited through it. Compared to the JV structure, QFLP is a pilot program that has more uncertainty," said Mulong Gong, a Beijing-based managing partner at law firm King & Wood Mallesons. "Its accessibility can vary based on foreign exchange regulations in different cities."

He added that QFLP operates at the fund level, not for single deals, and structures take more than six months to implement, compared to one or two months for JV structures. At the same time, while QFLP uses renminbi to invest in deals, it cannot access sensitive sectors because regulators look through the structure to the ultimate beneficial owners.

The Beijing-based LP active in the US dollar space observed that the tax treatment for QFLP is not as clear as it is for JVs, which are subject to a 10% withholding tax upon exit.

In other areas, renminbi and US dollar investors may participate in different parts of the value chain. The supply chains for robotics and advanced manufacturing, for example, are largely in China but customers are often overseas. This means renminbi funds can invest in the technology and US dollar funds can target the outbound expansion phase.

Enduring the winter

Investment has slowed across the board in 2022; even industries such as semiconductor and artificial intelligence, which had received USD 11.8bn as of mid-October compared to USD 21.6bn for the full 12 months of 2021. Investors note that little happened in the second quarter when Shanghai was locked down. "Closing announcements were mostly from the first quarter or the end of last year," said one GP.

At the same time, for all the talk of US dollars becoming less of a force in China, managers generally prefer that currency when fundraising. Offshore LPs are regarded as a more reliable source of capital that will re-up across several vintages, whereas their onshore counterparts are more like momentum investors. They follow the prevailing market theme and back a new round of GPs whenever it shifts.

"Local investors essentially rotate through the sectors. If a GP is not investing in the hot theme of the day, how can it be expected to raise capital?" one local government LP observed.

In addition, US dollar investors are known for executing stricter due diligence, but also for respecting the autonomy of the GP and not interfering in daily operations. Moreover, unlike government guidance funds, there are requirements that investments must deliver value to certain cities or provinces – although there can be scope for negotiation in this area.

Regardless, Inspiration refused to accept some guidance funds in its latest renminbi vehicle, which closed recently on CNY 600m, because it wanted to focus on market-oriented opportunities and not be encumbered by investment-back requirements.

It is hoped that some best practices from the US dollar side will find their way into the renminbi ecosystem as local GPs and LPs become more sophisticated. However, politics and regulation appear to be the key forces in directing their trajectories and the extent to which these may converge and diverge.

Following the latest round of US sanctions on China's semiconductor industry, the Beijing-based US dollar LP fully endorses the domestic substitution play, noting that backing the likes of Biren makes sense because the company's strongest US competitor won't be able to supply China. Exposure comes with risk, but this is manageable if these deals represent a small portion of the portfolio, the LP added.

Equally, others take the view that these shifts represent a temporary phenomenon and that, ultimately, US-China decoupling in high-end technology cannot be fully realised. Both sides emphasise opportunity rather than restriction, underscoring the fundamental optimism of investors.

"In 10 years, there may indeed be two systems and two markets, but that's all. It doesn't mean they won't communicate or invest in each other," said Jenny Zeng, a founding partner of MSA Capital.

"Chinese innovation has brought huge returns to LPs in the US and Europe, and most international investors make decisions independently rather than follow the will of government. I think that from the first quarter of next year, commitments to US dollar funds will start to recover."

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.