India IPOs: Long-term horizons

Indian PE and VC investors expect domestic and overseas public markets to become increasingly attractive exit avenues for their portfolio companies as the global macroeconomic volatility dissipates

The public market debut of business-to-business (B2B) marketplace Indiamart earlier this month provided a welcome boost in what is proving to be a slow year for Indian private equity-backed IPOs. Raising INR4.8 billion ($69.2 million) after pricing its shares at INR973 apiece, the top of the indicative range, Indiamart ended its first day of trading up 34%. The price has dropped since then, but as of July 29, the stock was just below INR1,200.

India has seen only three PE-backed IPOs so far in 2019. In addition to Indiamart, Metropolis Healthcare and Polycab India, backed by The Carlyle Group and the International Finance Corporation respectively, listed in April and are both currently trading above the offer price. Despite the drop from this point last year, by which eight IPOs had already been completed, investors believe the success of these offerings shows that there is still plenty of appetite for companies that can check the essential boxes.

"Indiamart has proven that there's pent-up demand from institutional investors for high-quality companies," says Manish Kheterpal, a managing partner at Waterbridge Ventures. "But they made the cut because they were profitable, they were in a space that's very different from most of the better-known Indian tech companies, and they were the right size for Indian investors."

However, tapping this demand could be more difficult over the next few years, due to a combination of macroeconomic factors and sector trends in the domestic market that are expected to hold back IPO activity. These developments are expected to benefit private equity-backed companies over the long term, but for now investors must be willing to bide their time or look for alternative exit avenues.

Cycle after cycle

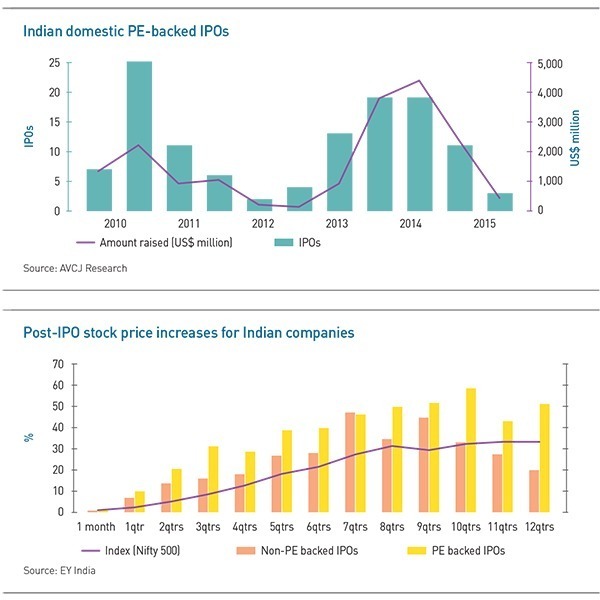

For industry veterans, the lumpiness of India's IPO market is a fact of life. AVCJ Research shows a regular cycle for PE-backed IPOs over the last 20 years: the peak years of 2007 and 2010 saw 27 and 25 offerings respectively, followed by the troughs of 2009, with seven listings, and 2013, with just two. After the most recent crest of 2016 and 2017, with 19 listings each, a drop-off in 2019 is well within expectations.

Added to this cyclical performance are several broader concerns such as India's recent general election, which created uncertainty about the future of the Modi government and its policies, as well as ongoing trade tensions between the US and China. Some of these issues have been resolved, but the volatility they fueled has had a chilling effect on the institutional investors that PE players rely on to snap up shares in newly listed portfolio companies.

"The headline Sensex has performed very well, but if you look at the underlying stocks, especially in the mid cap and small-cap space, many of them haven't done as well," says Sandip Khetan, a partner at EY in India. "Based on the headline numbers, your expectation of valuations might be very high, but there are no market participants who are willing to back up those valuations."

Reinforcing the impression of a pullback from public markets is a slowdown in filings with the Securities and Exchange Board of India (SEBI). Until September 2018, prospectuses from PE-backed companies appeared more or less every two weeks on the SEBI website, but this flow has largely evaporated. In the last 10 months only Coldex, a cold chain logistics player backed by Asia Climate Partners, has filed for an IPO, and no PE-backed companies have applied to list this year.

It is important to view the IPO numbers in context of the larger private equity exit story in India, which has also been depressed this year owing to many of the same macroeconomic factors. So far in 2019 IPOs stand at around 10% of total exits, close to the average for the last three years and significantly above the most recent low point in 2014. Trade sales have accounted for the greatest share of exits in terms of both number of deals and capital raised so far this year, as is typical for India.

In addition, while the lack of filings could indicate a slower pace of offerings in the next few years, there are still numerous PE-backed companies that have been approved for listing but have not done so yet. Investors might hold off on going to market until the timing is right, but they still have every intention of following through on their listing plans.

"There is a bit of softness in the market currently, and markets will be more selective about what kind of offerings can go through. But at the same time, it's not as if they are completely shut," says Padmanabh Sinha, a managing partner with Tata Opportunities Fund. "In our case, we are planning IPOs for two of our companies this financial year, and we think those should probably go to market, even if we have to be a little flexible on the timing."

Governance matters

One reason that investors remain bullish about the prospects for listings is increasing confidence in PE-backed companies among institutional investors. Financial sponsors are perceived as well-equipped to enforce higher standards of governance and reporting among their portfolio companies, even as minority investors. As a result, public markets have consistently valued these stocks higher than others.

A study last year by EY illustrates this preference. Of companies that have gone public since 2013, those backed by private equity investors at the time of listing consistently outperformed their non PE-backed counterparts. On average, by the second year after the IPO, the former had seen their stock price rise 51% above the offer price, compared to 35% for the latter. By the third year PE-backed companies stood at 52% above the offer price, while non PE-backed companies had risen 21%, a growth profile that underperformed the Nifty 500 index.

This comparison is not perfect: companies in different sectors will not perform identically, and not all sectors have an even spread of businesses with and without financial sponsors. In the retail, consumer, and food sector, for example, there are no companies with a vintage of more than four quarters that did not have private equity support at the time of their offerings. Nevertheless, the fact that PE-backed companies reliably outperform the Nifty index provides a powerful draw for public market investors seeking outsize returns.

"The capital markets in India aren't completely rational when it comes to valuing companies – you'll see three different companies in the same sector, trading at very different multiples," says Nitish Poddar, national leader for private equity for KPMG in India. "There are a lot of factors that can drive the valuation up and down, depending on how the institutional investors look at it – private equity support being one of them."

The perception of outperformance by private equity-backed companies has led to some shifts in market behavior. For example, Indian GPs are increasingly finding themselves sought out by companies that are planning a domestic listing and hope that an investment from a financial sponsor with international governance standards can provide them with credibility in the eyes of investors. KPMG is working on one such deal for an IT services company that intends to list by the end of 2020.

"The company has done well, but it's not backed by a larger company and it doesn't have a well-known brand, so not too many people know about it," says Poddar. "But with private equity coming in, people will say that they must be doing something right."

Growing institutional appetite for private equity could also lead to more willingness on the part of public market investors to back IPOs by Indian technology companies, but industry participants believe these are likely to remain rare. Aside from Indiamart, only a handful of VC-backed internet companies have pursued a domestic listing. The most recent was online matchmaking service Matrimony.com, which raised INR5 billion in its 2017 offering.

Reasons for the scarcity of IPOs in the internet space include the inherent conservatism of India's institutional investors, which are reluctant to back online companies that have yet to demonstrate a profitable business model. Regulatory hurdles also play a role. Though the government is working on easing some of the restrictions that have discouraged domestic listings, it can be difficult for industry professionals to make it clear to policy makers what changes are needed.

"A significant challenge for pursuing an IPO in India is the requirement of a minimum 20% promoter holding, which can be difficult for companies that have accepted multiple rounds of PE or VC funding," says Vinayak Burman, a managing partner at boutique law firm Vertices Partners. "Expecting financial investors to reclassify themselves as promoters, which requires three more years of lock-in after going public, makes an India listing problematic."

Coming to America?

Indiamart's IPO indicates that institutional investors are not completely opposed to supporting an internet business, but the company's profitability and relatively modest size put it in a very different category from better-known Indian e-commerce businesses. By contrast, homegrown online retail giant Flipkart forewent a listing last year in favor of a sale to Walmart at a $20.8 billion valuation.

A listing in an overseas market like the US is one way around the reluctance of Indian investors, but this route is not straightforward either. The last VC-backed Indian e-commerce company to list in the US was MakeMyTrip in 2010. None of its peers have followed this lead, as US investors are believed to be uninterested in companies focused only on Indian consumers. A globally relevant business model is required.

"US investors need to relate to the touch and feel of the companies they're investing in. If you're an enterprise company where your customers are Amazon and Apple, a US investor base will understand that easily," says Waterbridge's Kheterpal. "If you're developing an app for Indians to read local daily news, it's going to have much less significance to the US market."

This does not mean that Indian e-commerce companies have no chance for an overseas IPO, but they must find a way to broaden their operations. Oyo, the hotel room aggregator that is now present in 80 countries, is considered a prime candidate for an overseas listing. Educational technology start-up Byju's is also said to have the potential to go public in the US.

While Indian GPs acknowledge that the availability of IPOs is an important indicator of the health of the country's investment environment, they also caution against putting too much emphasis on a certain exit avenue. Provided the underlying company is healthy, there will always be an option for recovering the investment and providing returns to their LPs.

"We invest in high-quality companies. In our first fund we have six companies with a billion dollars in revenue or more, and five or six are in the top two in their segment," says Tata's Sinha. "If you meet those parameters there are multiple forms of exit available. I don't think we have ever backed a company saying that an IPO is going to be the sole form of exit that we pursue."

More on South Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.