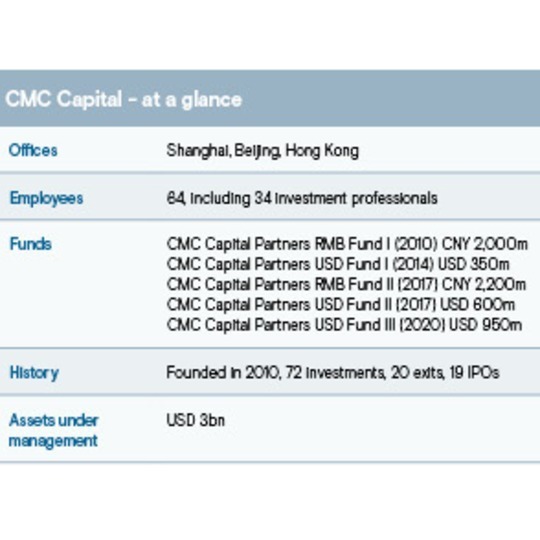

GP profile: CMC Capital Partners

China-focused CMC Capital Partners’ remit has expanded from media to consumer and technology, but the firm believes its knowledge and discipline as a specialist investor have never been more relevant

For Tony Han, CEO and co-founder of Chinese autonomous driving pioneer WeRide, achieving a valuation of USD 4.4bn earlier this year was cause for reflection.

Though blessed with a founding team drawn from Baidu, Didi Chuxing, and China Auto, the company's ascent has been far from smooth, with several near-death situations along the way. It courted controversy from the outset, when Jin Wang, the Baidu alumnus, departed following a dispute with his former employer.

Fast forward two years to 2019 and WeRide's cash reserves were so low it was eight months from bankruptcy. Salvation came in the form of a USD310m Series B and collaboration on an autonomous minibus with electric bus manufacturer Yutong Group, which led the round.

"After all the setbacks, we were once again endorsed by mainstream investors," said Han. "After that round, fundraising was much easier."

CMC Capital Partners was one of the participants in the Series B. The firm was interested in level-four (L4) autonomy – where there is still a driver in the seat, but the vehicle is fully autonomous in certain environments – and left no stone unturned in its research.

More than 40 experts, from carmakers to technology suppliers to regulators, were interviewed, as well as almost every major player in the space. This led to test drives with Pony.ai, AutoX, and DeepRoute.ai, meetings with the autonomous driving teams at Baidu and Didi, and even dialogue with robotruck specialists like Plus.ai and Inceptio.

"We concluded that robotaxis could achieve commercial landing in China faster than robotrucks. With the right policy support at city level, you run road tests using hundreds of vehicles, collecting data," said Alex Chen, a partner and CIO at CMC Capital.

"As for long-haul trucks, it isn't clear who is in charge of the Beijing-Shanghai highway. This is in contrast to the US, where policies tend to be set at state level, and most states have allowed robotruck testing or commercial operation."

Having narrowed it down to WeRide and Pony.ai, CMC Capital went with the former, citing a more reasonable valuation and a more open approach to due diligence. Han recalls Chen not only interviewing his management team, but also going deep into technical detail with the engineers. One exchange on a very specific topic lasted an entire morning.

"They weren't following a trend, they wanted to understand the whole industry, how everything works, and how your technologies rank against global competition. They even studied our upstream and downstream suppliers to see what kind of LiDAR and chips we use, and which companies provide use with vehicle platforms," said Han.

While TuSimple, a Chinese robotruck specialist with extensive operations in the US, was also considered viable, CMC Capital passed on the deal. Pandemic-driven travel restrictions were in place and Chen was uncomfortable investing based on a few video conferences.

Industrial expertise

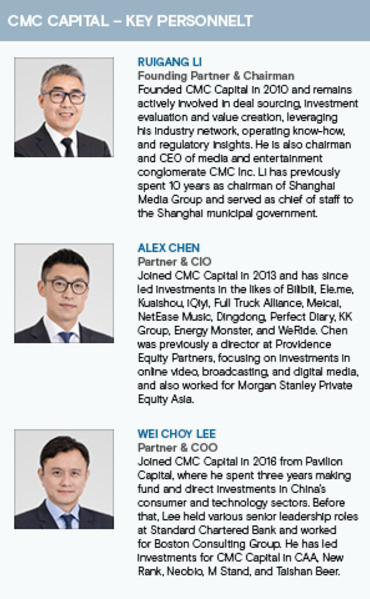

As an industry-focused investor from the outset, CMC Capital considers in-depth due diligence part of its DNA. Ruigang Li, the firm's founding partner, describes pure financial investors as no different from banks: one provides equity and the other offers debt, but there is no industry angle and neither party contributes in terms of value creation.

"You must be rooted in the industry and participate in the growth of the enterprise, from the iteration of its organisation and management, to the business development and product innovation, as well as government relations, media relations," he explained.

"You get profound insights of the industry from deep interaction with portfolio companies and other players in the value chain, and you can use your understanding and various other resources to empower other companies or participate in strategic plays."

Li is one of China's best-known media moguls, having spent a decade as president of Shanghai Media Group. Under his tenure, the company launched the country's first internet protocol television service, which was spun off as BesTV Media and went public in Shanghai in 2011 as China's first new media stock.

The decision to launch a private investment firm, which came in 2010, was driven by a desire to participate in technology-enabled transformation. CMC Capital was originally known as China Media Capital and it pursued deals across media and entertainment. The first investment was the acquisition of a majority stake in Star China TV from News Corp.

The third US dollar fund closed on USD 950m in early 2020, with commitments from the likes of public pension funds, sovereign wealth funds, insurance companies, financial institutions, endowments, fund-of-funds, and family offices from around the world.

Early successes included IMAX China. The movie theatre operator was struggling to gain market share in China, so Li flew to the US and persuaded the CEO to spin out the local entity and have it pursue an independent strategy. IMAX China was founded in 2012 with CMC Capital as a shareholder. It secured a 4x return following the company's Hong Kong IPO in 2015.

Nevertheless, the firm soon began to reconfigure its investment approach. Media and entertainment deals were divided into two categories, content creators and platform operators. The former stopped, given the high level of uncertainty, and the latter came to the fore. CMC Capital went on to back video platforms Kuaishou, Bilibili, and iQiyi, as well as comic specialist Kuaikan, NetEase Cloud Music, and Mango TV.

A consumer launchpad

From here, the firm moved into the broader consumer space. "Platforms provide content consumers, with mobile internet as the underlying technology infrastructure, so expanding into the consumer field was very natural," said Li. "It's about serving the same people with the same technical framework, just shifting from a spiritual product to a physical one."

E-commerce service provider Leqee is a good example of this evolution. The company – founded in 2009 by Colin Huang, who went on to establish Pinduoduo – offered end-to-end enablement services for online sales. CMC Capital joined a Series B round in 2018.

However, by 2020, five-year-old Pinduoduo was challenging Alibaba Group's local supremacy as an online marketplace. Leqee was effectively caught in the competitive crossfire, its background deemed an impediment to serving customers through Alibaba-owned Tmall. CMC Capital duly became the largest shareholder, to the satisfaction of both sides.

Investing in Leqee, a broad-based e-commerce service provider, rather than a narrower software-as-a-service (SaaS) platform says much about CMC Capital's philosophy. It favoured Leqee's focus on large customers, its stable growth curve, and its immediate profitability.

"For SaaS providers, KPIs [key performance indicators] can grow very fast, but also drop just as fast," said Kai Liu, president of Leqee. "We like to focus on large customers. While it's difficult to acquire them, once the relationship is in place, you're firmly tied to customers."

At the same time, the standardised SaaS products aimed at small and medium-sized enterprises (SMEs) are less of a draw for larger customers, which prefer customisation. Leveraging its strength in the beauty and baby products categories, Leqee tends to co-develop solutions with customers that have strict data security and privacy requirements.

Elsewhere, CMC Capital's historical roots in media and entertainment still resonate. Almost replicating the IMAX model, it established a China joint venture in 2017 with US-based Creative Artists Agency (CAA), which represents actors, directors, writers, and producers.

Then there is CMC Inc, previously CMC Holding, which was formed in 2015 with CNY 10bn in funding from Oriza Holdings, Tencent Holdings and Alibaba. It was devised as a platform for investments with a horizon of more than 10 years, ranging from entertainment real estate developments to a stake in the holding company of Manchester City Football Club.

However, CMC Inc has since evolved into more of an integrated media and entertainment group. Its members and affiliates include film producers Daylight Entertainment and CMC Pictures, Hong Kong-based TVB and Shaw Brothers, fashion and lifestyle-focused Huasheng Media, and investigative journalism platform Caixin Media.

"Our reach in media and entertainment is well-known. It is part of us. We have close ties to the industry and these can be of benefit to all our portfolio companies," said WeiChoy Lee, a partner and COO of CMC Capital.

"For example, if a company runs into difficulty with a brand upgrade, we can provide advice and access to resources like brand ambassadors. The cooperation we facilitate is efficient because it is based on mutual trust."

Unavoidable technology

CMC Capital's expansion from media into consumer and then into technology was equally fluid. Technology providers have always loomed large over both sectors, given the use of algorithms to recommend content and acquire and analyse users, Li contends.

Following this logic, the firm made inroads into software and digitalisation, backing the likes of robotic process automation (RPA) provider Cyclone and corporate reimbursement and expense management tool Maycur. Hardware came next with WeRide and unmanned mining transportation provider Tage.

It raises the question as to whether CMC Capital, having moved far beyond its traditional areas of coverage, can still offer differentiated resources to technology companies.

"Whether we can help a company is one of the considerations when we decide whether to invest in it," said Chen. "Each investment is an opportunity for us to expand into a certain industry, so building close relationships with companies is an important factor."

Brand support and customer introductions are part of the package, including government relations. CMC helped WeRide expand from its Guangzhou powerbase by connecting the company to authorities in Nanjing, Wuhan, and Shanghai. A commercial landing deal – which will feature robo-minibuses – was recently agreed with Shanghai's Lingang district.

Sometimes, the influence is incredibly subtle. Li recognised where Chinese regulators were moving on data privacy and briefed Han on the matter. Months before Didi's data breach investigation, WeRide invested nearly CNY 10m in data masking, which is used to identify and delete sensitive data such as faces and license plate numbers.

CMC Capital is determined to build on its domain expertise in areas like artificial intelligence. To this end, it co-founded the Shanghai Digital Brain Institute with Jun Wang, a professor at University College London and formerly chief scientist at Huawei Technologies' Noah's Ark Lab. The GP contributed internal capital to become the major shareholder in the project.

"The initial goal was to gain knowledge of the field, generate insights into challenges start-ups may encounter, and empower portfolio companies with its algorithms," said Lee.

"But it is also an independent business that we want to bring to the capital market one day. Our experience in the front-end market can help these scientists develop business scenarios and negotiate cooperation agreements. The institute itself can be profitable."

Risk awareness

CMC Capital's key technology investment themes are software-related enterprise digitalisation, smart mobility, and smart manufacturing. It has engaged with more than 30 companies in smart manufacturing since 2019 but has yet to pull the trigger because the gap between technological readiness and expected valuations is still too wide.

For example, on studying warehouse automation, Chen found that upfront investment by users was high, the extent of human substitution was unclear, and payback can take up to four years. Most start-ups are still loss-making because sales have yet to reach critical mass.

One company he spoke to was looking to raise capital at a valuation of more than USD 1bn based on projected revenue of CNY 600m. Actual revenue has half that figure.

"In the past, the mobile internet investment was traffic-driven. If traffic indicators like user numbers and time spent online were rising, valuations continued to increase," Chen added. "But you can't apply the same logic to a hard-tech or consumer company. If they are unprofitable and keep on burning cash, they will never be sustainable."

China has felt the brunt of a sharp contraction in valuation for growth-stage technology companies in the past 18 months, driven by a combination of domestic regulatory uncertainty and sell-offs in listed markets globally. CMC Capital is not unduly worried, noting that herd-like changes in investor consensus create volatility but don't invalidate business models.

Robotics appears to be the latest consensus play. However, Chen observes that as recently as the second half of 2019, investors were bullish on new retail thanks to brand development approaches based on online traffic. Excessive capital enabled intense and unsustainable competition, the market wobbled, and investors moved on.

Even though new retail and emerging consumer brands are no longer a hot concept, CMC Capital continues to look for deals in the space. It also remains confident about the prospects for existing portfolio companies like e-commerce beauty brand Perfect Diary.

"If we thought that Perfect Diary was an e-commerce company that could only work on Little Red Book and Douyin, we wouldn't have invested. Channel marketing is one of its core competencies, but during our due diligence period, Perfect Diary has built its own factory on the supply chain side, formed a strong team on the product development side, and was opening offline stores," said Chen.

"The company has end-to-end capabilities and that is a critical point. A consumer company cannot rely on just one area, it would be too vulnerable."

Confidence has been buoyed by sales of Perfect Diary products by offline retailer KK Group, another CMC Capital investee. However, Chen accepts that rapid fundraising at increasingly elevated valuations led to damaging pressure. Perfect Diary became too reliant on traffic as part of efforts to boost top-line revenue and its development rhythm was disrupted.

As CMC Capital looks to raise its fourth US dollar fund, technology and consumer remain the core focus areas, with entertainment treated as a consumer sub-sector. It is hardly an opportune time for China managers to be raising capital with LPs wary of the broader commercial and regulatory environment and exits still elusive.

Li believes that the current uncertainties around Chinese companies listing in the US will be resolved in time. However, recent experiences have heightened the need for diversified exit paths. Of CMC Capital's 21 exits, realised proceeds from IPOs total USD 487m with USD 669m coming through M&A, trade sales, and redemptions.

"You cannot rely entirely on IPOs and exploring other channels like trade and secondary sales tests an investor's understanding of different industries," he added. "Making a deal happen often depends on that domain expertise."

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.