2Q analysis: Flipping out

Flipkart sets the tone as strategics deliver tech trade sale exits; Chinese internet players and healthcare are the trendsetters in investment; buyouts, venture stand out in Asia fundraising

1) Exits: Strategic interest in tech drives trade sales

Flipkart's tenure as the largest unicorn in India hasn't been smooth. In recent years, the e-commerce giant has suffered valuation markdowns at the hands of mutual fund investors, senior-level departures, the arrival of Amazon, and the collapse of a proposed merger with local rival Snapdeal. And then there was that nagging uncertainty about exits. India's first generation of unicorns are a decade old, and in the absence of mega IPOs, most investors have yet to see realizations.

Then in May, Flipkart's backers had their payday. Walmart bought a 77% stake in the company for $16 billion, allowing the likes of Naspers and SoftBank's Vision Fund to sell their entire stakes, while Tencent Holdings, Tiger Global Management, and Microsoft Corp. made partial exits. Just over 12 months earlier, Flipkart had completed a down round at a valuation of $11.6 billion; Walmart was able to justify a near 80% premium to that for access to India's online shopping market.

It is the largest trade sale ever seen in Asia and helped propel private equity exits in the region to a record $43.3 billion in the second quarter, according to preliminary data from AVCJ Research. The previous high point, which came in the final three months of 2017, was $28.8 billion.

Dollar values were up on the first quarter across public market sales, secondary exits to other financial investors, and buybacks, as well as trade sales. In terms of deal volume, however, the lull in activity that greeted the start of 2018 continued. There were only about 100 exits in total – the average for the previous 10 quarters is 155 – with public market sales notably sluggish due to global volatility.

As is often the case, a cluster of large-cap transactions moved the needle. Unusually, three of the four largest were trade sales involving technology companies. In addition to the Flipkart-Walmart deal, Alibaba Group agreed to buy the 57% of Chinese food delivery platform Ele.me that it didn't already own for $5.16 billion and Meituan-Dianping acquired bike-sharing start-up Mobile for $2.7 billion.

An assortment of private markets investors has profited from the two Chinese deals, some of whom were able to return capital to LPs rather than mark-up valuations on paper. Mobike, for example, was a cash-and-share transaction and Joy Capital – which was the sole participant in the company's Series A and re-upped in the next three rounds – took 90% of its interest in cash. The VC firm stands to make an 11x money multiple on its investment.

At the same time, these exits are significant not only for their size but also for their strategic implications. Walmart's acquisition of Flipkart is likely to change the competitive dynamic with Amazon for both companies, while Ele.me and Mobike can be factored into the broader battle between Alibaba and Tencent. Alibaba threw its weight behind Ele.me having sold its stake in Meituan-Dianping, supposedly due to the company's perceived closeness to Tencent, another shareholder. Tencent is also an investor in Mobike, while Alibaba backs rival player Ofo.

Japan cannot match China and India as a scale proposition, but the country also had reason to celebrate the prowess of one of its unicorns – indeed, its first unicorn – in the second quarter. Mercari, a consumer-to-consumer marketplace, completed a JPY130.5 billion ($1.18 billion) IPO that enabled Global Brain, East Ventures, Itochu Technology Ventures, GMO Venture Partners, World Innovation Lab, and Globis Capital Partners to realize JPY33.7 billion through partial exits.

With Raksul, another VC-backed IT play, going public as well, Japan accounted for two of the dozen largest IPOs – a list typically populated by Chinese companies. There were about 40 private equity-backed offerings for the three months ended June, the lowest quarterly total in two years, although the cumulative proceeds of $10.9 billion were above average for the same period.

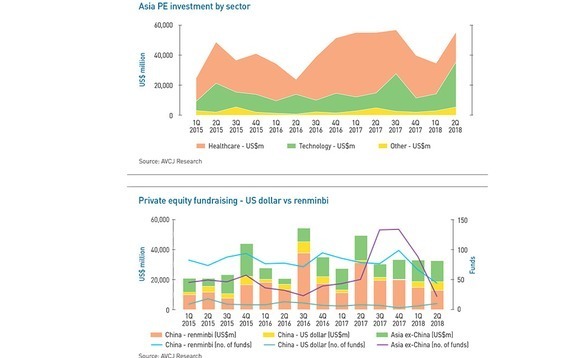

2) Investment: Ant Financial and the rest

Private equity investors deployed $55.2 billion in Asia between April and the end of June, up from a relatively meager $34.4 billion in the previous three months and just shy of the record total set in the third quarter of last year. Even more striking is the fact that more than $0.50 of every dollar committed went into technology plays – and one minority growth deal accounted for half the total for that sector.

Ant Financial is no ordinary start-up. It is the dominant operator in a global digital payments market dominated by China and has evolved beyond Alipay, the payments system devised for parent company Alibaba Group's e-commerce platforms. Its portfolio includes wealth management services, an online private bank, a credit assessment business, an enterprise services platform, and a string of investments in foreign and domestic tech companies.

Despite an eye-watering valuation of around $150 billion, Ant Financial had little trouble attracting participants for its $14 billion Series C round – the largest single fundraise by any company in the world. GIC Private, Warburg Pincus, The Carlyle Group, Khazanah Nasional, and General Atlantic are among the names in the company's blue-chip investor base.

Four of the five biggest investments from the second quarter involved Chinese technology players. Social e-commerce platform Pinduoduo received $3 billion months before filing for a US IPO, while app-based trucking logistics business Manbang and online financial services provider Du Xiao Man – a spin-out from Baidu – each raised $1.9 billion. There were also sizeable rounds for Ubtech Robotics and SenseTime, underlining China's growing significance in bleeding edge technology segments such as robotics and artificial intelligence.

Healthcare is the other key investment trend from the second quarter as private equity firms poured money into Chinese drug developers. China accounted for $2.9 billion of the $5.3 billion deployed in the sector and 51 of the 85 deals announced – the latter two figures representing all-time highs. A total of 27 Chinese biotech and pharmaceutical players received $1.7 billion between them. For context, the average for the previous 10 quarters is $583 million.

There are strong fundamentals underpinning these deals, notably the opportunity to acquire intellectual property (IP) in the US and turn it into treatments for launch in China. For example, China is home to 120 million of the world's 453 million diabetics and the anti-diabetes drug market is expected to treble in size over the next 10 years. Moreover, the move to allow zero revenue biotech companies to list in Hong Kong gives investors an additional exit option.

These factors have inevitably contributed to a ramping up in valuations – so much so that some specialist healthcare investors are spending more time on incubation, where they assemble a team to develop the IP. Incubation is also seen as a means of minimizing risk. Only about one in 10 drugs make it from phase one clinical trials to approval by US regulators. If the investors select the best people and the best product, the chances of achieving monetization are greater.

The joint largest biotech investment in the second quarter was Brii Biosciences, a company that is barely a month old and has the Greater China rights to four unproven products being developed in the US. But the experience of the founding team – and a partnership with Alibaba's health unit – convinced the likes of Arch Venture Partners, Boyu Capital, Yunfeng Capital, and Sequoia Capital to commit $260 million.

3) Fundraising: Something old, something new

Australia's GP community is by most accounts in decline as domestic LPs either pare their exposure due to concerns about fees or internationalize their portfolios. In this context, BGH Capital closing the largest ever first-time fund for Australia and New Zealand with A$2.6 billion ($2 billion) is even more impressive.

There is clearly still demand for brand-name firms – in the case of BGH, the brand is Ben Gray, formerly co-head of Asia at TPG Capital – raising relatively large funds. The Blackstone Group joined BGH among the significant final closes in the second quarter of 2018, having accumulated $2.3 billion for its debut Asia-focused PE fund. The firm now claims to have at least $3.8 billion in equity to deploy in Asia, including associated commitments from its global buyout program.

Meanwhile, The Carlyle Group led the fundraising rankings for the quarter, closing its fourth pan-Asian buyout fund at $6.55 billion. The vehicle is 31% larger than the initial target of $5 billion and 65% larger than its predecessor – which means Carlyle is very much on trend among the leading regional buyout players.

In total, Asia-focused managers received commitments of $32.4 billion during the period, slightly less than the previous quarter. However, the number of incremental and final closes fell below 100 for the first time in four years.

In seven of the last 10 quarters, more renminbi-denominated capital has been raised in Asia than US dollars. The three months ended June bucked this trend, as did the three months before that, suggesting the frenetic, largely government-driven activity in China over the last two years might be easing off. Chinese local currency vehicles raised $12.7 billion – with two government guidance funds accounting for three quarters of the total – while US dollar funds received $19.7 billion.

There was also increased activity in the venture space as VC managers collected $7 billion, the largest three-month total in seven years, if the China Venture Capital Fund-of-Funds – another state-linked vehicle that closed in 2016 – is excluded. Nevertheless, the rise of VC remains a largely Chinese phenomenon.

The list of final closes represents an interesting mix of established names, spin-outs from foreign GPs, and rising local stars. Qiming Venture Partners falls into the first category, having received total commitments of $1.4 billion across its latest US dollar and renminbi funds, as well as a US-China healthcare vehicle. It is joined there by Sinovation Ventures and Matrix Partners China, which raised $500 million and $750 million, respectively.

The spin-outs are Ron Cao and Chuan Thor, formerly of Lightspeed Partners China and Highland Capital Partners, respectively, who raised money as Sky9 Capital and AlphaX Ventures. And the local star is Vision Plus Capital Partners, which was established by one of the co-founders of Alibaba Group. The firm closed its second US dollar and renminbi-denominated funds at $250 million apiece.

More on Fundraising

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.