Deal financing: Homegrown solutions

Private equity firms are relying more heavily on Asia-based debt investors to support leveraged buyouts amid a loan logjam in the US, highlighting the region’s innovation and durability

The end of America's recent long weekend Labour Day holiday signals the start of a crucial few weeks for the leveraged loan market – and for private equity sponsors in Asia and elsewhere that want to tap the US markets for debt to support new deals.

It is estimated that banks are sitting on USD 30bn-USD 40bn in positions they underwrote prior to the Ukraine war and haven't been able to syndicate amid weakening investor demand. These must be cleared; it's just a case of how deep the discounts will be and how long the process will take.

"There is a huge amount of paper that will be launched and syndicated in September. We expect that volume will help free up limits for many arranging banks and that the market's ability to underwrite new deals will be more feasible going forward," said Andrew Ashman, head of the Asia Pacific loan syndicate team at Barclays.

Investors and lenders alike will be watching for indications of where the market is moving. They will track not only the largest outstanding deal – a USD 16.5bn take-private of Citrix Software by Vista Equity Partners – but also the likes of media ratings agency Nielsen Holdings and auto parts maker Tenneco, which come from industries deemed less recession-proof. Macro concerns are paramount.

"The Ukraine war accelerated the impact of inflation, but now there's the broader point around the probability of a recession in the short to medium term," said Peter Graf, a managing director at Ares SSG who focuses on direct lending in Australia and New Zealand.

"Investors are debating how many more interest rate hikes there might be, what would be the impact in terms of cost of borrowing if they continue to go up, and what this means for companies in different sectors."

Over the past six months, leverage loan indices have fallen from close to par to the low 90s and then back to around 95. This implies that investors can pick up debt in the secondary market at a 5% discount to net asset value, so there is little incentive to support new deals. As one Asia-based financing executive with a global private equity firm puts it: "The US markets are effectively closed."

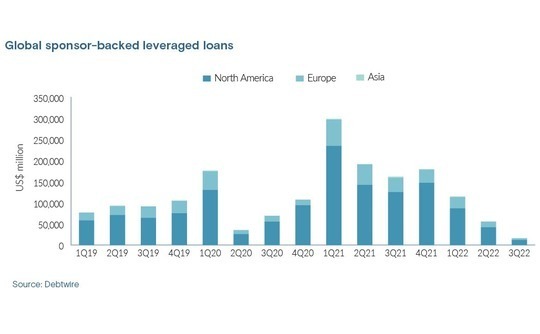

Global sponsor-backed leveraged loans in North America reached USD 650bn last year, according to Debtwire, AVCJ's sister title. The running total for 2022 is USD 140.8bn, with more than 60% of that transacting in the first three months. Europe, where volume hit USD 174.7bn in 2021, has followed a similar trajectory: a first quarter of USD 25.2bn and a second quarter of USD 13.2bn.

Exceptional cases?

In an Asia context, the direct impact has been relatively small. While the US term loan B (TLB) market is generally preferred to locally sourced bank loans for its generous leverage levels, longer tenors, and bullet repayments instead of gradual amortisation, it is not a realistic option for many sponsors.

"The US TLB and high yield bond markets are harder to access than before, but they were only ever servicing part of the market, typically high-quality PE sponsors and large-cap deals. Most of the market is Asia TLA and unitranche and those remain accessible," said Daniel Abercromby, a partner at White & Case.

The fact that Asia has remained open for business while other markets have not is inextricably tied to banks being the region's major leveraged lenders rather than institutions. Indeed, some sponsors have turned the situation on its head and distributed US TLB loans to those Asia-based investors.

Tricor Group offered a glimpse of what was possible when its USD 2.7bn acquisition by Baring Private Equity Asia (BPEA) was supported by nearly USD 1bn in debt, including a US TLB. A large portion of the deal went to Asian accounts, according to a source close to the situation. The transaction was agreed in late 2021 and the financing closed in February, two weeks before the Ukraine war began.

They are stable, cash flow-generative businesses backed by high-quality sponsors, and in each case, the TLB took out an existing Asian bank loan, so due diligence was relatively straightforward.

Moreover, both companies are well-known to lenders. Tricor was owned by Permira before BPEA and went through four financing events during a five-year holding period. HCP, meanwhile, is now on to its third private equity owner – and sixth financing event – in 10 years. Its Taiwan heritage translates into popularity with Taiwan lenders, who are among the region's keenest buyers of leveraged loans.

"The Asian market is very different. Syndication is mainly to other commercial banks, rather than CLO [collateralised loan obligation] funds, and the challenge is you don't have the financial covenants and other standard protections of a TLA," said Manas Chandrashekar, a partner at Kirkland & Ellis.

"In those deals, banks knew the assets, went through the creditor protections, and put their hands up for the debt. Whether this can be replicated on other deals depends on the asset's linkages to Asia and familiarity in the Asian leveraged loan market."

Incremental progress

The case for exceptionalism is emboldened by the experience of VXI Global Solutions, a call centre provider with a substantial China footprint that Bain Capital acquired from Carlyle for USD 1.2bn. A USD 615m TLB got stuck in syndication in the US market, so the focus switched to distribution in Asia, but progress has been slow, according to three sources familiar with the situation.

At the same time, an argument is made that TLB is following the same path to unitranche, which gained traction in Australia and then spread upwards through Asia, partly because products were pitched at Asian banks that bought up some of the Australian debt alongside local institutions and private debt funds. In due course, the Australian TLB took hold as an alternative to the US markets.

John Corrin, head of global loan syndications at ANZ, is cautiously optimistic about the development. "Slowly but surely, it appears that TLB is being accepted by Asian investors, so hopefully, those situations will increasingly not be exceptions to the rule," he said, while adding two caveats. First, deal flow has slowed down in recent months. Second, TLB will never be suitable for all transactions.

The issue of suitability has demand and supply angles. Sponsors opt for bank financing instead of TLB for transactions with relatively low leverage, or target companies might be uncomfortable with the level of marketing and disclosure involved. On the supply side, it is generally accepted that anything below USD 500m in senior debt won't fly, although that applies to institutional investors only.

TLB becomes a necessity for mega deals where local capacity becomes constrained. Chinese banks are a random factor in this equation, given their track record of extending USD 1bn-plus TLA for deals seen as being of national relevance and then lengthening the tenor and diluting the terms – no amortisation, one very loose covenant – so that it looks more like a version of TLB.

However, they are notoriously inconsistent, with White & Case's Abercromby noting that sponsor-friendly terms suddenly disappear when aggressive-lending banks fill their books.

Ramsay's dilemma

Australia is a more instructive example given local pools of capital are relatively shallow. The inability to access US TLB has called into question one of the largest take-privates anywhere in Asia: KKR's AUD 20.1bn (USD 13.6bn) bid for hospital operator Ramsay Health Care.

The deal is up in the air after KKR withdrew its indicative proposal at the end of August and put forward an alternative – which the Ramsay board has rejected – that removes the need for access to non-public information on Ramsay's separately listed European subsidiary. Still, there is some doubt as to whether the deal could proceed without offshore financing.

According to Russell Sinclair, head of Australia debt and capital advisory at PwC, local financing is challenging for debt packages above AUD 1bn. In normal circumstances, this wouldn't have been a problem for Ramsay. KKR was always expected to leverage the company's global status – most of its revenue is outside of Australia – and tap US TLB and euro high yield markets as well as local sources.

A potential solution might be found in the real estate that sits on Ramsay's books. The company owns 54 of the 72 hospitals and surgeries in its network, with Macquarie estimating after the initial bid was announced that the sale-and-leaseback opportunity could be worth up to AUD 8.7bn.

"Where there is a real estate component, it is possible to create an opco-propco structure, and then get real estate debt financing against the propco with a cheaper cost of capital because it is asset-backed. Debt financing can be obtained separately for the opco, which is the operating entity that uses those assets to generate cash flow," said Krish Vaswani, a member of Partners Group's Australia private debt team.

"Alternatively, an investor could take full ownership of the company and do a sale-and-leaseback of the real estate assets."

The Blackstone Group's AUD 8.9bn take-private of Australian casino operator Crown Resorts, which closed in June, featured a AUD 5.4bn unitranche facility provided by real estate investor Starwood Capital Group and debt funds affiliated to Blackstone.

Going back to 2019, Brookfield Asset Management's USD 4.1bn acquisition of hospital operator Healthscope included USD 1bn in equity, USD 1.4bn in long-term debt funding, and USD 1.7bn generated from the sale and leaseback of 22 freehold hospital properties.

"You're not asking for USD 10bn in TLB market capacity," said one private debt investor. "A lot can be done in creative structuring, but it's harder and more expensive in volatile market conditions."

As such, given a binding offer for Ramsay has yet to be finalised, some industry participants expect KKR to bide its time. "I wouldn't be surprised if they turned up with a US TLB in 30 days when the markets have cleared," said the Asia-based financing executive with a global private equity firm.

Guessing games

This raises the question of how quickly the turnaround is likely to take, and what this means for the role played by Asian investors. Drawing meaningful conclusions is complicated by a lack of deal flow.

One problem is that private equity firms have turned gun-shy. Several leveraged lenders note that sponsors are pulling out of processes they initiated months ago, unable to reconcile the valuations contemplated then with the equity market volatility and business model vulnerability they see now.

Lenders have also become warier. Vaswani of Partners Group highlights how deteriorating economic fundamentals necessitate a re-underwriting of existing portfolios and a reconsideration of new transactions, especially those involving companies that now are only just able to cover interest payments. The switch to risk-off is most visible in more volatile segments, such as Australian TLB.

"In the US and Europe, if banks wanted to take risk, they would ask for wide flex terms, which is often unattractive to sponsors. That has found its way into Australia. A handful of transactions closed just before markets went risk-off and it is likely that banks are now struggling to syndicate them," Vaswani added.

Unitranche markets and TLA markets remain active throughout Asia, but borrowers are on a tighter leash. Leverage for a TLA has been pared back to 4.5x from 5-5.5x and pricing might have increased 50 basis points. Leverage for unitranche remains in the 6x-6.5x range and pricing is still a few hundred basis points above bank debt, given unitranche is single covenant with lots of headroom.

There is also evidence of a flight to safety in terms of sectors, with healthcare and software at one end and consumer discretionary at the other, while Graf of Ares adds that lenders are being less aggressive on documentation than five months ago. This means reduced leeway in areas such as incremental debt capacity, dividend payments, asset sales, EBITDA adjustments, and step-downs.

"Having the right amount of protection in the documentation might be more valuable than getting a better price," he said. "You want the right credit at the right leverage level, and price is the discussion after that. If leverage remains where it was before, it's binary whether you do the financing or not."

Diversity delivers

When the US TLB backlog is cleared and new deals begin to flow again, the response in Asia might be delayed. Corrin of ANZ suggests that the same banks will be reluctant to take on the extra risk premium of Asia and nudge global sponsors towards TLA instead. Meanwhile, a surge in US and European take-privates is expected later this year as GPs capitalise on public market volatility.

No one doubts the ability of the market to bounce back and recapture some of its former excesses. If there is a lasting impact of the recent malaise, it might be revealed in heightened macro sensitivity, leading to closer examination of relative value and more frequent bouts of risk-on and risk-off.

In this regard, the emergence of more financing options within Asia is helpful. Unitranche has demonstrated the fastest growth, with global credit investors adding headcount in the region and earmarking more capital for deployment here. Several sources put the top-out level for a unitranche deal in Asia at USD 500m, but then qualified their responses and said it might be twice that figure.

TLB has nothing like that level of traction, but Chandrashekar of Kirkland & Ellis is encouraged by the fact that Asian investors are willing to "look past their standard asks, even for specific assets," noting that the market has been constrained by TLA products for a long time.

It's unclear what will happen when the US market re-opens, and investors acknowledge that long-term development hinges on the creation of a true institutional leveraged finance market in Asia. But there is a sense that the region is moving in the right direction.

"The more diversity in the bank group, the better execution in syndication, while increasing diversity across US and Asian lenders can drive improved pricing for borrower," said Ashman of Barclays. "Building strong demand across the two markets leads to a better outcome for the sponsors."

More on Australasia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.