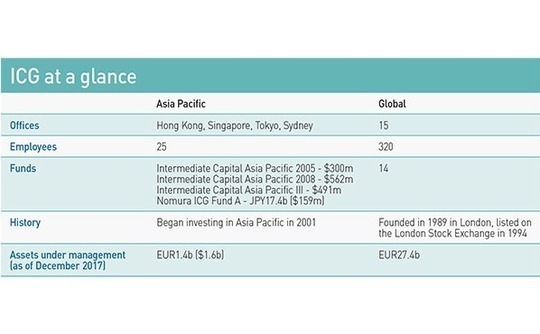

GP profile: Intermediate Capital Group

In recent years Intermediate Capital Group has branched out beyond traditional mezzanine to embrace deal structures that have no sponsor. It sees ample opportunities in Asia’s developed markets

Ventura Motors had reached a crossroads. The 100-year-old Melbourne-based company had an opportunity to acquire its competitor Grenda Transit Management and become the city's biggest bus operator. But to do so Ventura would need to raise A$155 million ($117 million) and it wasn't comfortable with the strings attached to the various proposed deals.

"Every discussion with private equity broke down because at a certain point the PE firm would say, ‘Now I want to buy your business,'" says Ryan Shelswell, who at the time was head of Australia equity and mezzanine at Intermediate Capital Group (ICG). "That's not what they had in mind: they wanted growth funding, they didn't want to sell control of the business, and they didn't want someone to be able to drag them to an exit."

With banks reluctant to lend Ventura the entire sum needed outright, the company turned to ICG for help with the financing. The firm initially offered to provide the required capital as mezzanine funding; when Ventura's lenders again rejected this idea, citing the high level of risk, ICG altered the proposal to a mix of mezzanine and a minority equity stake.

However, this too proved unworkable because the company's management worried that it would be too hard to buy out the investor in the future if needed. So the firm went back to the drawing board and returns with a loan structure that would mimic the returns of equity by tying the interest rate to Ventura's EBITDA, but would also allow management to buy out the debt at any time.

With this customized financing structure in place Ventura proceeded with the buyout of Grenda in 2012. Six years later the combined company signed a 10-year contract with the city government that greatly improved its perceived credit risk. With access to cheaper senior bank debt Ventura was able to buy out ICG's loan.

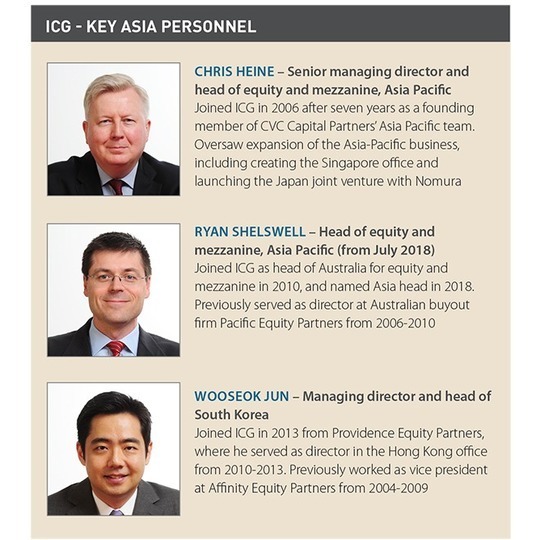

For Shelswell, who was recently picked to succeed Chris Heine as head of equity and mezzanine for Asia Pacific, the Ventura transaction is a perfect showcase for ICG's potential as a partner to business owners who seek financing on terms that private equity sponsors are unable or unwilling to provide. The firm still sees traditional mezzanine lending as strategically important, but it believes there is also considerable opportunity for credit providers that can work directly with borrowers. These deals are expected to play an increasingly central role in future investments.

In transition

When Shelswell joined ICG in 2010, the London-listed firm was still primarily known as a provider of mezzanine capital – in fact, that was how he had become acquainted with it, through his previous employer Pacific Equity Partners. ICG's reputation was that of a team that could find whatever solution a PE investor needed to make a transaction work.

"In every deal with a private equity sponsor you're trying to find cheap capital, but you're also trying to find flexible capital. And pretty much everything I ever needed or wanted, the ICG team found a way to provide," says Shelswell. "It wasn't usually the cheapest debt, but it worked really well. If you didn't have enough equity dollars, or you needed debt with certain characteristics, they were always able to structure something."

At the time, however, ICG's strategy was already in transition. The firm had begun to experiment with new deal formats in its European funds a few years earlier following the global financial crisis, and the response was promising enough that the investment approach was revamped across all the regional offices.

One of the biggest shifts was the adoption of sponsorless transactions as a central element of ICG's strategy alongside traditional mezzanine deals. The firm had always been open to this structure on an opportunistic basis, but the frequency with which the service was being requested led it to conclude there was enough demand in the market to warrant a more systematic approach.

"Quite often we will get a deal where the person on the other side of the table wants a particular solution and they can't get it through conventional means," says Heine, who has served as Asia head since 2006 and plans to step down in July. "He doesn't want too much debt in his company, and he doesn't want to give up control, so that eliminates a big part of our industry."

Sponsorless deals – known internally as corporate transactions – have emerged as an area of considerable focus in recent years. The firm believes that Asia's middle market holds myriad opportunities for its flexible financing solutions, to be used by companies that don't regard raising equity as an attractive option.

Yudo China Holdings, a South Korea-headquartered plastic injection molding specialist, is a prime example. ICG was approached by the company's founder, Francis Yu, who wanted a partner to help streamline Yudo's corporate structure ahead of a possible IPO. Over 14 months ICG assessed the company's far-flung operations and gathered sufficient information to make it comfortable to proceed with the investment.

The GP consolidated Yudo's 60 production, distribution, and sales facilities around the world under a new holding company in Hong Kong. This was accompanied by a $200 million commitment from ICG's third Asia fund that provided a partial exit for Yu, who was hoping to start the process of stepping down, and gave the firm a minority stake and a board seat through which it could further influence the business.

"For the first time the group has a single holding company structure, a single leadership, and all kinds of cost synergies," says Wooseok Jun, a managing director and head of South Korea at ICG. "We're going to have a consolidated set of numbers from 2018 onwards, and it positions them nicely for any kind of strategic options, including IPO."

Retirement plans

Succession planning is expected to be a major source of opportunities for the firm, as in the case of Yudo. Aging Korean and Japanese entrepreneurs are seen as significant contributors to this pattern, but ICG feels its history has shown that all markets in Asia are potential sources for deals of this kind.

Everlight Radiology, for instance, emerged as a succession planning opportunity in Australia in 2016. The radiology service provider's founders, who were approaching 70, wanted to sell the business and retire, and management was eager to raise financing to buy them out. But some unique features of the company made traditional private equity firms reluctant to get involved.

The first obstacle was the shareholding structure, which comprised two large positions held by the founders and more than 100 small stakes owned by previous investors. Under Australian law this put Everlight in the unusual legal category of an unlisted public company, or a company that is considered to have sold shares to the public without having listed them on a stock exchange. Acquiring such a business requires court proceedings to make sure all shareholders are protected, adding an extra delay that most investors do not want to bother with.

Another complicating factor was Everlight's joint venture with the UK's National Health Service (NHS), which raised concerns among potential investors that the partners might fall out in the future. Despite the Australian company's strong growth, the collapse of such a significant partnership could leave it without important revenue streams.

Despite these hurdles, ICG decided to go ahead and help management with the buyout. It reasoned that the NHS relied too much on Everlight's technology to risk dissolving the JV. More importantly, the complex ownership structure notwithstanding, ICG believed that the management was committed to making the deal work and that the legal process could therefore be managed, no matter how long it took.

"The management team can influence the exit so their support is essential. They liked what we were offering, and we shared the vision of the future of the business with them," says Heine. "The team on the ground in Sydney were able to build that relationship and position themselves ahead of the other bidders."

While corporate transactions constitute the most exciting opportunity for ICG, traditional sponsored mezzanine deals continue to play a major role in the firm's strategy thanks to its extensive experience in the field and connections with a wide range of GPs. Rather than a substitute for traditional mezzanine, ICG's managers see the corporate deal model as a supplement and a useful way to diversify its approach.

"There are times when there are tons of M&A deals in the market and high demand for sponsor mezzanine, and there are times when there's no need for mezzanine," says Jun. "If we were only doing sponsor mezzanine then I don't think we would have had the kind of results that we're seeing right now."

ICG's third pillar – opportunity – is a modification of the corporate deal model that the firm has recently begun to deploy. With opportunity, ICG plans to tackle restructuring situations involving companies that face more serious challenges, short of outright distress. The aim is to use the lessons learned through corporate deals to assist worthy companies in a section of the market where the firm has had little presence so far.

"There's always a lot of those opportunities around whenever there's a downturn, because people find themselves wrongly sized on their balance sheet in terms of how much debt they have," says Shelswell. "Too often people with bad balance sheets fall into distress. There are other funds out there that handle that, but we can help with balance sheet repair."

Market by market

ICG's recent activities in Australia across multiple strategies – in addition to corporate deals and mezzanine the firm also invests in Australian senior loans through its global fund – speaks to its confidence in the market. More broadly, the firm's strategy is rooted in investing in Asian markets where there are strong creditor protections.

Australia and New Zealand, the two markets ICG considers to be among the best in the world for creditor rights, are natural targets. South Korea is also attractive, not only for its creditor protections but also for the opportunities offered by the robust, developed market with a wide array of succession planning and corporate carve-out deals developing.

At the opposite end of the spectrum from Australia is mainland China, from which ICG has largely pulled back for now due to a perceived lack of lender rights. A similar pattern is seen in Southeast Asia, where investments mainly focus on Singapore – for instance, the buyout of tertiary education institution PSB Academy from Baring Private Equity Asia earlier this year. While the firm does consider deals in markets like Indonesia and Malaysia when approached by sponsors, it treads with caution because of the less developed creditor environment.

Japan is a special case: here the firm operates a joint venture with Japanese investment bank Nomura Holdings, founded in 2013 by an employee from ICG who left the firm to work at Nomura, then rejoined his old team later. Japan is strong on creditor rights, but its persistently low interest rates had held no interest for ICG to invest on its own. The employee prodded the firm to rethink its assumptions.

"He said that ICG knows how to do mezzanine deals, how to structure them, and how to assess credit risk. But the price is wrong for the rest of the Asia fund, so we weren't looking at this geography anyway," says Shelswell. "On the other hand, Nomura can easily raise the money and get access to deal flow. Why not create a JV and second people from both sides to work together just for Japan?"

The Nomura fund is now 70% invested, but unlike ICG's other vehicles it only targets mezzanine transactions; corporate deals are not part of its remit. ICG plans to reach out to more Japanese companies in its next pan-Asian fund. While ICG introduced its three-pillar business model through separate funds, its next fund will consolidate them all into a single vehicle. This is largely the result of demands from LPs that were exposed to only one of the previous funds and wanted access to the whole lot, since all were perceived as performing well.

ICG sees this as an encouraging sign for its newly adopted strategy, which at heart is about setting up deals that are not available either to straightforward PE firms or traditional lenders.

A recent transaction in New Zealand is a case in point. The founder needed financing to buy his partner's stake in the business, but refused another equity investor for fear of ending up in the same situation. Wary of the level of risk, banks demanded the founder take the company public in 12 months as a condition of lending him the money. However, ICG, noting likely cost synergies from a recent acquisition, felt the founder's position was much more secure than they gave him credit for.

"If you looked at it like a bank you would say nobody could do that as a debt deal," says Shelswell. "But if you looked at it like a PE investor you'd say of course you can – he's already taken the costs out, so the profit going forward is going to be much higher than the historical profit. So you can support more debt."

More on North Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.