China online education: Passing the test?

Capital has poured into China’s online education sector in recent years, but with losses mounting and valuations called into question, investors are finding that not all business models are created equal

In the space of five years, Zhangmen has risen from nothing to a valuation of more than $1 billion. The Chinese company, which provides online tuition to students from elementary through high-school level, achieved this milestone on closing the first tranche of its Series E round at $350 million in February. China Investment Corporation, CMC Capital Partners, China International Capital Corporation, Sofina, and Genesis Capital were among the backers.

It is Zhangmen's seventh funding round since inception and one of the largest completed by any K12 player in China. The size of the deal underscores how far the industry has travelled in recent years. Not so long ago, companies struggled to convince investors and customers that students could be taught online just as well as in the classroom – and that leveraging technology such as artificial intelligence (AI) would translate into huge efficiency gains.

"When we introduced our online products to customers in lower-tier cities in 2015, some parents thought our salespeople were conmen and almost set dogs on them. While e-commerce was already huge in China, no one at that time thought education or after-school tutoring could be conducted via online platforms," says Xiaofeng Li, founder and CEO of Yimi Fudao, which provides one-to-one tuition for primary and secondary school students.

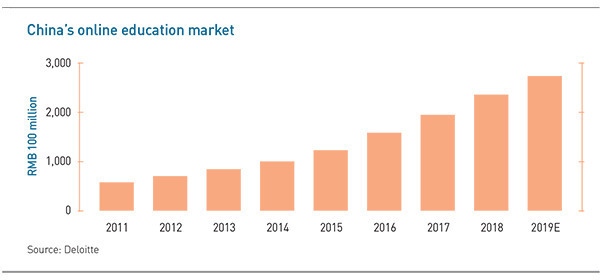

The breakthrough came on the back of increasing smart phone penetration and the development of China's internet infrastructure, which has made it easier for students nationwide to access online resources. Success stories such as Zhangmen and VIPKid – a one-to-one English-teaching platform that has raised over $825 million in the past six years – have also helped pique PE and VC interest. They deployed $6.4 billion in online education start-ups between 2013 and June 2018, according to Deloitte.

Despite this uptick in investment, the industry is far from mature. Investors expect it to stay fragmented for at least the next five years, after which a handful of companies will account for the lion's share of the market. Those with aspirations of joining the elite must find the right balance between rapid expansion and healthy cashflows. Eschewing profitability to pursue market share is not a viable long-term strategy.

"The logic of online education players is no different to some other internet companies. Both can chase scale first and worry about profits later. But investors in this space also need to consider whether the underlying business model of an online education start-up makes sense beyond whatever dazzling numbers a company presents," says Jay Gu, a managing director at Loyal Valley Capital, an investor in Gaosi Education, which supplies online teaching platforms to after-school tutoring companies.

The big picture

China's private education sector was worth RMB2.68 trillion ($387.6 billion) in 2018, underpinned by rising disposable incomes and parents who are willing to pay out if it means their offspring – usually an only child – can prevail in a fiercely competitive local school system. Even then, online only accounts for 9.3% of the market, suggesting potential for substantial future growth.

The industry is dominated by players that focus on tuition for school-age students in science, technology, engineering, and mathematics, the so-called K12 and STEM segments. Adult education and language learning come next, with early childhood education in last place.

Most private capital has therefore flowed into K12 start-ups, of which 15-20 are expected to become unicorns. Last year represented a new high point in terms of funding, led by a $500 million Series D-plus round for VIPKid. Zuoyebang and Yuanfudao raised $350 million and $300 million, respectively, while 17zuoye collected $250 million. Dada ABC's $100 million Series C seems small by comparison.

The relaxation of the one-child policy and regulations encouraging online education companies are expected to spur further expansion. Industry revenue is projected to reach RMB272 billion this year and continuing growing at double-digit pace. Investors looking to capture the scale of the opportunity can point to listed offline private education players TAL Education Group and New Oriental Education & Technology Group, which have market capitalizations of $4.3 billion and $13.2 billion.

"TAL and New Oriental have given investors unlimited scope to imagine the potential of online education. They were relatively generous in agreeing to the high-flying valuations of some companies last year, hoping that these players can grab much larger slice of the cake than their offline peers," says Jian Sun, a principal at Huaxing Growth Capital, a PE arm of China Renaissance, which is an investor in Zhangmen. "This frenzy has since calmed a bit and companies are becoming more cautious when burning cash to acquire customers."

Asked whether this valuation inflation will lead to a correction, several investors demur. They argue that the big will only get bigger and squeeze out smaller players. "If an online K12 player could grab 10% of the market generating RMB30-40 billion in annual revenue, then a valuation of $2-5 billion isn't overpriced," says Ray Hu, a managing partner at Blue Lake Capital, which backed Yimi Fudao.

Making money

The big question – as Hu admits – is when these companies will start turning market share into profits. At present, most of them are still loss-making because they are spending heavily on content and marketing, offering lessons at steep discounts to attract customers. This is especially true among one-to-one tuition platforms, although investors claim this business model is stickier because the quality of service is higher.

Teacher salaries account for over the half the cost of an online class, so the one-to-many (fewer than 10 students) and large-class (more than 50 students) models inevitably delivers wider margins. These providers are said to rely heavily on the brand-name appeal of "star teachers" who have built up a loyal following. But tuition cannot be tailored to the needs of the individual – less experienced tutors typically oversee smaller groups under the large-class format, with the star teacher leading proceedings – so parents may feel they are not getting value for money.

"For one-to-one classes, we aim to cultivate qualified teachers who are highly responsible and professional when facing students, but they are not star teachers," says Yimi Fudao's Li "They should also be able to deliver consultation and guidance in areas such as career planning."

Nevertheless, the economics of the one-to-many model cannot be ignored. Across the offline and online K12 education segments, one-to-many classes enjoy a 65-70% market share, followed by large-class tuition and then one-to-one. Perhaps most tellingly, the vast majority of online education providers that have listed or filed for an IPO are either pure-play large class platforms or offer a mixture of one-to-one and one-to-many classes. The reality is they are much closer to profitability.

Baijiahulian, which recently filed for a US listing, claims to be the third-largest player in China's large-class tuition market. Its revenue rose from RMB97.6 million in 2017 to RMB397.3 million last year as enrollments for paid courses increased from 65,092 to 552,294. The average number enrollments per K12 course went from 400 to 600. Over the same period, the company swung from a net loss of RMB87 million to a net profit of RMB19.7 million.

Regardless of how many students are in a class, successful online platforms can generally fall back on a track record of operating history in the education space, observers say. A company that has established a network of students and a consistent supply of teachers in the offline space is better-positioned to expand rapidly online. In addition, there is usually some upside in marketing online services to students sourced through offline channels.

Zhangmen is a case in point. The company started life as Zhuangyuan's Club, an offline K12 tutoring business established by students from several elite universities. In 2014, they changed course, selling all the brick-and-mortar study centers and recruiting online students and teachers from the existing offline base.

Yimi's recent merger with Juren, a subsidiary of US-listed OneSmart International Education Group, has a similar rationale. Juren has over 300,000 offline students that participate in large-format classes. Yimi plans to market its one-to-one and one-to-many – or small VIP – classes as a complementary service. In this way, the cost of acquiring new customers will be substantially reduced.

Another way to minimize marketing costs is avoiding the B2C segment popular among one-to-one players where services are sold directly students, or to their parents. Gaosi's customers are the after-school tutoring businesses that buy its online teaching resources and management systems. The company recently raised a $140 million Series D round led by Warburg Pincus; it was described as the largest-ever funding round in China's "K12-to-B" education space.

"The model of Gaosi allows it to have access to over 100,000 tutoring schools and avoid the competition in the K12-to-C segment. This is a light asset way of expanding quickly and thus we like it," says Loyal Valley's Gu.

Beyond K12

The consensus view is that the winners in China's crowded K12 space will be drawn from the current crop of market leaders. Even new entrants with ample funding would struggle to compete. There are, however, plenty of early-stage investment opportunities in other segments of online education.

Adult education, especially vocational training, is seen as having considerable promise. China's vocational training market was worth RMB76.8 billion last year and is on track to reach RMB100 billion by 2020, according to a report by Tencent. As Mariana Kou, head of China Education Research at brokerage CLSA, observes, it is easier to persuade an adult than a child to concentrate on a screen for a long period of time.

Most of the start-ups in this area focus on job hunting, IT management and qualification tests. While it is still highly fragmented, large players are beginning to emerge. They include Golden Education, which claims to be China's largest professional financial education provider. It raised RMB800 million in Series C funding – at a valuation of more than $1 billion – led by Hillhouse Capital and Morgan Stanley in 2018.

"A lot of workers in the manufacturing sector will be forced to find new jobs amid China's transformation from the world's factory into a more service and consumption-oriented economy, so demand for vocational training is expected to grow further," says Hu at Blue Lake.

Similar observations can be made for language training platforms that target adult customers. The market for online English-language tuition was worth RMB35.5 billion in 2017, according to government statistics, with test preparation for students looking to study abroad one of the key demand drivers.

Liulishuo, an English language learning app that uses artificial intelligence (AI) to deliver customized teaching solutions for adults, raised $71.9 million in a US IPO last year. The private equity-backed company operates on a freemium model, attracting students with free services and converting them into paying users. It also provides enterprise learning services to more than 100 corporate customers.

Liulishuo achieved sufficient scale for a listing, though costs continue to outstrip revenues. However, the further investors stray from core K12 education, the greater the uncertainty. Meishubao and VIP Peilian have received funding for education platform that focus on art and music, respectively, as they tap into the growing number of parents who want their children to have a more rounded education. But it remains to be seen whether subjects that do not feature on the standard curriculum will be able to achieve a critical mass of demand.

"Our biggest worry is how high the ceiling is for verticals like computer coding and art education. Are these segments large enough to support the formation of some unicorns? This is still a question to which we are seeking answers," says Sun at China Renaissance.

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.