Asia PE-backed IPOs: Fits and starts

Development has been inconsistent in Asia’s IPO markets, with frequent pacing issues and challenges unique to each region. But in the right hands, they can still be highly rewarding for PE investors

With proceeds expected to reach up to A$1.12 billion (A$843 billion), the forthcoming IPO of Ingham's Enterprises will be the biggest PE-backed offering in Australia in more than two years and the fifth-largest on record. The listing of the TPG Capital-owned poultry producer is also taking place against the backdrop of the Dick Smith scandal, whereby the sporting goods retailer imploded two years after its own IPO and one year after Anchorage Capital Partners sold the last of its shares in the business.

As the first large-scale offering involving a private equity sponsor since Dick Smith entered receivership in January, and with a legal action making its way through the courts, Ingham's will be seen by some as a signal of the industry's future direction.

"Australia's one of the very few parts of the world where you can put forecast financial information into a prospectus and therefore sell off that forecast," says David Willis, Australia private equity leader at KPMG. He expects future PE-backed IPOs to feature more emphasis on the GP's post-IPO holding and consequent alignment with management and incoming shareholders, and less reliance on such predictions, which investors may now suspect of being overly massaged.

The Dick Smith dilemma may be particular to Australia, but investors in each of Asia's biggest IPO markets - Australia, China and India - have their own grievances to air. Though the draw of an offering in terms of potentially positive public relations and return on investment is undeniable, the environment is far from universally hospitable to exiting GPs, and those with more enthusiasm than sense may run aground.

Asian PE investors still see considerable value in IPOs, but their reliability as an exit strategy is hampered by the restrictions, both written and unwritten, that each market imposes on companies trying to achieve a listing. GPs unwilling to deal with these issues must be willing to accept alternatives, even for potentially lower returns.

Liquidity events

IPOs have historically been a major part of the PE toolkit in Asia, but their prevalence against other forms of exit tends to shift dramatically. Over the last 10 years, the IPO share of overall PE-backed exits has swung between a high of 15.2% in 2007 and the low of 1.9% in 2012, with other crests and troughs intermittently. This compares to ranges of 15.6% and 4.9% in North America and 14.4% and 2.9% in Europe, according to Preqin. In North America the figure has been more stable than in Asia as well, remaining between 10% and 14% in seven of the last 10 years.

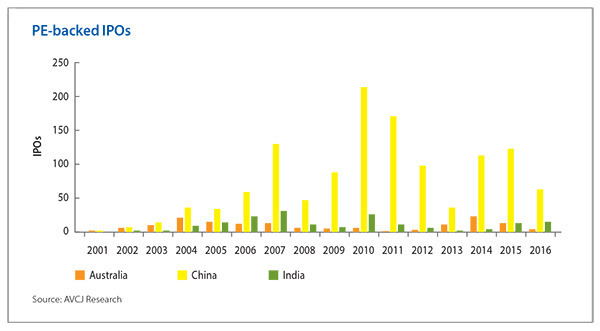

Examining the individual markets reveals some interesting trends as well, with each showing individual spikes over the last 10 years. In China, PE-backed IPOs reached peaks in 2007, with 130; in 2010, with 214; and in 2011, with 171. The combined total for 2010 and 2011 is larger than the total for both Australia and India since 2003.

As interesting is the precipitous drops between these bounces, when China's IPO exits have reached their lowest points. These falloffs have become a common sight for the country's PE investors, who have seen the government step in multiple times to suspend listings on the A-share market. Such interventions are usually motivated by a desire to reduce volatility - the most recent suspension happened last July - but the most protracted, in 2013, was intended to give regulators time to introduce closer scrutiny of listing candidates.

"I knew of a company in 2015 that went through the entire process, they even had the IPO proceeds in the bank, but the government stopped it," says J.P. Gan, managing partner at Qiming Venture Partners. "So this kind of government intervention can have a tremendous psychological as well as physical impact on a company."

Whether justified or not - and many point to the backlog of IPOs that builds up when the suspension is in place as proof that it is counterproductive, since it results in a flood of liquidity when the suspension ends - the possibility of government intervention is an irritating fact of life for Chinese companies pursuing listings. Those caught in the net have little recourse but to wait, or withdraw their applications.

Another challenge for a domestic IPO is the time required; even without suspensions, approval from the China Securities Regulatory Commission (CSRC) can take as long as three years, after which candidates may have to wait another year to actually list. During this time companies are forbidden to raise funds or make major acquisitions, leaving them less able to respond to changing circumstances. Those that make it to the end may find that the market has shifted so much in the previous four years they are less attractive than they thought they would be.

These limitations aside, domestic IPOs continue to be an attractive exit for PE firms - and an essential one given most investments are minority stakes acquired from company founders who have no interest in exiting their business through trade sales. Furthermore, companies that successfully make it through the process can at present achieve higher valuations than on any other bourse, and liquidity is strong as well. It takes an undeniable commitment, however - one GP says that a company must make achieving the listing its only goal for the duration of the process - and many investors look for other avenues.

A Hong Kong listing is one option for impatient entrepreneurs. The exchange has much shorter time requirements; the application process takes only nine months, and listing can be achieved six months after gaining approval. Companies that go this route can benefit from the freedom and flexibility it affords.

"In Hong Kong, once you satisfy the listing requirement, you will get approved for listing; the question is whether there will be enough cornerstone investors and whether the valuation is attractive enough for an IPO to take place in Hong Kong," says John Gu, a partner at KPMG China. "And we have clearly seen cases of private equity firms building positions or trying to sponsor a portfolio company to go for IPO in Hong Kong when China shut down the IPO applications."

US listings are also an option, of course, and many Chinese entrepreneurs have pursued IPOs on the New York Stock Exchange (NYSE) and NASDAQ, where tech companies are particularly well represented. A total of 133 PE-backed companies have gone this route since 2001; the largest by far was Alibaba Group, which raised $25 billion in 2014.

Spike down under

Australia, meanwhile, saw its biggest spike in more recent years; 47 PE-backed companies entered the market from 2013 to 2015, with 28 full or partial exits by GPs, and nearly half of these offerings occurred in 2014. In this case the surge had little to do with the government and more to do with the public markets investors, who were exercising caution in the wake of the global financial crisis, coupled with some underperforming PE-backed IPOs. The listing of Virtus Healthcare by Quadrant Private Equity in 2013 is considered the turning point when the public markets became comfortable with PE again.

"There was a real backlog of investments sitting in the portfolios of private equity firms," says KPMG's Willis. "Over the last two-and-a-half to three years, that backlog has dissipated, and a lot of PE funds have exited those investments in the Australian market through IPOs."

The pace seems to have slackened off a bit this year, with only four IPOs so far in 2016. Industry participants attribute this decrease partly to renewed wariness of PE-backed assets amid the continuing recriminations from the Dick Smith situation. Observers also note that GPs have already used up many of their IPO-worthy assets in the last few years and may be looking for new investments, making the slowdown more cyclical and less worrisome for potential PE sellers.

Moreover, IPOs are still seen as a good exit route, regardless of the current prejudices of investors. With large amounts of institutional money available due to the country's mandatory contribution superannuation fund scheme, interest in high-liquidity events such as public offerings will likely remain more very attractive to these investors. GPs must be on their guard in the short term, but must also keep in mind the likelihood that the current difficulties will not last.

"My view is that memories are short, and in two or three years, if there's not another Dick Smith the sensitivity to it will relax. But I do think at the moment it's front and center in the minds of investors and underwriters, and particularly if the sellers are PE funds," says Bruce Macdonald, a partner in the Australia office of Ashurst.

India has also seen its spikes; AVCJ Research shows 176 listings for the country, both onshore and offshore, since 2003, more than Australia's 151 but far behind China's 1,235. Its highest level of PE-backed IPOs occurred in 2007, with 31 - but following that the level dropped off again. Listings reached another peak in 2010 with 26, but began to pick up again, and 2015 and 2016 have so far seen 28 IPOs combined.

The recent rise in listings has made the capital markets attractive to Indian GPs, who point to the diversity of companies on public bourses as an indicator of the wide range of investment opportunities available. However, this diversity does not reflect the entire range of companies operating in India. The technology sector is generally underrepresented in the domestic market; one exception is IT security services provider Mphasis, which has been a public company since 1993 and was recently acquired by the Blackstone Group.

The relative lack of publicly listed tech companies is generally attributed to Indian investors' unfamiliarity with the sector. By traditional financial metrics many tech companies seem to underperform, leading to little interest from investors.

"People understand profits and revenue growth, but the metric for many of these new technology companies can be number of unique web users, number of repeat users or how long somebody spends on a web page," says Parag Saxena, co-founder and CEO of New Silk Route Advisors (NSR). "So the metrics are very different, and they're not financial. They may have very modest revenues, but still be very valuable companies."

An alternative route for tech companies is to list in an overseas market that might be more familiar with the appropriate performance measurements for a non-traditional enterprise, such as the NYSE or NASDAQ. Unlike in China, however, few PE-backed Indian companies have taken this path. Until this month travel company MakeMyTrip was the only example in the last 10 years. Solar panel player Azure Power recently broke the shutout when it raised $61.4 million in a NYSE listing; its backers include the International Finance Corporation, Helion Venture Partners, DEG and Foundation Capital.

US listings have historically been difficult for Indian companies, due to regulations requiring them to list domestically either before or at the same time as an offshore IPO. However, investors note that this requirement was recently removed; in time this might result in more companies following MakeMyTrip and Azure to the US. In addition, companies that are incorporated overseas - Flipkart is based in Singapore, for example - will have an easier time listing in foreign bourses and may pursue this option when the time comes.

Future prospects

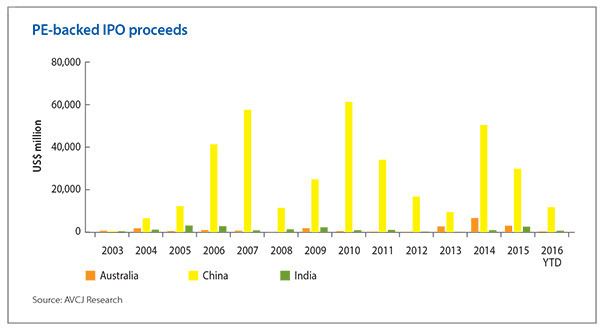

Despite the challenges associated with IPOs in each market, they continue to be an attractive exit avenue for Asian PE investors. One clear reason is the returns generated, which according to AVCJ Research total $20 billion since 2003 for Australia, $18 billion for India, and $371 billion for China - including both domestic and overseas IPOs by companies from these markets.

Observers in each market see interest as likely to continue; in India, for instance, investors at one time would have been alarmed at PE backers exiting a company during its IPO, taking it as a warning sign about the strength of the company. With more seasoning these investors have come to understand that a sell-down by PE backers is not necessarily related to the company's performance.

In Australia, despite the ongoing disputes over Dick Smith, observers do not foresee prolonged damage to prospects for PE-backed IPOs unless there is another such setback. As public markets become more familiar with the PE business model and better able to spot potential issues, the chances of such a blowup are considered likely to keep falling.

However, market participants also observe that Australia's current surge of IPOs is an aberration for a market that has traditionally been dominated by buyouts. While listings will no doubt continue, they are unlikely to reach the levels of recent years again unless the backlog that fueled this cycle occurs again - and that is unlikely without another catastrophe.

The trade sale route might be a good bet for the other markets as well. China still presents challenges going forward; the CSRC has placed previously announced plans to reform the approvals system on hold, and the focus on preventing volatility is expected to remain, and with it the occasional IPO suspensions. Companies with steady growth prospects are still considered likely to make it through the process and reap the benefits, but GPs have started looking to other routes to generate returns.

"We're beginning to see a lot of deals done on a trade sale basis, basically to try to sell the portfolio company to corporate players that want to expand their markets in China or position their strategy to have a presence in China through acquisition of PE portfolio companies," says KPMG's Gu.

India too is seen as a promising IPO market, due to the relative lack of regulatory issues and the dynamic capital markets - but here, as in China, GPs must be mindful of the type of company they are taking to market. Large, strong, well-established companies are considered the best bet for this type of exit; earlier stage enterprises would be better suited for other options.

"If you are doing a buy and build, or you're investing into earlier stage companies, or investing into businesses which are much smaller, then I do not think that it would be wise to bank on IPOs as the source of liquidity," says Padmanabh Sinha, managing partner for private equity at Tata Capital. "You'd have to look at either strategic or trade sales, secondary sales to private equity included, as the primary source of liquidity for such PE players."

More on Australasia

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.