1Q analysis: Monetising managers

Baring Asia and PAG underline the value of their management entities; exits slump amid uncertainty; BGH Capital, renminbi GPs shore up fundraising; investment fails to extend the late 2021 flourish

1) GPs: The BPEA, PAG show

Liquidity events involving private equity firms themselves rather than investee companies were responsible for the defining moments of the first quarter of 2022.

The global "fund of firms" that accumulate interests in GPs have made little impression on Asia: Affiliated Managers Group (AMG) bought 15% of Baring Private Equity Asia (BPEA) in 2016 and The Blackstone Group picked up 19.99% of PAG in 2018. Few managers in the region meet all these investors' requirements in terms of track record, fee-generating scale, and business line diversity.

In January, a third transaction was added to the list, as Blue Owl-owned Dyal Capital Partners acquired a 12% interest in MBK Partners. Two months later, BPEA announced it would merge with EQT and PAG filed for an IPO in Hong Kong. Having enabled the private equity firms to monetise their management companies, AMG and Blackstone are now on the cusp of monetisation.

These actions tap into a wider phenomenon in global alternatives, as the shares in the incumbent listed managers hit record highs towards the end of 2021 and others looked to join them on the public markets. TPG and Blue Owl account for the largest listings in the past 12 months; CVC Capital Partners is among the names touted for future offerings.

BPEA is said to have explored an IPO before agreeing to plug itself into EQT, a manager that has been on an expansion drive ever since its 2019 offering. EQT has demonstrated a willingness to buy its way into other markets, and it lacked an Asian PE offering that could match Europe in size and ambition.

EQT is acquiring 100% of BPEA's management company and entities that control its funds – plus a share of carried interest – for EUR 6.8bn (USD 7.5bn). BPEA will get EUR 5.3bn in stock and EUR 1.5bn in cash. The valuation has grown sixfold since AMG's investment. Over the same period, BPEA's fee-paying assets, across private equity, real estate, and credit, have risen by 5x to USD 17.7bn.

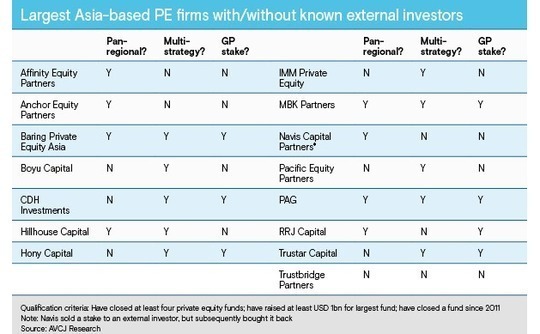

BPEA and PAG – with USD 29.6bn in fee-paying assets in private equity, credit, and real estate – remain rare creatures among Asia's independent managers.

AVCJ identified 15 active GPs that have closed at least four PE funds, including at least one in the past decade, and raised USD 1bn or more for their largest fund – a very rough attempt to filter out the small and short-lived. Of this select group, only four could claim to be both pan-regional and multi-strategy: BPEA, PAG, MBK, and Hillhouse Group.

2) Exits: Momentum misplaced

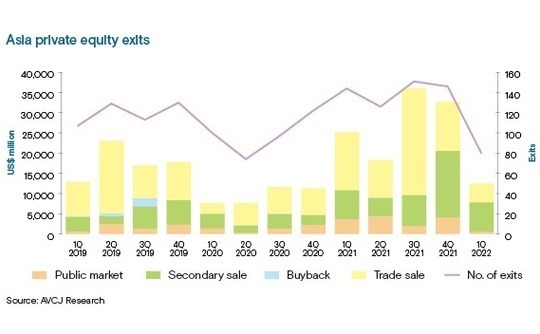

Private equity exits in Asia appeared to have regained momentum by the end of 2021. Aggregate proceeds in the second half of the year were 50% higher than in the first six months and 100% higher than the six months before that. Based on AVCJ Research's provisional data for the first quarter of 2022, it was a false dawn. Exits totalled USD 12.5bn, down from USD 32.7bn in the previous quarter.

Sales to other financial sponsors, which reached record levels in the latter part of 2021, fell by nearly half; trade sales plummeted by more than half, and public market sales dried up. Investors – financial and strategic, buy-side and sell-side – have become wary. Debt providers too. Pick any number of contributing factors: jitters over Ukraine, macroeconomic uncertainty, volatile equities markets.

Greencross and La Trobe were two of five Australia and New Zealand representatives in the top 20. India and South Korea accounted for six and four, respectively. There was only one mainland China deal and it ranked 20th on approximately USD 150m.

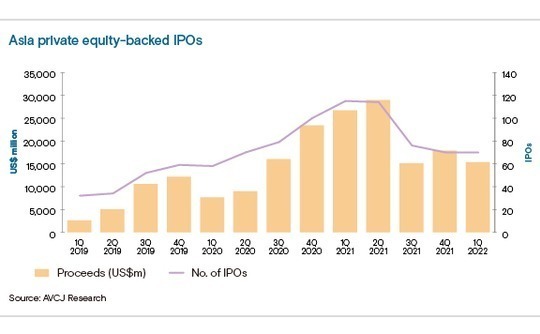

Private equity-backed IPOs held relatively steady, USD 15.4bn versus USD 17.8bn in the previous quarter, with China leading the way. Offerings on mainland exchanges were responsible for 90% of the regional proceeds – a statistic enabled by relatively inactivity on other bourses in Asia and the continued absence of Chinese companies from the New York Stock Exchange and NASDAQ.

Of the 20 largest listings by companies with financial sponsors, all but two took place on Shanghai's Science & Technology Innovation Board – or Star Market – and Chinext. For the Star Market, it was a notable return to form. The USD 7.8bn raised from 21 offerings represented a new quarterly high for the young bourse. Jinko Solar and ASR Microelectronics led the way with USD 1bn-plus IPOs.

Meanwhile, the trickle of Asia-based M&A activity involving US-listed special purpose acquisition companies (SPACs) continued, facilitating liquidity events for early investors. Singapore's PropertyGuru and Taiwan's Gogoro both began post-merger trading, while China-based artificial intelligence software developer Perfect Corp agreed a USD 1bn tie-up.

3) Fundraising: The many and the few

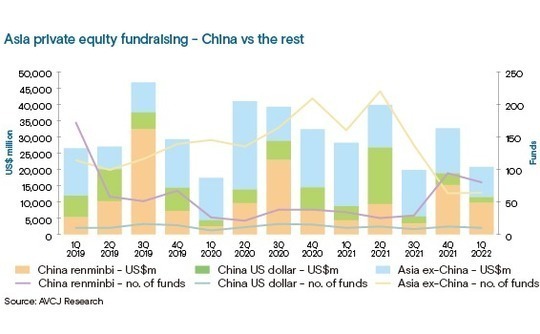

BGH Capital captured the contrasting fortunes in private equity fundraising by closing its second vehicle in March after less than six months in the market. The manager secured AUD 3.6bn (USD 2.6bn), which represents the largest-ever private equity fund focused on Australia and New Zealand.

Only 18 funds region-wide completed partial or final closes on USD 300m in the first quarter of 2022. Seven crossed the USD 700m threshold and BGH was one of three to surpass USD 1bn. Total commitments came to USD 20.7bn, compared to USD 32.7bn and USD 20.8bn in the two preceding quarters. Fundraising is consistent in its inconsistency.

In the nine quarters since the outbreak of COVID-19, the average capital raised is USD 30.1bn, down from USD 36.2bn in the nine quarters before that. The sharp swings reflect the presence of large-cap managers – plenty are currently in the market or preparing to enter it, they just aren't closing funds – and trends in the renminbi-denominated fund space, which lives by its own rules.

Of the 20 largest closes in the first quarter, 13 were by China-focused managers and nine involved renminbi funds. The local currency contingent occupied half of the first eight spots.

Renminbi fundraising has moved in the opposite direction, rising from USD 3.3bn in the third quarter of 2021 to USD 15.2bn in the fourth, and then USD 9.7bn in the first three months of 2022. In each of the past two quarters, renminbi activity has accounted for nearly half the regional total. The 50% mark has been exceeded twice in the last three years, but it was followed by dips below 25%.

Renminbi funds that achieved closes in January-March were not dominated by government-controlled sponsors. Numerous independent managers also feature. It could be indicative of the internalisation of China's markets, with local currency funds seeking local market exits. Equally, the renminbi share could collapse next quarter.

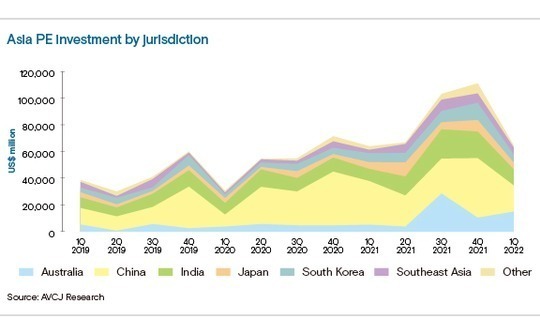

4) Investment: Downward adjustment

From a record high of USD 111.2bn in the final quarter of 2021, private equity investment in Asia slipped to USD 64.7bn in the first quarter of 2022. Though still a sizeable total – bettered only four times to date – it confirms anecdotal accounts of a weakening in investor sentiment.

The drop-off in venture capital activity was relatively mild; growth equity and buyouts were the weak spots. This was felt most keenly in China, where overall investment slipped from USD 44.7bn to USD 19.5bn, the lowest quarterly showing since the kneejerk response to COVID-19 in the first three months of 2020. Early and growth-stage technology investment is not to blame.

Deployment in the sector collapsed in the second quarter of 2021 as the government's assorted regulatory actions began to bite. It then stabilised and crept back up, reaching USD 10.9bn in the fourth quarter, although behind the numbers, investors were busily refocusing from consumer-facing to business-facing deals. In the first quarter of 2022, the total was once again USD 10.9bn.

Rather, the drop-off was in electronics and healthcare, which had risen high on the back of robotics and industrial value-add and biotech and pharma services. Electronics fell from USD 11.8bn in the final quarter of 2021 to USD 823m in the first three months of 2022; healthcare slumped from USD 6bn to USD 2.9bn, a level not seen since early 2020.

India, which gained prominence as a technology investment destination as China declined, was unable to maintain its frenetic pace. Unicorns are still being created and established industry giants like Byju's and Swiggy continue to close sizeable rounds, just with less intensity. Early and late-stage tech investment came to USD 8.1bn in the first quarter, down from USD 9.1bn.

Much as the transaction might demonstrate private equity appetite for gaming-related assets, Crown needs a facelift after a string of scandals and setbacks. The company has been investigated for possible breaches of anti-money laundering rules over its ties to Chinese junket operators, had its licences suspended or reviewed by state governments, and settled a class-action lawsuit.

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.