Bolt-on acquisitions: Buying growth

Bolt-on acquisitions enable private equity firms to bring down the cost of investments through multiple arbitrage and leveraging synergies. But in a climate of heady valuations, are GPs thinking too big?

Navis Capital Partners was at a crossroads. The private equity firm had helped Celebrity Fitness grow from fewer than 20 gyms and a predominantly Indonesian footprint into one of the two largest players in Southeast Asia with 62 outlets across the region. The company had built a clear lead over direct rival Fitness First in Malaysia and Indonesia. But after 10 years, an exit was in the cards.

At the same time, a merger with Fitness First had been a lingering prospect since 2013, after a creditor group led by Oaktree Capital took control of the business globally. Last year, Oaktree began to break up Fitness First into its constituent parts and discussions with Navis accelerated. Here was an opportunity to create a business more than five times the size of its nearest rival: 152 clubs with 400,000 members in Southeast Asia and Hong Kong, and annual revenue of $295 million.

Faced with a choice between a satisfactory return through a trade sale of Celebrity Fitness and the potential of a much bigger payday following a merger with Fitness First, Navis opted for the latter; a deal was announced in February. It was not a decision taken lightly.

The private equity firm has a lot of capital at stake, having taken a 75% interest in the holding vehicle by rolling over its Celebrity Fitness equity and putting in a further $100 million-plus as Oaktree made a partial exit. It also needs to bring the two businesses together relatively quickly, with an IPO or trade sale targeted within 2-3 years. However, to Nick Bloy, co-managing partner at Navis, it was a necessary course of action in a challenging market.

"Around the world, and Asia is no different, entry multiples have gotten to be very high. That means beta is becoming very expensive. In order to create a decent absolute return, with some alpha baked into it, you have to think about doing things that are more transformative than business as usual," he says. "This is not restricted to a standard buy-and-build approach, but bringing together two very strong companies to create a dominant market position."

Bolt-on acquisitions are an established feature of Asian private equity, particularly in mature markets where control deals are readily available. But managers across the region appear to be increasingly willing to consider platform-style deals, in some cases writing bigger checks than they have before. The success of these deals rests on an ability to maintain strategic discipline and ensure effective integration. Some firms will inevitably bite off more than they can chew.

Cost conundrum

Broadly speaking, there are two forms of bolt-on transaction: roll-ups, where the investment thesis is largely driven by a belief that assets in a fragmented industry can be brought together to make a more efficient whole; and more conventional deals in which M&A is one of several tools used to help a company achieve growth by increasing scope, scale, geographic coverage or product diversification.

The unifying element is cost reduction. The average EBITDA-to-enterprise-value multiple for private equity transactions in Asia Pacific hit a record level of 17 last year, according to Bain & Company, compared to about 10 in the US. If a GP buys an asset at 17x, one way to bring down the overall investment cost over time is to buy some complementary businesses that are smaller and therefore command lower multiples. Further savings come by realizing the synergies between the companies post-acquisition.

"Auction processes and take-privates are increasingly competitive and therefore people have to squeeze as much out of the value creation plan as they can," says Andrew Thompson, head of Asia Pacific private equity at KPMG. "One of the surest, repeatable and institutionalized value creation tools is bulking up what you have by acquiring smaller businesses. You not only create scale value but also synergistic value through financial and operational improvement."

It is difficult to point to data-based trends in this area because the dynamics vary so much between different PE firms and markets in Asia. Japanese mid-market GP J-Star and small-cap buyout firm The Riverside Company, for example, consider bolt-ons part of their DNA because they started small and didn't have the capital to do larger deals. But both see this as one of multiple tools in the toolkit.

"As we grew we realized we liked investing in small companies and the strategy has always been about helping these businesses grow – if you can apply top-end-of-town disciplines into the low end of the mid-market you can build some incredibly valuable assets. Add-ons allow you to accelerate this strategy, but growth can be organic or inorganic," says Simon Feiglin, managing partner at Riverside. Four of the five businesses the firm bought last year in Asia were bolt-ons.

Similarly, Navis and Pacific Equity Partners (PEP) have been making bolt-ons since their inception in the late 1990s. PEP's record for the number of acquisitions by a single portfolio company is 23: these were completed over the course of 10 years as Link Group evolved from an Australia-only share registry business into a global financial services support business, ahead of an IPO in 2005.

The private equity firm has completed 27 platform deals and more than 100 add-ons over the course of 18 years, but the most recent of five acquisitions by baked goods company Pinnacle represents its boldest of recent times. Flour producer Allied Mills was bought for A$455 million ($344 million) – considerably more than PEP paid for Pinnacle in 2015 – with a view to creating a bakery business that sells everything from bagels to the ingredients used to produce them.

"Our approach is about driving performance and operational improvement, and add-on acquisitions are part of that," says Tony Duthie, a managing director at PEP. "When we did the due diligence on Pinnacle we saw an opportunity to grow market share organically and through buying smaller players. But Allied is more transformational than an add-on and those deals come along rarely. It is a significant task putting them together given their relative size and the potential synergies."

This is a risk the PE firm is willing to take. A similar mindset is evident elsewhere in the Australian market, notably in how some larger firms use bolt-ons as a way of avoiding the highly competitive big buyout space. Bain Capital, for example, bought after-school-hours care provider Camp Australia in February, a deal described as smaller than its average commitment. Last month, Camp Australia agreed to buy Junior Adventures Group, its only industry peer with national scale.

"There is integration risk in putting businesses together, but if you were doing a bigger deal, would you be able to get a free run at something and achieve that outcome in the same way? Probably not," says Mark McNamara, head of private equity at law firm King & Wood Mallesons. "The imperative for a lot of sponsors is getting capital out of the door at a decent pace."

Agent of change

This issue is pertinent to managers operating beyond Australia, and perhaps the most visibly transformative bolt-on acquisitions are taking place in markets where such strategies are less ingrained. Two KKR portfolio companies, based in China and Japan respectively, offer some pointers.

First, the private equity firm acquired a minority stake in Chinese home appliance maker Qingdao Haier for around $550 million in 2013 and then supported the company's acquisition of General Electric's appliances division last year. Second, KKR bought a majority stake in Panasonic Healthcare for JPY165 billion ($1.67 billion) in 2014 and a year later tacked on Bayer's diabetes care business for $1.15 billion, creating a global leader in the space.

Haier wasn't a bolt-on in the purest sense because KKR does not control the company, but both transactions are emblematic of how private equity investors can play a role as corporates in China and Japan look to expand overseas. "This is a sign of a maturing market," says Eric Marchand, an investment director with Unigestion. "Bolt-ons are common in Europe and the US, but we are seeing it happen more in China and Japan. Southeast Asia should also be a natural M&A playground."

The Bayer deal is also seen as a classic case of using M&A to bring down investment cost – KKR is said to have paid 14x EBITDA for Panasonic Healthcare, but recognized the potential for bolt-on acquisitions from an early stage. However, Panasonic Healthcare is also a strong business in its own right, so success wasn't predicated on the deal becoming a platform play. Industry participants see this as an important characteristic of any investment.

"You need to have a good foundation. If you bring things together just to create critical mass, it is not necessarily attractive. The risk is you put three ugly ducklings together and get an ugly family," says Riverside's Feiglin. "And in my experience, if you do a deal and justify the valuation on the basis of add-ons, you end up investing in something that is too small or in a sub-optimal geography, and you have to overpay and buy something you shouldn't have bought simply to get back to scale."

Quadrant Private Equity is arguably the most prominent exponent of roll-ups in Australia, but deals are still underwritten based on their individual merits. Within four months of closing its eighth fund last August, the GP had made 10 investments and committed about 40% of the corpus. Six of those 10 deals were under two newly-created platforms focusing on fitness clubs and tourism.

According to a source familiar with those transactions, the initial investment was made with term sheets for the add-ons already in place, offering a clear path to achieving scale. The economics of the first deal were therefore based on the others being completed, but beyond that, the platform is intended to be sustainable on a standalone basis; further bolt-on acquisitions offer additional upside.

The second concerns post-merger integration and the ability to deliver synergies by overcoming cultural obstacles in terms of managing employees, customers and suppliers. Greg Hara, CEO of Japan's J-Star, notes that some of the earliest lessons his firm learned came in branded foods. Specifically, the cost savings from combining manufacturing facilities were not large enough to make an impact on the bottom line and the customer response was weak.

"People said because we were manufacturing at different sites, the product tasted different. We didn't pay enough attention to that or we believed it could be overcome, but salespeople who were loyal to the brand became less loyal. We got a positive return, but we were expecting a bigger success," he explains. J-Star has since primarily focused on bolt-ons within services industries, citing the greater ease with which ideas, processes and software systems can be integrated.

Finally, M&A goes wrong due to poor timing. Even if a company identifies an appropriate acquisition target and executes an integration plan that delivers value, broader market conditions prevent that value from being fully realized.

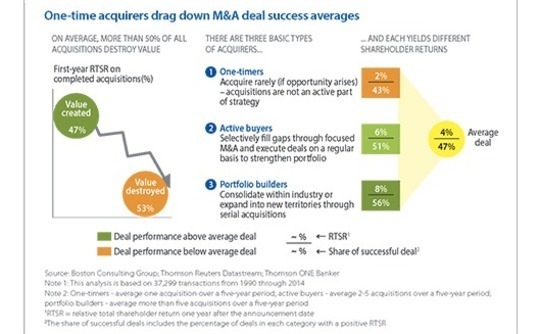

An analysis of more than 37,000 transactions from 1990-2014 by Boston Consulting Group (BCG) found that in just over half of cases M&A results in a negative relative total share return on a one-year basis. However, companies that regularly engage in deal activity – those that complete at least two transactions within a five-year period – are more likely to achieve positive outcomes than one-time acquirers. This bodes well for seasoned dealmakers in private equity.

"An advantage PE firms will have – provided it is transmitted to portfolio companies – is that they are deeply experienced in M&A and should they know how to get the strategy and investment thesis right up front, assist with due diligence and ensure management has a clear integration plan. If a company hasn't been acquisitive before, they can help them climb the learning curve," says Damien Wodak, a partner and managing director at BCG.

Be prepared

There are other reasons why a private equity approach to M&A might deliver different results than a corporate one. Notably, there is a tendency among corporates to set a strategy to enter new markets or product segments and then stick to it, even if this means paying a premium for certain assets. Private equity firms are generally more disciplined on pricing and their horizons are shorter, which means expansion plans are highly focused with a view to being additive in the near term.

At the same time, if high entry valuations are driving GPs towards increasingly ambitious bolt-on strategies, discipline might waver. This in turn puts more pressure on managers to make the operational side of a transaction work seamlessly. While global buyout firms have the resources to find solutions to problems, it is unclear whether the same can be said for smaller operators that are, for example, making forays into unfamiliar markets.

"When an acquirer is looking at a potential project, they may not be able to conduct sufficient due diligence to identify key areas for integration. Once the deal is closed they leave it to people on the ground who aren't from the deal team and don't understand the asset. That presents a lot of challenges," says Grace Tso, a partner at Baker & McKenzie in Hong Kong. "In more successful cases, the acquirer starts thinking early on about integration and an integration team is formed alongside the deal team to focus on particular issues."

Bolt-on acquisitions are expected to become more prevalent in Asian private equity – even if the current valuation pressure eases, the rise of buyouts in China and India will open up new options. KPMG's Thompson observes that if one were to ask most successful GPs globally where they found the biggest gains for the lowest risk in terms of value-creation endeavors, buy-and-build would feature prominently simply because it is an approach that can be institutionalized and repeated.

But in the pursuit of these outsize returns, not all bets will pay out. Private equity firms, particularly in emerging markets, are being asked to show they can do more than just find and close deals at short order. While a platform strategy may sound good on the fundraising trail, genuine skill is required in its execution.

"There is alpha inherent in the gamble but also risk," says Navis' Bloy. "You are trying to get the upside but you need people and capabilities that allow you to underwrite the risk. For example, if you have a single office in Singapore and you think you can go cross-border, it might be a risk too far. For those that start to do follow-on acquisitions and do them well, it will become a permanent part of their strategy. For others, it probably won't be."

More on North Asia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.