Asia corporate VC: Company towns

Acceleration of development in the technology space is giving rise to a new generation of corporate VC investors. Building an identity separate from their parents is crucial to the success of these emerging firms

Nobody expects disrupting an established industry to be easy, and William Li knew better than most just how difficult the journey of a start-up can be. However, having launched two successful companies that bridged China's booming technology and automotive sectors – online marketing company Bitauto and electric car maker Nio – Li was also aware of the impact an entrepreneur could have with the right motivation and support.

Nio Capital, which was founded last year by Nio, Sequoia Capital China, and Hillhouse Capital, is Li's attempt to marry the two insights. The investment firm aims to leverage the experience of its corporate partner to benefit China's most innovative start-ups at a time when they need allies the most. In return, joining with companies like autonomous driving software developer Momenta at an early stage can bring Nio a decisive advantage when their technology reaches maturity.

"Since we first invested in Momenta, a lot of people have followed us, including some big names in the investment world," says Ian Zhu, a managing partner and co-founder of NIO Capital. "But more than that, we've brought them to customers and helped them to engage with large OEMs [original equipment manufacturers] in China. We're one of the most knowledgeable board members regarding the auto industry, so we can help them formalize their strategy going forward, which adds tremendous value."

Nio is one of a growing number of corporate players looking to help build Asia's technology ecosystem and gain an advantage for their own brands in the process. The expertise that these investors are seen to bring to their portfolio companies has made them a welcome addition to the investment community. However, most have also emerged relatively recently, and are still configuring their strategies. VC investors expect their corporate counterparts to play an important role in the entrepreneurial scene, but questions about their identity need to be resolved first.

The Asian angle

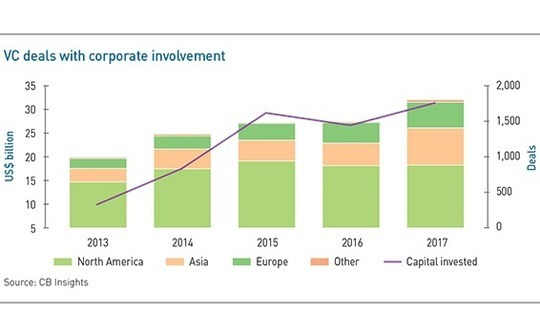

Corporate venture investing has been on the rise globally for several years. According to CB Insights, corporate investors participated in nearly 1,800 venture capital rounds last year, nearly twice as many as in 2013. Over the same period, total capital invested has grown nearly threefold, while the share of VC rounds with participation by corporate investors rose from 16% to 20%. In 2017, over 180 new corporate investors made their first investment, three times as many as in 2013.

Asia is becoming increasingly popular both as a source and a destination for corporate investors, with the region representing 29% of all corporate investments last year, up from 19% in 2013. Moreover, four of the 10 most active corporate VCs globally in 2017 were connected to Asian technology companies: Korea's KCube Ventures, now Kakao Ventures, and Samsung Venture Investment; and China's Fosun RZ Capital and Legend Capital (a VC unit of Lenovo owner Legend Holdings).

It is no coincidence that this boom in corporate investing happened concurrently with the rise of smart phones and mobile internet applications. As mobile devices grew in power and developers unlocked more and more use cases for them, established companies decided to join – or fund – the revolution rather than become casualties of it.

"That fundamental shift in technology and user behavior was the catalyst for a lot of investments as these players tried to protect themselves by investing in potential competitors, as well as being offensive and seeking out new opportunities," says Andrew Teoh, who helped to set up Alibaba Group's investment arm before leaving in 2011 to found Ameba Capital.

This cycle is now repeating itself, as the former generation of tech pioneers looks to stay abreast of a new cohort of rising start-ups. However, market participants have remarked on the speed with which some companies, barely out of start-up mode themselves, have set up their own investment divisions. Nio Capital was launched just three years after Nio itself, while rival Southeast Asian ride-hailing apps Grab and Go-Jek, both less than 10 years old, launched venture arms earlier this year.

"With the speed of development and innovation that's happening around some of these businesses, you need to be seeing what's out there so you know what's coming," says Shane Chesson, a co-founder and partner at Openspace Ventures. "A corporate venture wing is a good way to tap into that ecosystem and find out what else is going on, without tying down the management team."

Structural issues

These newly launched investment arms employ a wide range of funding structures. At one extreme are firms like Mandiri Capital, a financial technology-focused division of Indonesia's Mandiri Bank that invests solely off its parent's balance sheet. On the other end, Nio Capital, aiming to build a reputation as an independent player, invests from a RMB10 billion ($1.4 billion) pool of capital raised entirely from investors other than Nio, Sequoia, and Hillhouse. Management is also officially independent of the sponsors, though Li is a managing partner at NIio Capital as well as being chairman and CEO of Nio.

Nio Capital's structure is intended to forestall a common criticism of corporate venture arms: that they are ultimately beholden to the parent's strategic vision, insulated from the risk of their investments, and compensated without regard for the performance of their portfolio companies, and therefore not true venture capital at all. Zhu, formerly a partner at Chinese PE firm Tsing Capital, was well aware of this issue when setting up Nio Capital and determined to prevent it.

"We believe China's still going to be generating great companies 20 years from now, and we've set up our incentive structure in a way that we hope will promote collaboration and excellence," he says. "For example, our goal is to have equal partnership on the partner level, and we want everybody on the team to be incentivized with carried interest so that they are committed to the best performance of the fund."

Other corporate investors maintain that while their compensation tends to de-emphasize financial results, that doesn't mean they have no incentive to ensure good performance. Mandiri Capital's key performance indicators revolve around the firm's success in lining up collaborations between portfolio companies and a business unit at the bank, with quantifiable results. Employee compensation can be adjusted depending on the impact of these collaborations on Mandiri's bottom line.

Go-Jek Ventures is attempting a hybrid path, investing partly from Go-Jek's balance sheet and partly with capital committed by outside investors. This arrangement is intended to ensure that Go-Jek Ventures remains tied to the goals of its parent overall, while the staff feels a connection between their compensation and the success of its portfolio companies.

"There's a closer alignment with strategic goals in the event that it's fully funded off balance sheet, but then it becomes more and more difficult to motivate your talent," says one Southeast Asia-based GP that has backed both Go-Jek and Go-Jek Ventures. "On the other hand, if you're a purely LP-driven investor, then what do the shareholders of Go-Jek get out of letting you use the name?"

The incentivization question is just one aspect of a larger struggle to balance strategic alignment with freedom of action that tends to consume the first few years of a corporate investor's existence. This is a question that must be settled both within the parent organization and in the eyes of the larger investment and entrepreneurial community so the corporate investor can find its niche.

On the internal side, investment teams must have freedom to act on their own, even when they are constrained to balance sheet investing. Michael Di Cicco, a partner and head of Asia Pacific PE and real estate at Heidrick & Struggles who has helped several Asian corporate players set up investment units, has found that hiring a director for the division who will be able to stand up to the rest of the company is the biggest and most important challenge.

"You have to be able to share information and drive value to the business units, but you can't have those business units decide how you're going to invest," says Di Cicco. "Of course, if you start making larger and larger investments you're going to get more people involved from the business units and senior management, but you need a basic structure where you don't have to deal with all those restrictions."

Who's your daddy?

Corporate investors face some misconceptions on the investment side as well: for instance, that they are simply a vanguard scouting for buyout candidates on behalf of the parent company. While some such deals do result from an initial minority investment, most venture commitments by large corporates will not lead to an acquisition.

Of course, for most corporate VC investors their parent is far more often an asset than a liability, which they leverage as often as they can. In the case of Koinworks, a Thailand-based online lending platform focused on e-commerce merchants, Mandiri Capital proposed an investment that would give the start-up access to loan capital from Mandiri Bank, as well as the opportunity to reach a larger customer base. In return, the bank would gain access to Koinworks' proprietary credit scoring technology, which would give it an edge over competitors that struggle to assess creditworthiness of online businesses.

"Our selling point to a potential investee is that we can give you money, plus help you with traction, open up markets, and access the regulator," says Eddi Danusaputro, CIO of Mandiri Capital. "No disrespect to commercial VCs, but most of the time they just provide money. We can bring in the resources of Bank Mandiri, the Mandiri Group, and their customer base."

This is a common observation in the broader VC community, which highlights the complementary relationship of corporate and financial investing. Both types of investors bring their own resources to a portfolio company that, when deployed intelligently, can deliver better growth results than either can achieve on their own.

"A VC network tends to be start-ups and other investors, but a corporate network tends to be other corporates, and that can help them land partnerships and land deals," says Golden Gate's Lauria. "A VC can also provide you with guidance on how to grow your company, how to hire people, and how to run a board, while a corporate will come to the table with deep domain expertise."

Corporate investors even draw on different types of talent when building their teams, rather than competing for personnel. The incentivization structures play a role in this, since professionals that prefer a VC-style compensation tend to gravitate to the financial GPs, while the remainder gravitate to employers that offer a more stable salary.

Former VC professionals from the US and Europe have formed an unexpectedly large pool of talent for new corporate investment units to draw on. These executives are particularly useful since they have experience helping start-ups in emerging industries grow their businesses, and they are attracted by the focus that investing on behalf of a large, established corporate player can provide them.

"They have the capital to invest, so they don't have to be out fundraising all the time," Di Cicco says. "And they also have the reward of being able to make investments and see them have an immediate impact on the company. That's something that a lot of people have said they found very rewarding: you're not just investing for financial gain, you are having a strategic effect on a company."

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.