China AI: Deep questions

Concerns around valuations, commercialization timelines, deal targeting, and brand perceptions are coming into focus as China’s AI ecosystem catapults to global prominence

In the course of a decade, China has become a global leader in artificial intelligence (AI) due to a combination of strengths in data collection and processing capacity, as well as a focused political agenda. A bubble has formed as a result but given the game-changing potential of the technology in almost every industry, there is little concern about it bursting.

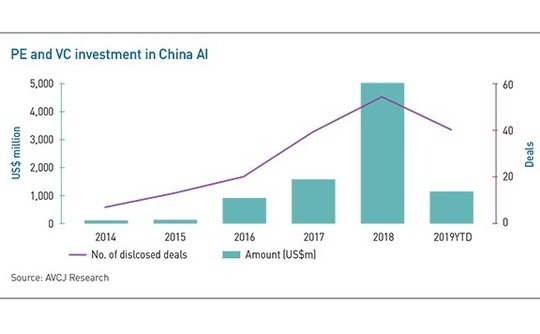

Private equity and venture capital investment in Chinese AI companies increased 3,500% over the three years to 2018, when about $5 billion was deployed across 54 disclosed deals, according to AVCJ Research. The parabola appears set to plateau this year, with only $1.1 billion invested to date. To be sure, much of the trend can be attributed to technology generalists rebranding themselves as AI, but the landmark deals do present a clear narrative.

Hong Kong-based SenseTime remains AI's global leader, hitting a valuation of $4.5 billion with its $620 million round last May. It is followed by Horizon Robotics, which raised $600 million at a valuation of $3 billion, while there have also been substantial rounds for Yitu Technology and Megvii in the past 18 months. Tellingly, all of these companies are heavily involved in the government-supported and ethically sensitive facial recognition segment.

AI's value stems from its potential across sectors, but in China, the most uniquely prospective domain is indeed video surveillance. This is an important indicator of the local market's relative complexity. AI owes its success in China to a range of exceptional factors with debatable merits, including intense government support and a sense that arguably oversized companies can offset bottlenecks around talent with superior access to data and risk capital.

"High valuations need to be supported by high levels of commercialization," says Yan Huang, a managing partner for the venture and growth team at CDH Investments, an investor in SenseTime. "Some of the newly emerged investors and entrepreneurs in this space are quite impetuous and want to chase quick revenues, which creates obstacles for companies taking their time to develop services. When we invest, we don't only look at how advanced a company's technology is – we measure how fast the technology is being applied."

False promises?

The chief concern is that rises in investment and valuations have not coincided with equivalent advances in technical capacity or practical deployment. A correction is therefore considered likely, but most investors are too bullish on the long-term to predict a serious retreat. The enthusiasm is taking tech hyperbole to a new level as many straight-faced developers graduate from calling AI the "next internet" to the "next electricity."

In China, the fervor comes with a feeling that AI will not be a winner-take-all opportunity set, nor one dominated by the country's IT oligarchy of Baidu, Alibaba Group, and Tencent Holdings. Business creation in autonomous retail offers a good case in point; while many international markets appear to be biding their time to see how Amazon fares with its "Go" stores, China has fostered a large but precarious start-up ecosystem in smart retail.

"More than 90% of companies in this field [AI] will face a survival crisis in the next two years," says Victor Ai, a managing director focused on new-economy investments at China Everbright. "We estimate that more than 75% of Chinese AI companies have less than RMB100 million [$15 million] in annual revenues, whereas more than half of them are valued at more than RMB1 billion."

The sticking point has been a lack of scaling milestones. Rolling out AI on a large scale not only requires an ability to train an algorithm to a market-specific dataset, but also an ability to retrain the system when new, more relevant data comes to light. Investors have been impressed by the initial integration of AI into Chinese businesses across several verticals, but they haven't seen evidence of continuous delivery – a key ingredient in commercial viability.

"There have been a lot of AI conferences showing proofs-of-concept and good demos by start-ups in controlled settings in the past 2-3 years, but the small to medium-sized enterprises that have actually started working with these players are quickly finding out that deploying the technology is a very different ballgame," says Aditya Kaul, research director at Tractica, a technology-focused market intelligence firm. "That's where a lot of AI is stuck now, and that's where the shakeout in China and the rest of the world will happen."

Wuzhen Institute, a specialist researcher in the field, estimates there are now around 3,000 AI companies in China. They received about $15.7 billion in total investment in 2018, which was 93% of the Asian total and 15% more than the US. It marked the first time China took the number-one spot globally after a 10-year build-up. Between 2009-2018, China has issued 68,000 intellectual property patents for AI, compared to 30,000 in the US.

Other bulls include Sinovation Ventures, which has backed five Chinese AI unicorns in the past two years, including Megvii, Horizon Robotics, financial technology company 4th Paradigm, autonomous driving developer Momenta, and crypto-focused Bitmain. The investor set up a RMB2.5 billion AI fund last year but warns the boom has been too focused on the technology itself rather than the industries being disrupted.

"There will be a consolidation and many companies based on data teams or teams with only internet backgrounds who are less experienced with the brick-and-mortar side of their businesses will face difficulties," says Peter Fang, a partner at Sinovation. "A lot of those kinds of AI companies get VC funding and the whole thing takes off, but that's not good enough if you want to survive. When VCs are investing in AI, they need teams that understand the traditional industries they're trying to revolutionize or infuse with AI."

This issue will slow things down most in the sectors with existing skills shortages. Healthcare, for example, has witnessed much online pharmacy and diagnostics experimentation but little in the way of real-world application. Similar observations can be made in industrial robots and autonomous driving, the latter of which has inspired construction of driverless car lanes on Beijing-area highways despite representing a negligible slice of overall traffic.

Follow the state

Investors can make use of these signals, however, as indicators of AI's likely monetization patterns as they pertain to China. Areas where the government is the customer, such as surveillance and perhaps regulatory tech, will be the first to mature. Ubiquitous smart phone usage has suggested that personal-use applications, including fintech models around insurance and payments, will be the next.

Smart city systems, which are typically subject to significant bureaucracy hurdles in other jurisdictions, are expected to follow on the back of concerted policy support, although widespread rollouts could take more than a decade. This will encompass autonomous cars and other transportation systems, as well as utilities automation and urban internet-of things. Logistics, supply chain, and more private B2B models may come even later.

Yin Qi, co-founder and CEO of Megvii, claims to see huge potential for AI to alter the way people live and work, comparing it to the industrial revolution and the development of the internet. He believes "almost every industry has potential to be improved and transformed with AI," but the question is when. "We have to be very disciplined about looking at areas where AI can add great value, and when a sector is ready to be commercialized," Qi says.

Megvii, also known as Face++, is arguably the oldest of the big AI players in China, founded in 2011, well before any audible government noises about developing the technology. The company is said to be mulling a $1 billion IPO in Hong Kong. The public sector represents a significant chunk of operations, with Megvii technology reportedly used by police departments in some 260 cities.

Security heavyweights in Chinese AI are keen to emphasize their range, however, and Megvii has done so by introducing its authentication systems to the banking and payments industry in partnership with Alibaba. Other explorations include algorithms for automating warehouses and imbuing videogame avatars with lifelike gestures and personalities. In the image detection game, these diversifications are important to public relations.

Concerns around the ethical implications of facial recognition AI have stirred a noticeable backlash against the technology that is starting to ripple through China, with SenseTime deciding this month to sell out of a security joint venture in the contentious western region of Xinjiang. Naturally, these pressures are most acute for less diversified companies.

As one investor puts it: "If you see a company that is only engaged with things like churning out surveillance technology for the government, you might want to be cautious about investing in it."

This notion was not lost on the founders of Clobotics, a group of ex-Microsoft computer vision scientists who made avoiding privacy issues one of their company's central tenants. The China and US-based start-up raised a $21 million Series A last year for a business model that uses AI-enabled cameras to monitor wind energy installations and brick-and-mortar retailers. For the latter, this means zooming in on shelves, not customers.

"We purposefully picked these two areas to operate in because we want to bring value to enterprise customers and solve business pain points – not get into debates about the sensitivity of data," says Claire Chen, co-founder and COO of Clobotics. "Data privacy is a big issue for a lot of AI companies, so we don't take pictures of faces or collect payments data. China is a perfect sandbox for us because we benefit from the large population but what we choose to do has nothing to do with people's identities."

Watch me

Still, video surveillance is roundly considered China's fastest-growing industry for AI. Other standout ventures include CloudWalk, a face recognition specialist focused on police work that has received almost $400 million from investors since 2016, and MiningLamp, a big data number-cruncher for the security industry that has raised about $500 million and expects to be profitable this year.

Early-stage technology investor Ceyuan Ventures sees this as a space where even small companies can achieve meaningful client contracts within three years. The firm's most direct AI play to date is DeepGlint, a video surveillance company that uses 3D imaging technology to improve security monitoring of large crowds. It is one of the few AI-focused verticals the VC deems ready for early-stage investment.

"There have been AI start-ups that have raised $50 million or more, and that's great for them, but that resource will only support their experiments for 2-3 years because they have to buy data, and talent in China is getting expensive," says Ye Yuan, a managing partner at Ceyuan. "That means bigger AI players have a significant advantage and start-ups with premature technology are being overvalued. But in 5-10 years, the start-ups with commercial capability will catch up to those valuations."

Hype has not been the only factor pushing valuations. Securing the services of AI professionals that are leaving bigger institutions puts pressure on start-up economics. Some Chinese AI unicorns are said to pay senior AI engineers up to RMB2 million a year. Even within companies where algorithm development is not the main business, AI talent is expected to become increasingly indispensable as the technology becomes a must-have.

AI investors are consequently compelled to maintain a "minimum asset" in technical expertise around machine learning and related software architecture support. A team in this sense acts as an insurance policy; if a portfolio AI company cannot realize its business development goals, at least it can market its technical know-how to a strategic buyer. Exit options in this vein could prove important if high valuations translate into a dearth of IPOs.

"We don't want to pile into a company with a valuation of more than $500 million because we don't think companies that have surpassed that mark could give us 5x or 10x returns," says Qin Qin, a partner at CreditEase Fintech Investment Fund, a vehicle whose portfolio is currently about 10% composed of AI companies.

The problem here is that in many AI segments, the smaller, more affordable companies may be difficult to invest in. Autonomous driving, for example, is seen as having extremely low tolerance for algorithm faults, which forces young companies to burn a lot of cash in the lab to be competitive. As echoed in several other categories, the internet giants have joined the traditional auto industry leaders, exacerbating economic barriers to entry.

"In the past few quarters, we've seen a trend where AI investors are now tending to put their money in top-tier start-ups, and that's creating challenges for newcomers," says Philip Ng, a partner and head of technology at KPMG China, noting that the overall AI market is stabilizing as it goes through a cycle seen in other hot investment areas. "Those in the angel or Series A stages will find it more difficult to secure funding unless they have a unique competitive advantage."

On the edge

There is reason to believe that China's AI start-ups will be in a good position to blueprint these competitive advantages. Ng adds that in the past 24 months, China has seen significant traction in the development of hardware and datacenters focused on AI processing. While physical AI infrastructure in the US remains largely the domain of the likes of Google and Amazon, China has witnessed some of its most interesting innovations in silicon at the start-up level.

If the trend holds, it could be a boon for China AI as a global transition unfolds toward "edge computing," in devices such as mobile phones, drones, cameras, robots, and virtual reality headsets. Edge frameworks are said to improve power management and performance metrics around latency and bandwidth by processing data with on-site hardware modules rather than with a cloud.

"China is unique in the sense that there are a lot of companies at the start-up level that are driving innovation in the hardware, infrastructure and chipsets on which you can build commercial applications," explains Tractica's Kaul. "Anyone investing in this technology long term needs to understand AI computing models are shifting toward this hardware edge and China, taking into account its local hardware manufacturing capabilities, has the upper hand compared to other countries in that trend."

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.