1Q analysis: Impact winter

As the coronavirus outbreak escalated into a global pandemic, what was a problem for China investors quickly spread into other geographies. Fundraising, investment and exits inevitably took a hit

1) Investment: A staggered slowdown

Four months ago, BGH Capital and Ontario Teachers' Pension Plan (OTPP) were devising strategies to help New Zealand dental clinic operator Abano Healthcare develop its business in Australia. The company had a 17% share of its home market but only 2% across the Tasman. BGH's local operating expertise and OTPP's experience taking US-based Heartland Dental on a similar consolidation-themed journey would remedy a previously challenging expansion effort.

Now the proposed NZ$300 million ($190 million) buyout is in tatters, following government-mandated shutdowns of non-essential dental services in New Zealand and Australia intended to stem the spread of COVID-19. This development triggered the material adverse change (MAC) clause in the investment agreement, and BGH and OTPP pulled out. They may reengage later – perhaps at a lower valuation – but presumably not while the industry and macro outlooks remain so uncertain.

The Abano situation attracted attention because the details were publicly disclosed, but it's by no means an isolated incident. GPs across Asia are said to be evaluating their options in terms of agreed deals and hitting the brakes on new investments. The implications of cutting off out-of-home consumption and curtailing supply chain activity will be widespread and likely drawn out. No investor is comfortable signing off on valuations in the current climate.

This is the context for the wholly predictable drop-off in private equity investment during the opening three months of 2020. According to preliminary data from AVCJ Research, a total of $23.2 billion was deployed, the lowest quarterly total since 2014. It represents 61% decline on the last three months of 2019, which was the second-biggest on record, and a 51% decline on the average for the previous eight quarters.

The pain was felt across almost all strategies – oddly enough, venture capital investment increased on the last quarter – and geographies. Deployment in China plummeted from $30.2 billion to $6.7 billion, a seven-year low. Activity in India and South Korea fell by more than half on the previous three months, while the drop-off in Australia, Japan and Southeast Asia was not so severe thanks to a handful of relatively large-ticket transactions.

There were only three deals of $1 billion or more (compared to 11 in the fourth quarter) and China accounted for just two of the 10 largest transactions (compared to five in the fourth quarter). But all bar one of the eight investments outside of China were announced in January or February, before COVID-19 escalated from a local problem into a regional concern and then into a global pandemic. The staggered response to the crisis is worth examining in more detail.

In December 2019, China's share of PE and VC investment in Asia was 55% and 42%, respectively. These percentages fell to 28% and 23% in January and 19% and 9%. Come March, with new infections under control and people emerging from lockdown, the shares rebounded to 74% and 46%. The number of transactions also picked up from the first two months. Healthcare and online services came to the fore, with Yuanfudao becoming the country's most valuable online education start-up following a $1 billion round.

The swing was accentuated by activity in other markets fizzling out. Private equity investors put $592 million to work outside of China in March; the January total for Korea alone was $468 million.

It remains to be seen whether the China resurgence was driven by transactions that GPs essentially closed before COVID-19 took hold but held back from announcing until the curve started to flatten. If so, investment might decline over the coming months as managers catch up on new deal due diligence that couldn't be conducted under lockdown. Outside of China, there is less conjecture: the second quarter is likely to look even worse than the first.

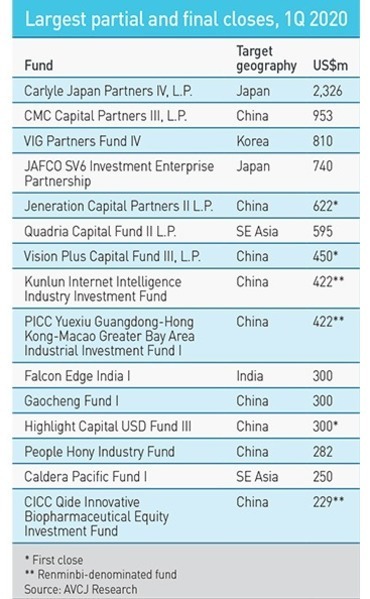

2) Fundraising: Fall back on the familiar

There are only two developments – one actual, the other possible – that might prevent Asia private equity fundraising from delivering a bleaker set of numbers in the second quarter than in the first quarter. First, CVC Capital Partners announcing a final close on its fifth pan-regional fund at the beginning of April means that there is already $4.5 billon in the kitty. Second, another of the larger managers currently in the market could reach a meaningful first close.

The scorecard for January-March already makes for dismal reading: $9.7 billion raised across 65 partial or final closes, down from $23.8 billion from more than 180 closes in the final three months of 2019. In US dollar terms, the first quarter represents the worst showing since 2013; as for the number of closes, one must go all the way back to 2004 to find a deeper trough.

China fundraising slipped from $11.8 billion in the final quarter of 2019 – a low total by recent historical standards – to $3.4 billion in the first three months of 2020. The split between US dollar and renminbi-denominated funds was close to even. However, the fall in fundraising tracked the spread of coronavirus, eventually spreading throughout Asia.

HighLight Capital, a specialist Chinese healthcare GP, announced a first close of $300 million on its latest US dollar fund in February, having spent just three months in the market. However, having set a target of $400-450 million, the firm is not expecting a final close until the autumn. Existing LPs were probably well-represented in the first close. Going forward, the emphasis swings towards new investors and due diligence requirements are generally higher than for re-ups. Travel restrictions will prevent these LPs from conducting any on-site assessments.

This theme looks set to endure until the crisis abates, although it will not impact all managers equally. There are numerous examples of private equity firms postponing fund launches, targeting a series of rolling closes with LPs that have already completed some due diligence, and looking to do dry first closes where they don't have to start the IRR clock and are therefore under less pressure over the timing of the final close. And then there are GPs with a strong enough following that they can continue to raise capital almost regardless of the difficult circumstances.

There are still many unknowns surrounding the impact of COVID-19 on private equity. But it would appear a safe bet that the gap between the haves and have nots – fast closers and slow closers, or perhaps fast closers and no closers – will continue to widen.

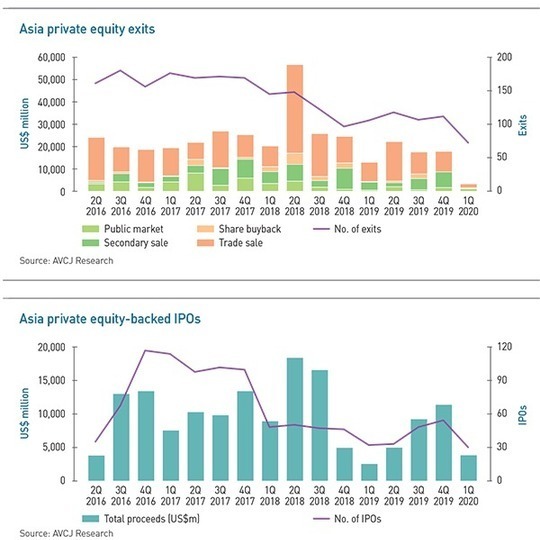

3) Exits: Grinding to a halt

Over the past two years, coinciding with the introduction of regulatory relaxations regarding weighted voting rights and zero-revenue biotech start-ups, Hong Kong has averaged eight private equity-backed IPOs per quarter. There were only two during the first three months of 2020 and one of them listed in the first half of January, before financial sponsors started fretting about wild swings in the Hang Seng Index and limited demand for new names among public markets investors.

InnoCare Pharma found a path through the chaos in March to raise HK$2.24 billion ($288 million), but 12 cornerstone investors – including some existing PE shareholders – covered half the offering. The last of the three Chinese companies that went public in the US was done by mid-February.

While the $3.8 billion in proceeds generated by 31 private equity-backed businesses in the first three months of 2020 represents a sharp drop on the last three months of 2019, it isn't a disgracefully low total by recent standards. For example, $2.6 billion was raised from 32 offerings in the first quarter of 2019 and $4.9 billion from 35 in the quarter after that. Nevertheless, two offerings accounted for half of the regional proceeds, with India's SBI Cards alone contributing more than one third.

Overall private equity exits in Asia came to $3.3 billion for the quarter, down from $17.7 billion in October-December 2019, with the number of announced deals dropping from 111 to 72. Things haven't been this bad since the global financial crisis in 2009 – the last time a serious market shake-up prompted widespread termination or suspension of sale processes by strategic and PE owners.

Trade sales inevitably took a hit, falling from $9.1 billion to $1.8 billion. Four $1 billion-plus deals in the last three months of 2019 became zero in the first three of 2020. KKR was responsible for the largest, having agreed to exit Japanese DJ equipment manufacturer AlphaTheta Corporation to a local strategic investor for JPY35 billion ($324 million).

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.