China distress: Dining on defaults

GPs expect a wave of non-performing loan sales in China as the slowing economy leaves banks with more bad debts to resolve, but could the distress investment opportunity be even broader than they envisage?

After months of speculation, the fate of Xiaomin Lai finally became clear in February. The former chairman of China Huarong Asset Management was charged with bribery, corruption, and, perhaps more surprisingly, bigamy. This is what happens when you are deemed to have taken illegal ownership of several public properties and RMB270 million ($40 million) of illicit cash is discovered in your home.

All in all, February was also a difficult month for Hong Kong-listed Huarong. Days after Lai was charged, the company warned investors that it was likely to post a 95% drop in net profit for 2018 due to declining valuations of some of its financial assets, losses suffered by non-financial subsidiaries, and an increase in interest payments on its loans.

Established in the 1990s, Huarong and its three fellow asset management corporations (AMCs) – Cinda, Orient and Great Wall – were mandated to help resolve non-performing loans (NPLs) held by China's major banks. However, in recent years they diversified aggressively, expanding into securities broking, investment, and high margin lending, with unfortunate results, particularly in the case of Huarong.

The combined weight of Lai's disgrace and AMC underperformance has resulted in these organizations facing increased pressure from Beijing to refocus on their core business. In April of last year, all four were said to have received orders from Beijing to fire staff and halt some of the operations at their Hong Kong-based subsidiaries – a clear sign that it wants to end activities unrelated to NPLs. As a result, distressed asset investors expect AMCs to start putting more portfolios of bad debts up for sale.

"Since last year, the Chinese authorities have put more emphasis on AMCs and expect them to refocus on their core business. This might indirectly lead to an increase in the supply of NPLs," says Wilson Pang, head of turnaround and restructuring services at KPMG China.

The big picture

These organizations might also be motivated to accelerate dispersals by the expectation of more bad debts arriving from banks as the economy slows and companies find they no longer have enough revenue to keep up with loan payments. And it might not end with the RMB6.3 trillion of NPLs officially recognized in the system. The most recent credit cycle has seen a proliferation of financial instruments, not to mention a huge pile of troubled real estate developments that must be cleaned up.

Hongzhang Lei, a department head at Great Wall, spoke last year of a "new era" in which the scope of distressed assets extend from the financial into the non-financial and from pure debt into equity and property rights. The question for foreign investors – which are arguably better positioned to take advantage of this credit cycle than any previously – is to what extent they are willing and able to participate.

"Although changing economic conditions in China may work to the benefit of these investors, success in China, more than anywhere, is likely to turn on having the necessary scale and on having access to an established and experienced domestic servicer to deal with all issues that can arise," says Damien Whitehead, a restructuring and special situations partner at law firm Ashurst.

It is impossible to draw an accurate picture of China's distressed asset space. In addition to RMB6.3 trillion in acknowledged NPLs – of which RMB2 trillion is still with the banks – lenders have a further RMB3.4 trillion in special mention loans that show signs of stress, according to PwC. Even these numbers may not capture the full extent of the distress. The official banking industry NPL ratio reached a 10-year high of 1.89% at the end of 2018, but some investors assume that the real figure is around five times higher.

At the same time, bad loans held by non-banking institutions are also on the rise, which include corporates' receivables – total receivables for large Chinese corporates stood at RMB13.5 trillion as of 2017 – as well as private and peer-to-peer loans. Based on a default rate of 2-10%, the number of NPLs in the non-banking system could be anywhere from RMB400 billion to RMB2 trillion, according to a note by Haoda Li, formerly an associate at Panda Capital and now head of global institutional business at Singapore-based cryptocurrency exchange Huobi.

Distressed real estate is even harder to measure. Industry participants put it at trillions of renminbi, with more than 30,000 developers thought to be struggling to raise new funding in the wake of the central government's deleveraging campaign. A wave of consolidation is expected in the sector, which could see many projects become available at knockdown prices.

Ready to reengage

For many international investors focused on NPLs, this isn't the first time they have sensed an opportunity as a credit cycle turns. China's first cycle in recent times started in 2001 and ended in 2007 when a government-orchestrated process to sell off bad debts faltered, and some GPs were left with nothing to do. A lack of large deals, aggressive competition from local investors and overly priced portfolios combined to dash the hopes of some of the firms.

A second cycle began to gain traction in 2015 and investors staffed up accordingly. They clearly remain interested, with China identified as a key target market for over 55% of respondents in a recent global investor survey conducted by Ashurst. Roughly the same number claimed to have deployed capital in the country's NPL space over the past two years.

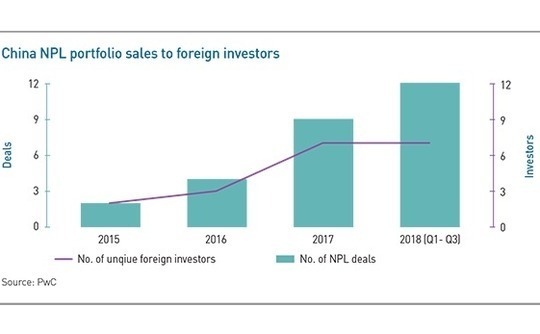

Foreign investors committed $1.5 billion across 20 deals in the 18 months to September 2018, according to PwC. Three more came in the final quarter, taking the total for 2018 alone to 15. Oaktree Capital, Lone Star, Goldman Sachs, PAG, Bain Capital Credit, and CarVal were among the buyers.

A tightening of NPL reporting standards is highlighted by investors as another reason why sales volume is surging. Since last year, the China Banking & Insurance Regulatory Commission (CBRIC) has required lenders to recognize all loans that have been in default for over 90 days as nonperforming. This represents a major shift from the previous more subjective assessment methods, under which banks were only obligated to add a debt to the NPL list if it had been in default for more than 12 months.

Meanwhile, aggressive competition from local investors appears to have faded. This is linked to the ongoing crackdown on banks and AMCs that have overindulged in shadow lending, including the extension of financing to investors that wanted to acquire NPL portfolios. New rules on wealth management products issued last year also cut off an important funding channel for local players.

"In 2016 and 2017 there was a pretty significant pool of capital purchasing NPLs in the form of renminbi-denominated wealth management products. Many of the groups raising that kind of capital had short-term vehicles that are not appropriate for NPLs, as these are usually longer-term assets. Now, some of these vehicles have shut down because they are struggling to repay retail investors says Benjamin Fanger, a managing partner at ShoreVest Partners. "Renminbi as a source of competing capital has receded very significantly, and some have even dropped out or quit."

These local investors were not necessarily in competition with the likes of Oaktree and Lone Star – which are seeking to deploy $50-150 million in deals – but their withdrawal from the market has contributed to a general reduction in pricing. "We continue to be very bullish on the market," notes Phil Groves, president of DAC Management. "The tightening credit domestically has limited the number of domestic competitors so it is a good time for foreign investors."

Prices dropped more than 10 percentage points between the first quarter and the third quarter last year, according to Orient. Industry participants anticipate further decreases, facilitating more deals and higher IRRs. "The prices don't seem to be attractive enough for us at this stage, so we are still waiting for them [to drop further]," says Xiaolin Zhang, CIO of Lakeshore Capital, who is best known as managing partner of Shoreline Capital. "We have an industry network nationwide to monitor price changes."

Selina Zheng, CEO of DCL Investments, adds that there are still regional discrepancies in pricing. She points to China's northeastern, central and western geographies to exhibit the most volatility, while more developed regions such as the Pearl River Delta are more stable.

Local insights

Part of the selling point for local players such as ShoreVest, Lakeshore and DCL is their ability to stay abreast of local nuances by leveraging on-the-ground networks that larger international players don't have. Lakeshore has 12 offices nationwide, while ShoreVest is planning to establish a team of up to 30 in Shanghai this year to complement its existing presence in Guangzhou and Beijing. Indeed, when Bain Capital Credit bought an NPL portfolio in 2017, ShoreVest was appointed master servicer.

These networks should prove useful as the China distress opportunity widens to incorporate more asset classes, structures, and institutional sellers. So far, there have only been hints at what might be to come. Lakeshore's teams, for instance, are not only there to track NPL pricing in different regions, but also to monitor companies that are likely to default. This points to the possibility of providing special situations-style structured solutions directly to corporates.

There is already evidence of investors approaching banks directly about loan portfolios, engaging in negotiations, and then running deals through AMCs for procedural reasons. This approach can result in more attractive pricing because the investors is effectively heading off the competition, but it also potentially opens up a litany of challenges that can only be navigated with the aid of local knowledge.

"How close a relationship does the investor have with AMCs? You need to understand the characters of the senior people to make sure they won't leak information," explains one China-based GP. "We have seen incidents where a deal that had already been negotiated with a bank was snapped up by another investor that offered a higher price after getting the information from the AMC handling the deal."

There is also the option of buying NPLs from local AMCs established to address bad loans held by smaller banks. There is almost no precedent of a foreign GP taking this approach, to the level of uncertainty is high, but at the same time, local AMCs usually hold newer loans due to their shorter operating history and the quality of the collateral is generally quite good.

Investors must make careful assessments of the economic and political situations of the regions or cities in which they are operating before they pile in, but it might only be a matter of time before they do. where the local AMCs are located to decide if they want to pile in. "We've had local AMCs ask us to partner up and co-invest in deals with them or buy assets from them," notes ShoreVest's Fanger. "We haven't done it yet, but I do see this happening at some point."

The menu of options is only expected to lengthen. In addition to pure NPLs and structured solutions, more activity is expected around the corporate bond market and debt-for-equity swaps involving Chinese state-owned enterprises. Real estate, meanwhile, represents a step into a different asset class with its own competitive dynamics. Warburg Pincus entered the space earlier this year through a joint venture with local player Hande Group, hoping its initial capital of $1 billion will become $5 billion within five years.

For many investors, partnerships will be the optimal approach as they look for an edge in deal sourcing. "You have to use all kinds of ways to approach key figures in the institutions that have good quality assets," says one local GP. "It doesn't really matter what means you use, but you can't miss the chance when a good asset turns up."

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.