Japan secondary buyouts: Between friends

Negative perceptions and local sensitivities have stymied the development of secondary buyouts in Japan. International GPs – plus some of their domestic peers – have the firepower to drive change

Ayumi is about to welcome its fourth successive private equity owner, a distinction achieved by few – if any – other Japanese companies. The sale of the drug manufacturer by Unison Capital to The Blackstone Group, which hasn't made a PE investment in Japan for nearly a decade, underlines how pan-regional and global firms are intensifying their focus on the country. It also draws attention to the relative paucity of secondary buyouts.

"The Japanese market has a low percentage of fund-to-fund transactions compared to Europe, for example. This is largely due to the strong appetite of strategic buyers – they have been willing to pay a high price for companies that have been cleaned up by PE investors. When a business is put up for sale by a fund and strategics are among the bidders, the GPs involved generally aren't hopeful," says Joji Takeuchi, head of private asset investments at Asset Management One, although he notes there are certain niches where PE is more likely to prevail.

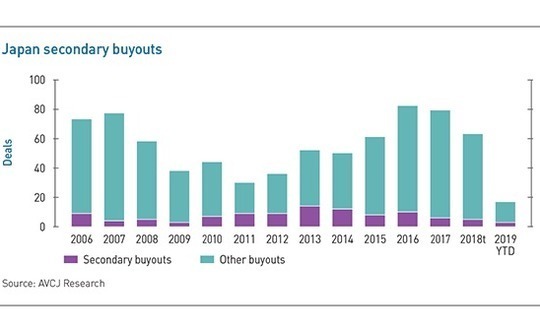

There have been approximately 400 private equity buyouts in Japan since 2011, according to AVCJ Research, and sponsor-to-sponsor deals account for less than one-fifth. Activity ramped up in 2013 and 2014, with more than two-dozen transactions completed, partly driven by investors ridding themselves of assets acquired before the global financial crisis. The momentum didn't last. The combined total for 2017 and 2018 was 11. While secondary buyouts appear to struggle with cultural and perception issues, several industry participants believe they will become more prominent.

"Secondaries are unpopular with some people because they assume the previous owner has done what needed to be done and there are limited value-add opportunities remaining," says Tsuyoshi Yamazaki, a director with Integral Corporation. "I don't think that's necessarily true. Each GP has a different style. We have a large team and we see ourselves as very hands-on investors. In previous deals, we have been able to make operational improvements."

Integral completed three secondary buyouts in its second fund, which closed in 2014: barbershop chain QB Net Holdings from Jafco, scaffolding manufacturer Shinwa from CVC Capital Partners and Mezzanine Corporation, and nail salon chain Convano from Ant Capital Partners. All three listed last year. The first deal from Fund III in 2017, call center business Customer Relation Telemarketing, was acquired from Advantage Partners. Yamazaki notes there are more secondary deals in the pipeline.

Optimal positioning

The notion of later private equity owners building on the work of their forbears is borne out by Ayumi. CVC and Jafco backed a management buyout of what was then Showa Yakukin Kako in 2004 before selling to AIG Global Investment – which became PineBridge Investments – Polaris Capital, and Tokio Marine Capital four years later. Unison took ownership in 2012.

"The size and shape of the business is totally different from when we bought it," says Tatsuo Kawasaki, a partner with Unison. At the time, Showa Yakukin Kako produced generic painkillers and fever reduction medication as well as dental products. The latter division was sold off and Santen Pharmaceutical's anti-rheumatic drug business was acquired, creating a more focused operation that relies on a network of physicians and orthopedists for distribution.

Unbundling non-complementary business lines was intended to make the asset appeal to strategic buyers. Secondaries account for only three of Unison's approximately 20 exits to date because the firm tends to focus on trade sales. Early on in an investment, it reaches out to strategic players to gain insights into the industry and explore potential partnerships. Not only does this support business development efforts, but these partners might ultimately become prospective buyers.

However, Kawasaki wasn't necessarily surprised that Ayumi has ended up going to a financial sponsor. "A portfolio of drugs has very stable revenue streams. When you can predict future cash streams, it is easier for a buyer to take advantage of leverage," he says. "There are also strong growth prospects. Demand for pain control medication is rising due to Japan's aging population, while the fever reduction treatments are often prescribed with influenza drugs."

Other consumer plays have followed a similar pattern. Advantage sold Komeda Coffee to MBK Partners in 2013, having taken it from 300 to 500 stores and doubled revenue over five years. Its return was 7.2x. MBK increased the store count to 747 and listed the business in 2016, making five times its money. Another Advantage expansion story, involving massage chain Riraku, culminated in a sale back to the founders in 2017. However, CVC bought the company a few months later.

When The Longreach Group bought coffee shop operator Kohikan Corporation last year, emulating Komeda's growth was an ambition – although perhaps not one that can be realized during the holding period. Should it get on the right trajectory, another PE buyer might step in. The same could be said for Wendy's First Kitchen, a burger chain Longreach acquired in 2016. Mark Chiba, the firm's group chairman, notes that the company has achieved only 15-20% of its store growth potential.

A common feature of the Ayumi, Sushiro and Komeda transactions is that they were sold by local GPs to pan-regional or global managers. There is an underlying logic to this: the companies required a larger equity check and a different kind of operational assistance to continue their growth. Nevertheless, there are mixed views within the domestic private equity community on selling to financial sponsors.

Reluctant counterparties

Tokio Marine Capital generated a 6x return when it sold Bushu Pharmaceuticals to Baring Private Equity Asia in 2015, but there have only been two or three secondaries out of approximately 20 exits in total. Koji Sasaki, a partner with the firm, notes that strategic interest is generally strong – Tokio Marine often receives inbound inquiries within days of announcing a new investment – and management teams sometimes want to avoid private equity ownership.

This view is echoed by Megumi Kiyozuka, a managing director with CLSA Capital Partners. "If a private equity firm offered a large amount of money and there were no other options, of course we would take it," he says. "But if we have other options, like an IPO or a trade sale, I would prefer to go with one of those. A private equity buyer means another layer of leverage, and I don't want to put the management team in a difficult position."

J-Star has sold one asset to a private equity fund, housing repair business Burn Holdings in 2014. Management lobbied for another financial investor because there was a desire to stay independent and go for an IPO. Greg Hara, J-Star's CEO, offers a similar explanation to the rest: a listed corporate that only needs to better its current return on equity of 9-10% is always likely to outmuscle a private equity buyer. Another reason is reputation.

"Most of the time when we buy company a lot of the goodwill is created. If a secondary buyer comes in there is more goodwill. At some point in the future that goodwill is impaired. No one knows when it will happen, but once it happens there is pressure on the balance sheet, possibly negative net worth, and it becomes harder to exit to strategic buyers or go IPO," says Hara. "We tend to stay away from secondaries because we care about continuing corporate growth after we exit."

Provided the balance between strategic and financial buyers remains tipped in favor of the former, this kind of seller's dilemma should be an infrequent occurrence. However, the emergence of local private equity buyers with larger funds and an appetite for bigger-ticket deals – as well as banks that are willing to provide financing – suggests a gradual shift in the industry dynamics.

Two secondary buyouts of more than $400 million in enterprise value have been announced so far this year. Blackstone was triumphant in the Ayumi auction, but a couple of domestic GPs were still in contention as the process entered its final stages. A few months earlier, Polaris Capital acquired aged care business Hitowa Holdings from CVC Capital Partners, turning on its head the notion that secondaries are all about local managers selling to global peers. The more capital entering the asset class, regardless of size and strategy, the greater the chances of it ending up in secondary buyouts.

"Secondaries emerge at some point in a private equity ecosystem and usually not at the front end of it," says Longreach's Chiba. "Much like co-investment, it should happen as the market matures."

More on North Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.