Japan carve-outs: Improving the old

Private equity investors are keen to acquire mature but unloved assets from Japanese corporates and reposition them for growth. Execution is seldom straightforward, and size often means complexity

KKR is determined to fix Marelli. The equity portion of its USD 4.5bn acquisition of Japanese auto parts manufacturer Calsonic Kansei Corporation in 2017 has already been written off. Meanwhile, two new tranches of equity have been pumped in: one in 2020 when Calsonic, rocked by COVID-19 while still adjusting to a USD 7.1bn merger with Europe's Magneti Marelli, refinanced its debt; and another earlier this year as part of a restructuring.

The latter action – a two-stage process that saw KKR reappointed as Marelli's sponsor on the strength of its revitalisation plan – involved convincing banks to forgive JPY 450bn (USD 3.2bn) out of a JPY 1.1trn debt pile. The private equity firm's equity contribution at this juncture was USD 650m.

"With the greater financial stability provided by this revitalisation plan, I am confident the team at Marelli are well placed for the future," Hiro Hirano, co-head of Asia Pacific private equity at KKR and the firm's Japan CEO, said on announcing the capital injection.

"The automotive industry has faced unprecedented challenges over the last couple of years, and KKR is determined to work together with Marelli to improve its global operations and return to growth."

KKR has completed seven corporate carve-outs in Japan since 2010; Calsonic Kansei, previously a listed subsidiary of Nissan, was the fifth. The GP and its peers have spent years preparing for the trickle of non-core divestments by corporate Japan to become a flow, making their case as good custodians of those assets. No one wants a black mark against their name.

Marelli amounts to an extraordinary tale of misfortune. KKR's plans to drive change in the business have seemingly been thwarted at every turn by pandemic-driven factory shutdowns, global semiconductor shortages, and rising raw material costs. Freak events like factory fires, extreme weather events, and the arrest of Nissan chairman Carols Ghosn can also be factored into the mix.

At the same time, it underscores the inherent risks of corporate carve-outs in Japan even as GPs set their sights on ever-larger targets. These undermanaged and underinvested assets represent a huge value creation opportunity, but execution is akin to steering a tanker. If enough things go wrong in a business that might be relatively low-growth and highly leveraged, it is difficult to get back on course.

"These are competitive auctions, so the winning bidder has underwritten a meaningful amount of value creation already – they aren't buying the business for current profit and a few percent of growth. There's a lot of pressure to improve profitability," said Jim Verbeeten, a partner at Bain & Company. "You also need to do stress testing because you never know what might happen."

Low-hanging fruit?

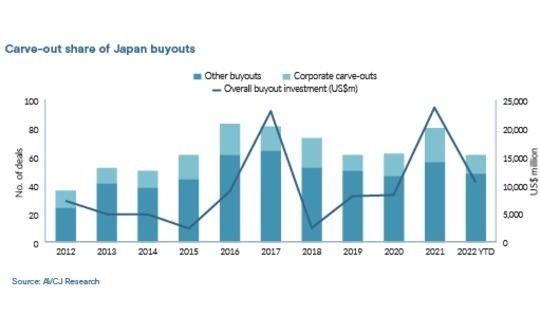

The carve-out share of Japan buyouts over the past 10 years is around 25%. It has been consistent during this period, tracking broader private equity investment trends. AVCJ Research has records of 24 transactions of this kind in 2021, only the third time deal flow has surpassed the teens.

What they lack in volume, carve-outs make up for in value. This is in part driven by the circumstances of the seller. Japanese corporates are under pressure from all sides – lenders, regulators, institutional shareholders, activist investors – to deliver performance rather than scale; and when forced to divest something, they prefer transactions that make a meaningful impact on the balance sheet.

Advisors name about 10 offshore players, plus a few local GPs, as credible bidders for these assets. Bain Capital recently overcame competition from at least three rivals to secure a JPY 427.7bn medical devices carve-out from Olympus Corporation. Meanwhile, Toshiba received eight privatisation bids and two minority investment proposals, most of them backed by financial sponsors.

That isn't necessarily difficult, given the characterisation of non-core assets as uncompetitive, inefficient behemoths helmed by ageing salarymen who prioritise expense accounts and golf club memberships. They have essentially been cast adrift within the conglomerate structure, the parent redeploying whatever cash is generated and leaving nothing for growth.

Not all carve-outs start from the same point. Hitachi Metals, which is subject to a JPY 816.8bn tender offer from a Bain Capital-led consortium, is a listed entity with a freestanding corporate structure. However, size brings complexity. The company is almost a conglomerate in and of itself with assorted subsidiaries that often have little in common and could be divested.

At the other end of the spectrum, last year J-Star – which typically makes investments of JPY 1bn-JPY 3bn – acquired a waste management business from NEC Corporation. Greg Hara, the private equity firm's CEO and managing partner, said that turning the business into a standalone entity, notably the personnel and systems elements, represented a significant challenge.

Typical early assignments include installing proper corporate infrastructure: SG&A (selling, general, and administrative expenses) reporting; systems that track money flows by customer, region, and product; and key performance indicators (KPIs) that can be used to hold everyone accountable.

To begin with, management might be augmented rather than replaced, for example by bringing in a professional CFO or a hands-on chairman. Ultimately, there could be redundancies, but these are accompanied by initiatives to promote, empower, and incentivise younger talent.

"There are talented and motivated people, but the incentive structure is different to the US and Europe, where people have shares in the company, so they look beyond annual compensation and care about long-term growth. In Japan, they have less skin in the game. The right incentive schemes can help change behaviour," said Tatsuya Ochi, head of Japan private equity at Partners Group.

There is a need to disentangle the business from its former parent, but also maintain some form of dialogue. This should be business-like, with the separated entity choosing which services to purchase, said Tom Noda, a managing director at AlixPartners, although he noted that redrawing relationships along commercial lines means breaking entrenched habits.

Cost reductions can be wide-ranging, but often include phasing out less profitable business lines and focusing on a concentrated number of perceived winners. This gives shape to mid-term strategic plans and growth-oriented investment programmes that had previously been lacking.

"You need at least 18 months to start seeing real effects and that initial period should be high impact in terms of management, systems, culture, strategy, and business plan change," said Mark Chiba, a partner and group chairman at mid-market buyout player The Longreach Group. "Solid outcomes may emerge after three years, but all-in you might want to hold an asset for 4-5 years to harvest returns."

Bolt-on bonanzas

The Carlyle Group went through this process with Senqcia Corporation, a supplier of earthquake-resistant building materials it acquired from Hitachi Metals in 2015 and recently agreed to sell to Lone Star. The GP claims to have installed a more flexible organisational structure, divested non-core assets, revised pricing strategies, and established new business lines.

According to Kazuhiro Yamada, head of Japan at The Carlyle Group, after that initial 18-month period of change, it is standard practice to consider bolt-on acquisitions and strategic alliances, usually with a view to international expansion. Cross-border M&A has been a feature of most of Carlyle's Japan carve-outs. While the emphasis used to be on sales, supply chains are now a key consideration.

"We may take businesses where most of the manufacturing is done in Japan and establish factories and distribution overseas. These days, we must think carefully about supply chain stability and where key components come from," Yamada said.

M&A has served KKR well in the past. The firm's JPY 165bn purchase of PHC Holdings Corporation – Panasonic's medical equipment division – in 2014 was followed a year later by the USD 1.15bn bolt-on acquisition of Bayer's diabetes care business. This diversified a Japan-centric revenue base and secured a global leading position in blood glucose monitoring meters and diabetes sensors.

Six more acquisitions were executed through 2020 as PHC's revenue increased threefold. At the same time, the company divested non-core business units and introduced new management systems and compensation structures. It listed in October 2021 with a market capitalisation of JPY 397bn.

The Calsonic Kansei-Magneti Marelli tie-up was driven by a similar desire for diversification. Nissan was by some distance the former's main customer, accounting for 80% of transactions, while one-third of the latter's revenue came from Fiat Chrysler Automobiles. It also doubled EBITDA at a stroke.

However, a month after the deal was announced in October 2018, Ghosn was arrested in Japan on charges of under-reporting his salary and gross misuse of company assets and dismissed as chairman of Nissan. The company, beset by internal strife, took more than a year to appoint a replacement, which contributed to delayed product launches, reduced output, and loss of market share.

In March 2020, with COVID-19 rampant, Marelli temporarily shuttered 100 of its 145 factories globally at the same time, crippling EBITDA. Two months later, it obtained JPY 130bn in funding to ride out the downturn, comprising an equity cure from KKR and debt from Japanese banks.

Global light vehicle sales fell from 87.8m units in 2019 to 74.7m units in 2020 and recovered to 78.5m units last year, according to IHS Markit. As of April, it was predicting 80.6m units for 2022. A more fulsome recovery was expected in 2021 but automakers found themselves competing with the computer and consumer electronics industries for a limited number of semiconductor chips.

Supply chain issues at Marelli were compounded by a blockage in the Suez Canal, reduced production volume at Renesas Electronics – which supplies nearly one-third of the automotive industry's microcontroller chips – following a factory fire, and ice storms in Texas that shut down numerous chipmakers.

"Various things turned against Marelli that were unexpected, things that don't happen with most private equity carve-outs," said one industry advisor.

Storm conditions

Marelli took action to reduce fixed costs, but in March it applied for alternative dispute resolution (ADR), an out-of-court mediation used in Japan to impose a standstill on debt payments and allow companies to continue operating while they negotiate with creditors on a restructuring.

"This was an effort to help a genuinely good company receive the resources it needed to see through the bottom of the cycle and reach recovery. The goal is to be a partner to Marelli and to corporate Japan," said a source close to the situation.

An ADR process can only proceed with 100% credit support. Approximately 90% of Marelli's outstanding debt was held by Japanese banks, and the rest was split between lenders from Singapore, Taiwan, and mainland China, the source noted. Some of the overseas players declined to approve the deal.

Consequently, the company moved in July to a court-led rehabilitation, where KKR's bid to be reappointed as sponsor could be challenged by other parties. With a clear majority of lenders in favour of KKR's proposed haircut and its revitalisation plan, the court proceeding was swiftly concluded.

Putting aside the danger of being blindsided by unforeseen events, industry participants observe that automotive can present a challenge to investors, with Bain's Verbeeten noting that there are "systemic risks that make it a bit trickier than other sectors." This feeds into a general aversion to cyclical industries.

"We stay away from cyclical industries like parts of the semiconductor, high-tech, and commodity sectors," said Carlyle's Yamada. "Significant change is happening in many other areas, and business models are evolving rapidly. We are focused on carefully identifying these longer-term changes and trends that will take place over the next 5-10 years and capturing these opportunities."

The fear tied to cyclical exposure is essentially poor timing. Investors might misread or misjudge the cycle, resulting in a holding period that coincides with a protracted contraction. This is especially difficult when a company already has heavy-duty value creation programmes underway and suddenly there is limited capital available.

"If revenue fails to grow or even falls, it becomes difficult to underwrite planned investments or sustain capital-intensive businesses. As distress builds, suppliers may accelerate payments, customers may delay orders, and employees may get skittish," said KPMG's Ford.

"In response, operational flexibility is essential, but in certain situations companies may lack this flexibility due to the combination of high-cost structures, lack of labour scalability, and the implications of high debt service obligations."

Unknowns around cyclicality are also the caveat weighing on the investment timeline illustrated by Chiba of Longreach. He recommends focusing on certain operational levers that can be controlled irrespective of broader market conditions – such as cost reductions – to counterbalance risks presented by cyclicality and building cross-border platforms.

In addition, external headwinds can disrupt meticulous and incremental progress towards another key objective of corporate carve-outs: facilitating a shift in management mindset and an acceptance of the merits of private equity-driven operational initiatives.

Yamada explained that Carlyle is deliberately patient in its approach, recognising that the cumulative benefits of other efforts – from bolt-on acquisitions to systems upgrades – might fall short if those tasked with execution don't embrace the corporate vision. The GP begins with small steps and small successes, which are highlighted internally to demonstrate the contribution to larger change.

"The biggest risk is not being able to align with the company on the change agenda," added Bain's Verbeeten. "If you don't have a plan that resonates, management might say, ‘That sounds interesting, let's discuss it internally,' which means ‘We will see what we can do with it and continue with business as usual.' The result might be no action or only a mediocre attempt at your ambitious plans."

Rich pickings

Despite its difficulties with Marelli, KKR remains an active player in the carve-out space. In April, it launched a tender offer for Hitachi Transport Systems at a valuation of approximately JPY 749.5bn after agreeing to acquire parent company Hitachi's controlling stake in the business. As part of the deal, Hitachi will be awarded 10% of the acquisition vehicle.

This would be KKR's third carve-out from Hitachi in the space of five years. All three rank in the top 20 Japan private equity buyouts on record. Six of the top seven are carve-outs, with Hitachi Transport Systems set to occupy third place behind Hitachi Metals, which is also pending completion.

Hitachi is unusual in that it embarked on a systemic divestment programme, pledging to reduce its number of group companies from 800 to 500 by 2022. Attention is now shifting to what the conglomerate might buy as it continues its strategic repositioning, but the likes of Fujitsu, Mitsubishi, and Seven & I Holdings are all tipped as potentially active sellers.

Meanwhile, the opportunity set is broadening. "A wide variety of assets are becoming available in terms of size and industry," said Ochi of Partners Group. "Corporates in Japan have been over-diversified for a long time, but now they realise the importance of portfolio adjustment and optimising their portfolios to achieve long-term growth."

This view is echoed by Longreach's Chiba, who has been tracking a shift in his deal pipeline towards consumer and services businesses. "The market was opened by industrial conglomerates that were under the most financial pressure to get these deals done. Now we see more deal flow from consumer and services companies that may have plenty of cash but are shedding assets for strategic reasons," he said.

In addition, it might be argued that macroeconomic conditions are highly conducive to buyouts by GPs with offshore funds. The yen has depreciated significantly against the US dollar, from JPY 115 in March to JPY 138 as of late August, making Japanese assets relatively cheaper. Meanwhile, inflation remains benign compared to other markets and deal financing remains available on attractive terms.

"Despite various macro geopolitical and economic uncertainties, we still have significant and growing capital held by private equity firms looking to do deals in Japan, and a large industrial sector here that offers rich opportunities for strategic and operational renewal," said KPMG's Ford.

"With the continued acceptance and awareness of private equity as a viable exit candidate, the weak yen, low interest rates and a good financing environment relative to other markets, we can reasonably expect strong deal activity in the near term."

More on North Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.