Hong Kong tax: A life less certain

Hong Kong introduced legislation intended to give private equity investors greater tax certainty, but the implementation guidelines have moved it further from this goal. The implications could be wide-ranging

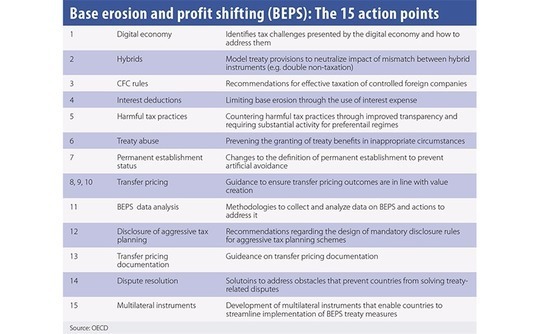

Will action point six be a deal-breaker for private equity? Of the 15 action points that make up the BEPS initiative - intended to stop investors exploiting gaps in the tax system to artificially shift profits to low or no-tax locations - the one on treaty shopping has perhaps been watched most keenly by the industry.

GPs rely on a string of offshore entities, from funds in the Cayman Islands to special purpose vehicles (SPVs) in Mauritius, to move capital efficiently around the globe. Double taxation agreements (DTAs) have become the glue that holds this system together, giving funds smooth passage between jurisdictions as well as tax breaks on dividend payments and other passive income streams generated by their investments.

Action point six could make the industry reconsider these processes. The questions it asks are not new, but the final report published last year by the Organization of Economic Cooperation & Development (OECD) codifies them and - once implementation details are agreed - will tie them up in a single multilateral document. It is expected to include a subjective principal purpose test designed to explore whether a structure has been set up to obtain a tax benefit. If that is found to be the case, DTA benefits would be denied.

"The OECD issued a consultation paper in March on treaty benefits for non-CIV [collective investment vehicle] entities. It asked: If you have a fund set up in Cayman and an SPV in another jurisdiction, should treaty benefits accrue to the SPV? Several questions of this nature were raised, but there are no recommendations yet," says Florence Yip, Asia Pacific tax leader for financial services at PwC. "Hong Kong is paying close attention to that paper. It is not an OECD member but it has to follow best practice."

The Hong Kong government issued a consultation paper on BEPS in October. The territory must now ready itself for rules that could redraw the international tax landscape. A principal purposes test would likely emphasize substance - the more of it, the less likely authorities are to look through investment structures - and Singapore is currently ahead of its neighbor in this regard. The Singapore incentives system, which involves bringing structures fully onshore, will no doubt face greater international scrutiny, but Hong Kong has yet to satisfy investors regarding its treatment of offshore entities.

"The substance required to access the tax incentives is such that it probably would not be questioned under BEPS; other jurisdictions would come under pressure long before Singapore," says Alexander Traub, Singapore-based Asia managing director at fund administrator Augentius. "In the last month I have met with two global firms that set up here just for that reason. They are comfortable with the tax treatment and they are comfortable there is enough substance for tax positions not to be contested."

Critical misstep

Industry participants are united in their belief that Hong Kong took a substantial - though not irreversible - step backwards earlier this year when the Inland Revenue Department (IRD) published practice notes relating to the extension of a local profits tax exemption to include offshore private equity funds. The extension came into effect in 2015 after years of lobbying by the industry for greater clarity on tax treatment, a clarity that was supposed to ensure Hong Kong could compete with Singapore.

Once covered by the exemption, PE firms with funds domiciled offshore would no longer have to set up structures designed to avoid triggering permanent establishment in Hong Kong and becoming liable for local tax. It would also make it easier to access the tax treaty network - funds must meet local substance requirements to qualify for treaty benefits and this could be done without risking local tax liability.

Recommendations made by the Financial Services Development Council (FSDC) ahead of the rollout were partially integrated into the legislation and the government kick-started a second process to introduce open-ended fund company (OFC) structures. These are intended to encourage mutual fund and hedge fund managers to raise Hong Kong-domiciled vehicles. However, it was hoped this could be the precursor to a revised local limited partnership ordinance, enabling private equity managers to bring their entire structure onshore instead of keeping the fund entity in Cayman.

The FSDC published a paper on limited partnerships in December 2015, drawing up a proposed legal and regulatory framework for the instrument. Observing the contribution private equity and broader financial services make to the economy, as well as the potential of serving as a conduit for a Chinese PE industry keen on outbound investment, it said that "promoting onshore PE fund establishment in Hong Kong is a natural extension and a corollary" to the OFC regime and the extension of the exemption.

The most contentious section of the practice notes issued this year that threaten to undo the previous good work relates to carried interest: Hong Kong has become the only major private equity center to declare that carried interest will be taxed as income rather than capital gain. But other parts of the notes, specific to the use of the tax exemption, are also concerning.

"The HKVCA [Hong Kong Venture Capital & Private Equity Association] has consulted widely with its members to discuss how useful to them this new law will be, now that the practice note has provided some details on some of the interpretations. The reaction is that it will provide little benefit to most PE firms with Hong Kong operations," says John Levack, managing director of Electra Partners and chairman of the HKVCA's technical committee.

Adam Williams, a Hong Kong-based tax partner with EY, adds that most GPs at present are still relying on the traditional approach where the fund, SPVs and fund management entity are located offshore while the Hong Kong sub-advisor undertakes certain limited activities onshore.

"The intent behind the rules, was to provide certainty that would allow managers to undertake additional functions in Hong Kong without exposing the fund itself to Hong Kong tax," he says. "Unfortunately, where things are at the moment is that there are a few areas that require further confirmation before GPs will have the certainty they need to bring additional decision making activities into Hong Kong."

Tainted love

There are two major concerns: the tainting of a fund - in that it no longer qualifies for the tax exemption - if its exposure to Hong Kong-based assets crosses a certain threshold; and the narrow definition of SPV activities, which prevents a manager from building substance in Hong Kong.

The tainting issue exists largely as a means of preventing local companies from using offshore fund structures to convert taxable profits into non-taxable income. As such, a qualified offshore private equity fund is unable to hold Hong Kong real estate assets or shares in a company with business operations that exceed 10% of the overall value of the target company - with a three-year look-back period starting from when the investment is made. And a single deal could taint the entire fund.

"Say you have an investment in a mainland company, and that company invests in a Hong Kong subsidiary. The subsidiary does well - it is worth more than 10% of the mainland company - and within three years you exit the investment in the mainland company. Your fund gets tainted," explains one investor. "Or if you are a minority investor in a Chinese company, you might not even know that it has bought a property in Hong Kong, but the valuation could be enough to invalidate the entire structure."

On the treatment of SPVs, the government's concerns were also rooted in tax avoidance, specifically the notion that it could encourage the round-tripping of Chinese money into Hong Kong and back into China purely to take advantage of DTA benefits. According to the practice notes, a qualifying SPV must be established for the sole purpose of holding and administering one or more private investments. They specify that an SPV cannot trade, be compensated by an offshore fund for the provision of services, or be involved in the management of portfolio companies.

"The activities of the SPV are restricted to: the review of financial statements of excepted private companies normally made available to shareholders or investors; attending the shareholders' meetings of excepted private companies; opening bank accounts for collection of dividends or investment receipts; and appointing company secretary and auditor," the notes say.

In short, the SPV would not be allowed to do any of the things typically required to prove substance in a jurisdiction, obtain a tax residency certificate, and take advantage of DTA benefits. As a result, there are limited economic grounds for establishing an SPV in Hong Kong in the first place.

"We wanted to get a clear exemption for the private equity funds, so we are competitive with the likes of Singapore. In addition, we wanted to make use of the substance we have here, so Hong Kong could be used as an investment holding location for the investments made by PE funds," says Darren Bowdern, a Hong Kong-based tax partner at KPMG. "But when it comes to implementing, intent can get watered down because the focus is on potential abuse by other taxpayers. As a result, we are in a position where it is so restrictive in application I'm not aware of any funds that would use it."

Anthony Lau, a tax partner with Deloitte in Hong Kong, sees a further limitation in the IRD's definition of qualifying funds as "bona fide widely held." The requirement is that there be at least 50 investors in a fund and that no fewer than 21 collectively hold interests in the vehicle that entitle them to at 75% or more of the income or property of the fund.

"The IRD doesn't want local funds to disguise themselves as offshore funds to take advantage of the tax exemption. They are saying the fund will still qualify for the exemption, but Hong Kong resident investors will be taxed directly unless it is ‘bona fide widely held' - a genuine fund that is marketed to many investors rather than just a few Hong Kong residents. However, the threshold will be difficult for many private equity funds. Typically they have fewer investors than hedge funds," Lau says.

Industry participants see little possibility of the practice notes being rescinded, but neither is the situation as it stands likely to precipitate a mass exodus from Hong Kong to Singapore, although it is becoming increasingly difficult for organizations such as the HKVCA to convince members to be patient and that a better deal is around the corner.

However, the current offshore-onshore system may not offer a long-term solution in a post-BEPS world, or indeed whatever global regulatory initiative follows that. Needless to say, an onshore fund structure would suffice in that it removes the need for an offshore exemption and brings fund and manager under the umbrella of a single jurisdiction with a substance requirement that stands up to international scrutiny.

The problem is that the OFC regime intended to serve as a launching pad for workable local limited partnerships has been causing frustrations of its own. The structure must be exempt from local taxation - otherwise no one would use it - but the IRD said in its initial guidance that to achieve this a fund should fall within the current offshore fund exemption, i.e. a Hong Kong-based vehicle should be managed anywhere but in Hong Kong. While the implication is that the political obstacles to such legislation would be too high, there may be a way of using existing regulatory infrastructure.

"We think this could be addressed quite simply: if the onshore fund is licensed by the SFC, which is one of the requirements for it to be an onshore fund, then that should be on its own sufficient to get the exemption. It doesn't need to be a non-resident fund, just as long as it's licensed and satisfies the other conditions," says KPMG's Bowdern.

At the same time, he warns that the stance taken by the IRD on the offshore exemption does not inspire confidence within the industry for a user-friendly onshore regime. If there is a risk of local taxation, people will just go elsewhere.

Future plans

Given Hong Kong's last limited partnership law was written in 1915, considerable changes would be required to get the ordinance to a level at which it offers Cayman-style flexibility. Moreover, the practice notes debacle raises the question of whether there is sufficient political and regulatory will even to take small steps towards a more user-friendly outcome.

At present, Singapore's requirements for substance, and therefore tax residency, might be daunting for a private equity firm that wants to set up a fund structure - typically a sub-fund that sits below the Cayman master vehicle - and a string of SPVs: annual business spending of at least S$200,000 ($140,000); at least three investment professionals on the payroll locally; annual tax filings with the Monetary Authority of Singapore; and, in certain cases, mandatory use of a local fund administrator.

But changes in the global tax landscape could prompt a reassessment of these economics. If the jurisdiction in which a PE firm makes an investment questions the structure on the grounds that capital is pooled in Cayman and routed through other locations to extract DTA benefits, Singapore might become a location for master funds, not just sub-funds. Similarly, if DTA access is conditional on passing a principal purpose test, there could be a push into locations where fund management activity can be concentrated and aligned with fund structure, and where certainty of treatment is available.

"If you can structure your business in a way that your fund, your fund manager, and fund holding platform are all located in the same country, you are placing yourself in the best possible position to satisfy that principal purpose test," says EY's Williams.

Singapore has made its qualification criteria more stringent in response to scrutiny of its tax incentives system, such as requiring managers to have at least S$250 million under management; Louisa Yeo, a Singapore-based partner with EY, describes the government's stance as "making sure it is compliant on the world stage while staying relevant to the funds industry." In the meantime, Hong Kong risks getting left behind by not rolling out the necessary infrastructure in advance.

The main loser in the long term could be the territory's financial services sector. The FSDC paper on limited partnerships noted that private equity is not a large employer - around 3,220 people were working for PE firms in Hong Kong in 2014 - but services outsourced by the industry have a substantial multiplier effect. It estimated that private equity sustains an additional 10,000-20,000 jobs in Hong Kong, and that for every $100 billion under management, a locally-domiciled fund would need to spend at least 1% on payroll expenses and other service providers.

"The uncertainty that is introduced by the practice note means that few of HKVCA's members will add management activities to the advisory role currently being performed in Hong Kong," adds Electra's Levack. "This is disappointing as a deeper operational role in Hong Kong would have created new jobs here."

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.