India middle-market: Looking for positives

Private equity activity is gradually resuming as India’s economy emerges from lockdown, but investors are wary of paying too much for assets or putting their money behind unsustainable trends

The global bicycle shortage – spurred by an aversion to public transport, gym closures, and an increased focus on healthy living – has come to India. Sales rose 25% year-on-year in June as the lockdown was lifted, according to the All India Cycle Manufacturers’ Association. With multiple reports of individual retailers running low on stock, the association has warned of a growing supply-demand gap.

Bicycles are one of numerous beneficiaries of changing habits in response to COVID-19. “There has also been an upsurge in demand for sports and fitness ,” says Gopal Jain, a co-founder and managing partner of Gaja Capital. The firm has seen this in its own portfolio through SportzVillage, a sports program manager for schools.

For an emerging trend to become a meaningful investment thesis, it must pass the long-term sustainability test. But COVID-19-proof business models already loom large as India’s private equity industry looks for seams of growth in a challenging environment.

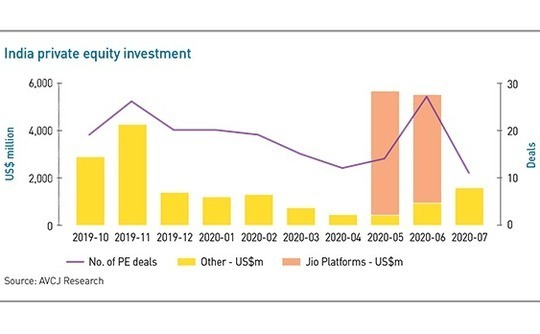

Having ended 2019 on a high, with a record $8.5 billion deployed during the final quarter, the pandemic exacerbated a lackluster start to the new year. PE investment – VC is excluded – slipped from $1.3 billion in February to $736 million in March and $450 million in April. While May and June saw a remarkable turnaround, if Jio Platforms is removed from consideration, the totals of $5.6 billion and $5.5 billion become a more modest $417 million and $930 million.

Most industry participants regard the Jio effect – Reliance Industries’ bid for dominance across mobile internet services, e-commerce, broadband and cable – as exceptional. “Jio is a one-off in my view,” says Nitish Poddar, partner and national head of private equity, KPMG India. “It is all about the ability of Mukesh Ambani to create a Tencent of India, that’s what people are betting on.”

Reengagement point

Nevertheless, Poddar claims that general private equity activity in India remains relatively robust, even as M&A has slowed down. He estimates deal flow is only about 10% down on last year and AVCJ Research’s numbers appear to corroborate this. A total of $1.6 billion was deployed across about a dozen PE transactions in July compared to an average of $1.8 billion and 18 deals for the first eight months of 2019.

“While there’s been a slowdown in some of the larger deals we would traditionally work on, we’re seeing an uptick in hiring within the PE community and for portfolio companies. That’s a positive sign,” says Deepak Bhawnani, CEO of Alea Consulting, a risk mitigation and investigative consulting firm. “There has been a surge in demand for due diligence checks. Previously, GPs relied on their own networks or headhunters doing face-to-face meetings, but those meetings are not happening.”

“A lot of deals fell through in March and April because the economy ground to a halt and investors stepped back,” Jain says. “The opposite is now happening. There are deals that were negotiated in May and June, and given how the economy is recovering, entrepreneurs find them unattractive. There has been a spate of readjustments and deals falling through because the extrapolation from April, May and June is no longer valid going forward.”

He points to a string of indicators as evidence of the recovery: consumption of steel, electricity and petroleum, automobile sales, rail freight volumes, and goods and services tax revenue were all at least 80% of the February level as of last month. Passenger air and rail traffic are still struggling, although a sharp rebound is expected once the pandemic abates.

ANZ offered more guarded optimism in a briefing published last month under the title “India: a painful recovery.” It noted that the battle with COVID-19 is continuing, personal mobility remains subdued, credit growth remains weak, and even the improving indicators are still below pre-COVID-19 levels, suggesting that the return to growth would be protracted.

Concentration effect

At the same time, valuation mismatches are only found in verticals that are growing faster than the overall economy. Even before COVID-19, most local private equity firms concentrated on four sectors. IT services and healthcare retain their appeal, with valuations in the latter continuing to rise; the general feeling on financial services is wait-and-see; and consumer is volatile, with hospitality floundering just as certain consumer goods segments are flourishing.

“Private equity isn’t really looking at areas that have been impacted by COVID-19, so there has been no dramatic change in valuations pre-COVID-19 and post-COVID-19,” says KPMG’s Poddar. “India is famous for mismatches in valuations from a buyer and seller perspective. That has been a regular complaint from financial sponsors for 20 years.”

There is an additional thematic overlay that cuts across sectors: rural rather than urban, online rather than offline, non-discretionary rather than discretionary, and mass-market rather than premium. The challenge for investors is twofold. Are valuations in these more favored areas justified given the persistent macroeconomic uncertainty? And will the emerging trends that underpin these valuations likely to be sustained once India returns to a version of normal?

“You must look for trends that are durable,” says Sanjay Kukreja, a managing partner at ChrysCapital Partners, who observes that India is probably bottom decile in terms of economic outcome, but valuations in many areas are still top decile. “I’m not saying bicycle sales aren’t durable – we could be at an inflection point in terms of fitness. But you have to be careful about what you back. You need tailwinds beyond COVID-19.”

More on South Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.