Emerging Asia start-ups: Governance revisited

Even a modest cooling off from tech investment euphoria experienced in the peak of the pandemic could reveal big cracks in Asian start-up markets. Diligence efforts are ramping up, but is it enough?

In April, Sequoia Capital India aired some dirty laundry with a blog post condemning instances of "wilful misconduct" and "fraud" in its South and Southeast Asia portfolio. From varying perspectives, it was a symptom of familiar venture market undulations and a harbinger of industrywide governance exposures to come.

"It is easy to think of this issue as ascribed to poor due diligence," Sequoia said. "But let's remember that when investments are made at seed or early stage there is hardly a business to diligence. Even later stage investors can face negative surprises, post investment, if there is willful fraud and intent."

Still, it is considered likely that Sequoia did not supervise financial audits of the investees in question post-investment, instead leaving it to the companies themselves to engage auditors. It is also considered likely that many other investors backed these companies on the back of Sequoia's endorsement and assumed due diligence. AVCJ reached out to Sequoia for comment but had received no reply at time of publication.

The episode opens a spectrum of issues, from granular portfolio monitoring practices to understanding the psychology of founders, to the painfully won wisdom that the approval of a brand-name investor is not a bulletproof business validation. Much of the industry considered it a wake-up call about floundering due diligence standards during a period of intense investment.

LPs took to the phones, seeking clarity from managers in the region as to how much time they spent on governance and due diligence. Performance numbers were not on the agenda. Indeed, many of the start-ups under fire are considered category winners, among them Zilingo, a fashion social commerce player active across Southeast Asia that raised USD 226m in 2019 at a valuation of USD 970m.

Shailendra Singh, a managing director at Sequoia, recently stood down from the board of Zilingo after questions were raised about the company's accounting practices. The board launched an investigation and suspended CEO Ankiti Bose, who denies any wrongdoing.

"There is a preference to move faster and messier than slower and more accurately. And it's not easy to be accurate every month when things are changing so fast with new are opening up, especially in a business like that where there's a lot of cross-border customers of different sizes," said a former investor in Zilingo.

"What happened there is not uncommon, except how it became public. Sequoia has the most to lose from what I can tell. It seems like a personal issue between a couple of people, which is very unfortunate."

Fanned by FOMO

From a high altitude, the tides of the VC market are heaving predictably. The strong confidence in tech businesses brought about by COVID-19 created momentum in deployment, increasing competition, driving up valuations, and eroding discipline in due diligence.

The risk of not investing had to be weighed against the risk of flying relatively blind; some VC firms are said to have spent as little as one week assessing companies before investment during this period. Many absorbed more risk than they intended, and it will only be a matter of time before these lapses are revealed.

This is playing out as part of a correction rather than a downturn per se. The heady investment activity of the early pandemic is levelling off but sentiment remains relatively bullish.

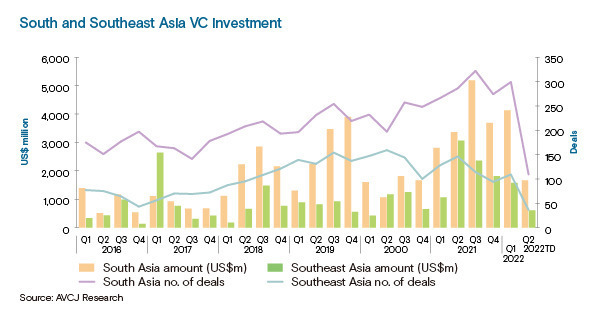

In South Asia, the climax came in the third quarter of 2021, when total VC investment hit USD 5.2bn, according to AVCJ Research. Southeast Asia peaked three months earlier with USD 3.1bn deployed. These figures were USD 4.1bn and USD 1.6bn, respectively, in the first quarter of 2022 and on track to be similarly robust in the three months to June.

"I don't often encounter sophisticated established GPs cutting major corners in due diligence, whether it's a good or bad market, even if they're under pressure to be quicker and accept greater risk," said Andrew Thompson, KPMG's head of private equity for Asia, observing increasing scepticism around high cash burn tech businesses.

"The core GP base will continue doing what they always do as an overheated market normalises, but because there's less competition, they'll be under less pressure and it might feel like a downturn."

There is reason to believe that the phenomenon, although global, will play out more acutely in developing Asia due to inherent governance challenges. One of the biggest obstacles in this vein is the difficulty of securing necessary business approvals in many South and Southeast Asian markets without potentially problematic political connections.

Patrick Yeo, PwC Singapore's Venture Hub leader, notes that reasonable standards of technical and commercial due diligence in developing Asia are well established, but the region suffers from a lack of resources for financial checks. Along with a generally lower capacity to bear diligence costs, this has contributed to a pronounced tendency to assume the lead investor in a round has done its homework.

At the same time, there is the notion that accounting standards have not been built for the digital ecosystem. This makes companies harder to value, especially in developing markets where comparisons to global companies are harder to justify.

Warning signs

The most pervasive outcomes of these pressures are inflated revenue and a deceptive emphasis on vanity metrics. The severity of the risk depends on the category. Gaming and education platforms are less susceptible because payments are generally made transparently through gateways. E-commerce and social media, which tend to overstate user traffic, are some of the most egregious offenders.

Another factor is that many start-ups have failed to plan for a more difficult capital raising environment post-pandemic. As their runway shortens, desperation sets in, and creative – even fraudulent – accounting makes its way into the pitch.

Yeo said investors have responded with more focused due diligence efforts in recent months; some have begun to insist companies file an external financial audit as part of their ongoing reporting requirements. Other emerging areas of concern include hoopla around corporate partnerships with little substance, boards controlled by related parties, and founders paying themselves excessive salaries.

"It's no longer the case that if you show a large growth trajectory, they're going to back you," Yeo said. "Investors are looking at when are you turning profitable, your governance structure, and how you grow. We are still seeing huge inflows of funds in the VC space in Asia. The issue is that investors are becoming more sophisticated."

Soft clues about the mindset of founders must not be overlooked in this process, especially where there has been a significant dilution of ownership. After several funding rounds, founder-CEOs left with only scant remaining ownership positions in their companies face psychological barriers around letting go of decision-making and control of day-to-day activities.

To some extent, this is an age issue. Technology start-up founders are typically in their 20s and 30s and lack experience in terms of building companies for resilience across cycles and shocks. They are driven by value and see value as coming from sales. In developing Asia, they are often from rural areas, lacking familiarity with the protocols of venture capital.

"We've done due diligence on a lot of different tech businesses in the past couple of years, and we've seen that the good ones are the ones where there is transparency and the maturity to know it's not a one-man show," Dhruv Phophalia, an India-based managing director at Alvarez & Marsal focused on disputes and investigations.

"If you're looking to scale up quickly, you have to have the right mindset, the right people on the team, and the experience. And that's not necessarily about being older."

This view helps clarify the idea that exposure of governance shortcomings in the post-pandemic deceleration is not merely a matter of recommitting to financial due diligence – it's about culture and education. Even as late as Series B, board meetings can be informal, ad hoc affairs in developing Asia. Effective mentorship is most often cited as the key missing ingredient.

Stepping up

VCs are generally not equipped to offer more than high-level guidance to start-ups, which leaves them uninvolved in day-to-day accounting, team building, and communications activities. One potential fix is the concept of the external advisor, an ostensibly neutral third-party coach and sounding board on ground-level operations and cultural matters.

In lieu of intense mentoring resources, these issues can be handled by identifying and resolving – or avoiding – them pre-investment. Vikram Utamsingh, Alvarez & Marsal's country leader for India, points to his predominantly private equity client base as an example of how reputation checks around matters such as team morale and counterparty relations can translate into fewer governance problems down the track.

"Because the big global funds have been here for 15-20 years, they understand that even if they own 90% of a company in this market, they're dependent on individual promoters to drive growth and get their returns," Utamsingh said.

"That's why they're so conservative about the type of person they'll team up with. They're not necessarily walking away because of fraud or misconduct – it could be as simple as how they treat employees."

There is evidence that best practices pursued by these global players around due diligence and governance support are filtering through the local ecosystem to early and growth-stage investors. India's Iron Pillar Capital is a case in point.

The firm typically hires the CFOs and COOs for its portfolio companies. Every company is audited annually by one of the big four accounting firms, and there is a 30-member value-add unit that advises in part on governance. There are seven partners currently responsible for 12 portfolio companies. The idea is that no one partner should cover more than five.

"There's nothing that can trump individual partners having the time to give the founder their ear," said Anand Prasanna, a managing partner at Iron Pillar whose experience includes a stint at Sequoia in the early 2000s. "VC is a business that takes time, and if you try to flip that around and manage so many companies with limited time, that model is going to break down."

This philosophy was not particularly popular during the pandemic investment boom. Iron Pillar, which invests from the Series B to D stages, doesn't like to pay more than single-digit EBITDA multiples and has received significant pushback from emboldened founders in recent months. There were only four deals last year, three of them at single-digit multiples. No investments were made in the first quarter of 2022.

It helps illustrate a difficult reality for investors planning to buckle down on due diligence, governance, and valuations in the current environment.

Coming correction?

Ostensibly, the froth in Asia's post-pandemic investment market is subsiding as air comes out of the US tech bubble. "Investor sentiment in Silicon Valley is the most negative since the dot-com crash," David Sacks, a VC investor and founding COO of PayPal, said last week. Meanwhile, the conflict in Ukraine has offered a nail in the macro coffin, exacerbating long-festering uncertainties around East-West decoupling and supply chain-related economic risks.

The slowdown is still largely theoretical, however. VC confidence remains robust in developing Asia, even in unproven business models. Public markets have not corrected for the shift in mood, and this isn't expected to happen for another six to nine months. Many start-ups are still focused on maximising valuation rather than optimising quality of capital.

India is perhaps the poster child. Iron Pillar estimates about 100 tech unicorns have been created in the country since January 2020, and there will be 250 by 2025. There is a significant amount of pride in this development, and it is rightly flagged as a benchmark of overall ecosystem maturity and growth.

But the Indian unicorn count is also a kind of vanity metric all its own – a difficult to substantiate statistic doubtlessly inflated by dubious claims and overzealous investment. Many companies are justifiable members of the club, but many are not, and that is a ratio that has not been clarified.

For Prasanna, the depth of an ecosystem can be more accurately measured in the number of companies that have crossed into USD 100m of revenue and how many are about to achieve profitability. These figures are increasing in developing Asia, but they are still not being factored into valuations.

"Investors are saying, ‘What is the valuation you want to raise in 18 months? I will give you that valuation today.' That kind of conversation is actually happening," Prasanna said.

"You're literally putting the founder on a treadmill and accelerating the treadmill, and that is going to crack at some point. Some people are going to figure out they can't deliver those metrics and see how they can bend the rules. Investors who invest in companies at unrealistic valuations are fully to blame for what happens in this ecosystem in governance because they're pushing people to bend rules."

More on South Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.