Portfolio: Capital Square Partners and Aegis/StarTek

Capital Square Partners’ acquisition of Indian business processing outsourcing (BPO) player Aegis ultimately helped two different companies find global relevance after a turbulent and disruptive decade

Three years ago, Sanjay Chakrabarty a managing director at Capital Square Partners, was considering ways to restore Indian business process outsourcing (BPO) player Aegis to its former glory. He opted for a reverse merger with a US-listed company – a tricky move, but one that appears to have paid off.

At the start of the previous decade, Aegis – then a division of domestic oil-to-steel conglomerate Essar Group – operated 56 call centers in 13 countries. Mounting debt at the parent company level, however, resulted in the sale of Aegis' operations in the US States and the Philippines to Teleperformance, the France-headquartered industry leader.

Profit margins subsequently fell as rising competition and falling demand meant the key markets of Malaysia, Saudi Arabia and India failed to make up for the loss of the lucrative and higher revenue-generating US market. In 2017, Capital Square, a Singapore-based private equity firm, offered to take out Essar in full. It paid $270-300 million for the business and soon began positioning it as a suitable acquisition target for a US peer.

"Executing back-to-back acquisitions is not easy," Chakrabarty says. "Doing a control transaction and merging two companies requires the ability to understand multiple dimensions of a company - its organizational culture, regulatory requirements, and market mechanics."

Know your target

It helped that Capital Square had earlier experienced a similar process. A year earlier, working in conjunction with CX Partners, it completed a $420 million exit from Minacs Group, which was also the former division of an Indian conglomerate. The buyer was US-based BPO provider Convergys. As a result, the private equity firm built up an understanding of the US BPO landscape and it knew which companies were interested in M&A opportunities.

Capital Square identified StarTek, a Denver-headquartered business that traded on the New York Stock Exchange, as its buyer of choice. Prior to 2017, StarTek had posted losses for six straight years. Three of the four leading US telecom carriers were its customers, together accounting for over 50% of revenue. The rise of interactive voice response (IVR) solutions and customer care apps, however, meant call centers were becoming less popular. The proposed merger between T-Mobile and Sprint, the country's third and fourth-largest carriers, was set to further jeopardize the company's future.

The challenge facing StarTek was easy to grasp but difficult to address: It needed to become more than a local BPO provider to stay relevant to US clients.

Capital Square presented a vision – a merger that could lead to the eventual creation of a globally competitive brand – that appealed to the company's majority shareholder. This led to StarTek acquiring Aegis in a cash-and-stock transaction with Capital Square taking a 55% interest in the new entity.

As the result of the merger, StarTek's international operations have grown substantially. Telecom carriers now contribute less than two-fifths of revenue. Meanwhile, the company that used to be Aegis – now able to bill clients from the higher revenue-generating markets in North America – has a more secure future. "StarTek brought the US and Philippines market presence [back for Aegis]. It also brought significant new growth opportunities in e-commerce. StarTek previously had a large customer engagement with a leading e-commerce player," says Chakrabarty.

The unification came at an appropriate time as well. Less than three months after the event, Teleperformance, which has 460 call centers globally, entered the Indian market by acquiring Intelenet from The Blackstone Group. In the same year, Concentrix acquired Convergys to create the second-biggest player in the US. In both their primary markets, StarTek and Aegis might have struggled had they continued on their own.

For the stakeholders of what used to be Aegis, the association with an entity listed on the New York Stock Exchange brings with it other tangible benefits such as a reputational boost, a perception of improved transparency and a brand with a longer legacy.

Patient stewardship

Following the removal of the CEOs at both companies, StarTek initially brought in Lance Rosenzweig, Aegis' former point man for the US, to lead the management team. Capital Square then recruited a CFO who had previously worked with them at Minacs and appointed Aparup Sengupta, an operating partner at the private equity firm, as chairman of the board. As CEO of Aegis in the first decade of the millennium, Sengupta is credited with turning the company into a globally competitive player.

After outlining the vision, Capital Square tasked Rosenzweig, and a management team comprising executives from both companies, with establishing global service delivery capabilities and global sales teams. The objective was to show clients that they were now being served by an improved operation that offered near shore, onshore and offshore call center capabilities. StarTek now provides customer care services across time zones in Southeast Asia, South Asia, the Middle East and North America.

"There are inherent benefits to being a global partner. For example, StarTek primarily delivered services in Spanish and English. With Aegis, it is now capable of delivering services to customers in more than 20 different languages," Chakrabarty says.

After making sure the right people were in charge in the US, Capital Square then turned its attention to the overseas operations. Rajiv Ahuja was duly hired as global COO of StarTek last year. Over a 40-year long career, Ahuja claims to have been a part of 18 acquisitions. Integrating disparate international operations and settling nerves has become an all-too-familiar task. It also helps that he's familiar with the non-US operation having earlier built much of it himself at Aegis a decade back.

"I was instrumental in building and selling the Aegis' Philippine business to Teleperformance. I was very familiar with half of the new company. I think I played an instrumental role in building what was Aegis [outside India]," he says.

While Ahuja was not at the company at the time of the merger, his assessment upon arrival was that Capital Square had opted for a mature and patient approach as the financial owner of two companies with very different cultural backgrounds. "Either you adopt a fast and furious ‘big bang' theory and put together a team that is going to address the integration challenges across the three broad domains – people, process and technology – or you wait for the dust to settle," he says. "Looking back over the past few quarters, I think CSP did the right thing by waiting for the dust to settle."

Earlier in the year, Sengupta was promoted to CEO after Rosenzweig opted to leave. The GP had earlier agreed that Rosenzweig would only stay for an interim period after meeting an agreed set of objectives. It was only towards the middle of 2019 that the two companies began operations under the unified StarTek brand, Ahuja says.

However, merely having a global presence may not be enough to safeguard StarTek's future. Some bullish technology start-ups believe a post-call center world might not even involve a human picking up the phone. Skand Bhargava, a practice director at Everest Group, says clients are also critically evaluating service providers by looking at whether they offer digital solutions as well as call center capabilities. "Scale continues to be important in this industry to drive better margins and deliver economies of scale but it's also about building adjacent capabilities," he says.

In particular, many BPO firms are investing in digitalizing back-end operations by employing agent-assisting software solutions that improve analytics and visualization capabilities. If they can speed up the phone call experience for both the employee and the user alike, there are contracts waiting to be won.

Purely focusing on "butts on seats" as the industry's long-preferred metric is expected to go out of fashion. Ahuja states StarTek is aware of such trends, but he believes there will always be a need for effective human-centered customer service especially as newer industries emerge that can replace falling demand from telecom firms. The in-house view is that customer service will become a lot more technical, involving helping customers deal with problems such as interacting with apps or solving other complex issues beyond bill payments.

Investments in such capabilities can now be made given StarTek's emergence as more than just a regional player. "With the capability of a much larger scaled organization, we can invest in newer areas such as digital [customer service] that is increasingly a requirement," Chakrabarty says.

For now, though, Ahuja's main task involves finalizing the global integration plans. To that end, StarTek appointed a new chief technology officer and global head of sales after Ahuja's appointment.

Consolidation continues

With the coronavirus pandemic muting investor sentiment across markets, the call center operator's stock does not have a positive outlook for the near term. As of March 30, StarTek's shares closed at $4.05. On the day of the merger, it reached $6.81. Even if the stock were trading higher, Capital Square would not be tempted to sell, arguing that it is too early to be considering an exit. Owning a listed asset, though, does give the firm several options that private equity owners seldom obtain so early.

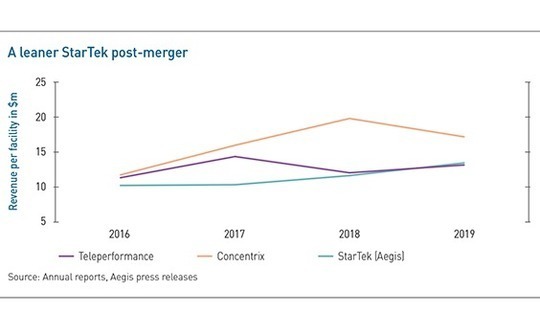

For the time being, the GP is focusing on cost and market synergies that have yet to be fully realized. According to its 2019 annual report, StarTek earned $13.4 million per facility based on consolidated results that combines sales figures from Aegis and StarTek centers. This compares favorably to EUR11.6 million ($12.7 million) per facility earned by Teleperformance but it is lower than the Concentrix figure of $17.1 million.

Nevertheless, StarTek is in a favorable position in an industry where consolidation is expected to continue. With the company's five largest call center competitors capturing less than 20% of the market, the pace of vertical mergers will quicken, Bhargava says. Later in the year, Synnex, the parent company of Concentrix, plans to list the business, which will bring back attention to the industry.

For Capital Square's Chakrabarty, the back-to-back deals also demonstrate that Asian private equity firms can go beyond providing growth capital and execute complex transactions. Not only did Capital Square recognize the right deal-making opportunity early on, the GP formulated and carried out a multi-year plan by leveraging its experience, network and financial acumen. "Everybody talks about operational leverage but when you translate it, it really comes down to whether you are able to operate in a seamless fashion in multiple markets," he says.

By doing so, Capital Square believes it has placed StarTek in a good position for the fourth decade of its existence. "There is an opportunity for consolidation [in the BPO sector] and we have contributed to that consolidation," Chakrabarty adds. "While it is a fragmented market, the number of companies that can do it on a global scale are not that many."

More on South Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.