Private equity & credit: Seeking synergies

GPs are placing greater emphasis on Asia private debt strategies to capture deals that don’t work as private equity. Much can be achieved by pooling ideas and resources, but collaboration isn’t as straightforward as it seems

CDIB Capital has spent the best part of a decade introducing new strategies. Established as the private equity arm of Taiwan's China Development Financial (CDF) in 2006, it shifted from balance sheet investor to third-party fund manager in 2015 with the close of a debut growth vehicle. Since then, the firm has bolstered its legacy venture capital business, and formed special situations and buyout teams. The latest addition is structured credit.

"We always looked at credit as a natural way to expand our footprint into complementary strategies that would allow us to improve the quality of earnings by generating contractual returns as opposed to lumpier returns you get in private equity," says Lionel de Saint-Exupéry, president and co-CEO of CDIB. "Some companies need capital, but they want it to be non-dilutive. We can be that bridge between senior debt and equity that helps them accelerate growth."

The middle-market PE firm brought in a three-person team from The Carlyle Group and committed $150 million to seed a portfolio. It is positioning to tap third-party investors for a private credit fund.

The potential synergies go beyond integrating the private equity and credit teams and encouraging them to share ideas. CDF owns KGI Bank, KGI Securities firm, and Taiwan-based China Life Insurance. Three credit deals have closed so far. The bank provided a currency hedge for the first and came into the second as a senior lender alongside the securities firm.

"We are doing a good job of unleashing some synergies, but there's more to be had," says Tor Trivers, CDIB's head of structured credit. "Now that KGI Securities has participated in one deal with us, I think we will get synergies in origination as well. And should we want to do a securitization for one of our borrowers, the securities firm can help us to move that product. The life insurer potentially could even be a purchaser of those securities."

Ambition to scale

CDIB's move into private debt comes as more global private equity firms look to roll out the strategy in Asia, with a few of the larger pan-regional GPs joining in as well. Announcements are usually accompanied by a familiar narrative about not being able to take advantage of all the investment opportunities they see because target companies are reluctant to take equity funding.

The reality is somewhat different. While there are examples of private equity and credit teams looking at the same deal flow and deciding which strategy is the best fit, this behavior is not necessarily widespread. A dearth of relevant talent in Asia means getting private debt programs off the ground isn't easy. Those that manage it might find that compliance protocols limit cross-asset-class exchanges to broad industry knowledge-sharing rather than granular pipeline detail.

"At this moment we don't have a lot of synergies between our private equity and private debt businesses," says a representative of a large multi-asset manager, having declined to be interviewed for this story. This wasn't the only knockback.

No one contests the fundamental appeal of private debt in Asia. The region accounts for one-third of global GDP, two-thirds of global growth, and it is the world's largest credit market. Banks are responsible for 80% of credit, compared to 35% in the US and 55% in Europe, yet there is ample demand for alternative solutions – from borrowers that either cannot obtain financing through traditional channels or want something more customized than banks are willing to provide.

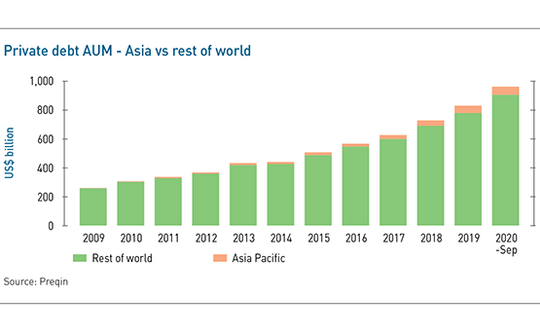

Ten years ago, Asia's share of global private debt AUM was negligible. Since then, AUM has grown nearly fourfold, reaching $973 billion as of September 2020, according to Preqin. The Asia share is 6%. Special situations and mezzanine are the two largest segments, followed by direct lending.

It is suggested that Trivers and his team moved from Carlyle to CDIB partly because their strategy within private debt – non-competitive situations, checks of $20-50 million, and preference for lending against other financial assets – wasn't scalable enough.

"Five years ago, there was a big effort to grow the credit business and focus on opportunities where we can achieve scale. Our credit AUM more than doubled over this five-year period to $56 billion. There is a target to grow it to more than $80 billion by 2024," says Ming-Hau Lee, a managing director in Carlyle's Asia credit team. "We have exposure to Asian or Asian-linked assets through our global funds. My role is to build out our credit business in a much more focused way. We are interested in Asia's trillion-dollar economies – primarily China, Australia and Korea."

Carlyle joins global private equity peers such as Bain Capital, KKR, and The Blackstone Group in targeting the broad Asia private debt and special situations space. Participating Asia-based large-cap GPs include PAG, Baring Private Equity Asia, and MBK Partners, though their remits vary.

KKR was among the earliest entrants, having identified Asia as an expansion priority in 2017. The firm's journey into the credit space in North America began 13 years earlier after losing out on an energy deal to Warren Buffett. KKR was familiar with the target company and invited to participate in the transaction, but it ended up passing on the opportunity because it wouldn't work as private equity. Berkshire Hathaway profited handsomely.

Joining the dots

KKR launched its credit business in 2004. Initially focusing on leveraged loans and liquid credit, it entered alternative credit in 2009. Asia benefits from the same kind of network effect as the global operation. The private equity team, third-party advisors, and organic origination each account for about one-third of deal flow.

"We are in the midst of a huge amount of commercial activity and much of it isn't private equity-related; we want to surround our core country teams with a product suite that is relevant to the market," says Brian Dillard, head of Asia credit at KKR. "Having the ability to approach a company about a buyout or a minority investment and then flip the script based on what they are trying to accomplish, that is a very natural thing for KKR. We have many different pools of capital."

The script was flipped in 2019, for example, when KKR was one of several PE firms approached by the family owner of listed Singapore waste management business 800 Super about supporting a take-private. On closer inspection, the GP concluded that structured mezzanine financing would be more cost-efficient, and the family agreed. KKR claims to be the only private equity firm that delivered a debt proposition.

With Transaction Services Group (TSG), an Australia-headquartered payments software provider, the deal went in the other direction. KKR was outbid by Advent International, so the private debt team took the diligence work conducted on the company and offered to finance the deal for Advent.

Not everyone is sold on the notion of frontline dealmakers generating opportunities that can feed more than one strategy. One counterargument is that private equity investors have a different coverage universe to their credit peers, and they approach situations with a different mindset.

Rahul Kotwal, founder and a managing partner at Zerobridge Partners, an Asia-focused credit investment and advisory firm, notes that the private equity side wants high-growth companies capable of delivering 20%-plus returns and the focus is on upside scenarios and increasing value. Private debt, meanwhile, prioritizes businesses with stable cash flows and ensuring the principal can be reclaimed in downside scenarios.

"There certainly are synergies," he says. "The brand name helps, the ability to raise capital helps, and clearly there is going to be some overlap. But it's not quite as simple as saying they cover companies that need minority capital, so we are going to get massive scale efficiency here."

One of the reasons 800 Super ended up as a private debt deal was because it was deemed unlikely that Singapore's waste management industry, though efficient and boasting attractive competitive dynamics, could deliver private equity-style returns. However, Dillard asserts that the credit team is very much interested in the kind of high-growth businesses that appeal to private equity. In this sense, KKR positions itself as separate to lender-of-last-resort special situations capital.

Alignment between private equity and credit teams is secured along financial and communication lines. KKR shares out carried interest across the firm, so an individual responsible for one strategy would share in some of the success of others, which is intended to encourage collaboration. The silos are further broken down by including credit, infrastructure, and real estate executives at Monday morning meetings alongside their private equity colleagues.

"We have nine credit specialists across the region embedded in country teams. They are present at the pipeline review and hear what is going on in private equity," says Dillard. "When discussing equity ideas, we look at valuations and ask whether there is a way to invest behind a company that would generate a better risk-adjusted return. There is a lot of back and forth between the teams."

Behind the wall?

CDIB is set up in a similar way. The investment teams sit together, participate in some of the same calls, and regularly make referrals. A recent opportunity emerged via an advisor who pitched a pre-IPO deal involving an Asia-based company to the team in New York. They decided it was too early for the company to list and growth equity wouldn't suffice. Seeing the company had some receivables – and knowing the structured credit group likes lending against those – New York handed it over.

"It's not so large a firm that we are all siloed. We are familiar with day-to-day goings-on of the equities side and we have meetings where everyone explains what they are doing," says Trivers. "We don't have Chinese walls in place between debt and equity because it's not warranted here."

CDIB would not go so far as to have debt and equity teams participating in the same deal; the conflicts would be too difficult to resolve in the event of a debt restructuring scenario.

Other firms do have ethical walls. At Carlyle, for example, the private equity and credit teams sit on the same floor but in separate sections, with key card-accessed doors in between. Cross-strategy internal discussions must be signed off by a member of the compliance department who may sit in on them. The credit team does not participate in the private equity Monday morning meeting.

This doesn't mean exchanges are without value. Referrals can be made through proper channels; a wealth of industry-level information, produced by different strategy teams, is shared throughout the firm; and the credit team can access the historical log of Carlyle private equity deals, which helps in terms of mapping out the borrower universe, conducting channel checks, and knowing who to ask for an introduction. Members of different teams can socialize; they just know where the lines are.

All large multi-strategy PE firms have compliance protocols designed to facilitate knowledge-sharing while ensuring that commercially sensitive information is ringfenced. "You wouldn't want a certain borrower to know that private equity has access to the same information as you, the financier, because that is a potential competitor down the line," observes one global credit executive.

However, there are nuances in approaches to Asia where the credit landscape is very different. Collateral lending obligations (CLOs), which often feature leveraged loans taken out by other PE firms, are non-existent. Lending to financial sponsor-backed companies is also relatively limited. When it comes to compliance, some GPs apply a uniform set of global rules. Carlyle is among them. Others give private equity and credit more scope to work together where they see little conflict risk.

It might be argued that the prevalence of family-led over sponsor-led counterparties in Asia lends itself to coordination between private equity and credit. Minority equity investments are commonplace, yet family owners – many of them first-generation owners – can be loath to dilute their holdings. Given a choice between expensive debt and equity, a sponsor-led company would likely do the math and take the latter. Families often opt for the former, seeing it as a short-term fix.

"Sponsor-led deals in the US tend to be more transactional, they come down to pricing and terms," says Lee of Carlyle. "In Asia, dealing with family counterparties, relationships are very important. If the private equity group knows a family well or has previously invested in one of their companies, it's easier to pick up that relationship and offer customized credit solutions. Often, they don't differentiate between private equity and credit groups. To them, it's one Carlyle."

These counterparties aren't necessarily small. Certain Asian economies are dominated by sprawling business conglomerates – often family-owned – that operate across dozens of verticals. Their capital needs vary by time, place, and structure. Meanwhile, the region's relatively small bond markets are not always an option. KKR's Dillard struggles to come up with meaningful analogs in the US or Europe, simply describing Asia as a fundamentally different setup.

The line between debt and equity is often blurred, with numerous accounts of deals switching back and forth, depending on counterparty appetite and market conditions. Intermediate Capital Group (ICG) routinely provides a combination of the two and sees this as a competitive edge over private equity firms that would be reluctant to allow parallel strategies do the same.

"Most of the deals we look at traditional credit funds wouldn't be able to do," says Wooseok Jun, head of Asia Pacific at ICG. "If anything, the ones we come across are private equity funds."

Going local

These dynamics underscore the importance of having a presence across multiple jurisdictions to build relationships with borrowers and navigate the cultural, legal, and linguistic differences that underpin Asia's lack of homogeneity. Global private equity firms are advantaged in this respect because they can leverage existing platforms when taking credit coverage into new geographies.

The key roadblock is finding people to execute this strategy. Independent platforms are logical places to go shopping for talent and several managers say their country heads have been approached by global firms looking to expand into credit. One recalls being contacted by a head-hunter looking for tips on who to hire because he had been tasked with replicating this manager's team. Recruitment challenges serve as a reminder that Asia's credit space is still relatively young.

"There are firms that see their global peers replicate success in private equity in other asset classes and they think about doing the same," says Zerobridge's Kotwal. "But there is a dearth of talent here and experienced people who can do that. The skillets of the private equity firms out here are quite different in terms of how you originate deals, how you structure deals."

KKR's most active markets to date have been Southeast Asia and Australia, which together account for three-quarters of capital deployed. India comes next, followed by China, Korea, and Japan. Offering local currency solutions in India and China necessitates a local presence and various licenses. While the firm has built out a substantial footprint in India, it hasn't been as prolific in China. This is partly due to personnel.

"We have a large private equity business there, so we see a lot of opportunities, but we haven't done a lot of China credit historically and we won't until we find the right person to lead that business," says Dillard. "China is a 2021 priority, laying the groundwork there. It will take time to make it a larger part of the business."

More on GPs

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.