Regulation: Dialogue in the dark

The Committee on Foreign Investment in the US has a huge a backlog of applications to process and a staffing shortage. Potential buyers have little choice but to be patient

For Canyon Bridge Capital Partners, the writing seemed to be on the wall. After nearly a year the China-based GP was no closer to completing its planned acquisition of NASDAQ-listed chip maker Lattice Semiconductor than when it started.

The problem was not with the company – it had agreed to a sale in November 2016 – but with the Committee on Foreign Investment in the US (CFIUS). The body responsible for reviewing the national security implications of proposed investments had subjected the deal to three 75-day review cycles before telling the parties there would be no endorsement. It cited concerns about the buyer's close ties to the Chinese government and the possibility of transferring intellectual property to China.

With its third attempt at negotiation stymied, Canyon Bridge took a gamble, going over the head of CFIUS and appealing directly to President Donald Trump for approval. But if the GP hoped that the famously independent-minded new leader would break with tradition once again by ruling against the committee's determination, they were disappointed by his decision last month to block the transaction.

"Obviously for the president, it's hard for him to go against the recommendation of CFIUS, especially with his rhetoric on China," says Daniel Dusek, a partner at Kirkland & Ellis. "So I think that was not the surprise – the surprise was that despite CFIUS' clear recommendation to the president to not approve the transaction, the parties didn't just pull it and terminate the agreement, and instead forced it to his desk."

The demise of the Lattice deal was a dramatic illustration of Chinese investors' growing frustration with CFIUS, whose increasingly slow processing pace has resulted in a backlog of cases. With the committee apparently more and more reluctant to approve deals, many buyers have begun to reconsider whether it is still worth the time to actively engage CFIUS.

While the alternative course of action – cutting the committee out of the loop – may save time, M&A specialists caution that investors should think carefully about their plans. Given the current political climate, an acquirer that seems to be trying to avoid regulatory scrutiny could invite much worse consequences than a delayed deal. CFIUS approval may have gotten more arduous, but investors will have to put up with the frustration for the time being.

Defensive action

Trump's decision to block the Lattice deal was not without precedent. Two of his predecessors had exercised the same power: Barack Obama twice issued orders involving overseas buyers in 2012 and 2016 respectively, while George H.W. Bush ordered the divestment of a US aerospace manufacturer in 1990. All three cases involved Chinese buyers or owners. The two under Obama were the divestment of wind farm assets near a US military facility by Ralls Corp. and the proposed takeover of a US-based subsidiary of Germany's Aixtron by Grand Chip, a German company with Chinese backers.

The rarity of such presidential interventions speaks to the normally smooth functioning of CFIUS, which was set up during the administration of Gerald Ford. The committee, which is composed of representatives from various cabinet level offices such as the Department of Homeland Security and the Department of State, encourages deal parties to bring cases on a voluntary basis, though it has the power to compel a review if it decides the parties have overlooked or withheld information on matters related to the national interest.

"The notion was that it doesn't cost that much in terms of time and money to file, and you could avoid the catastrophe of having the US government determine that there's a national security issue and the president order divestment," says Stephen Heifetz, a partner at Steptoe & Johnson who served on CFIUS between 2006-2010. "The incentives would be stacked in favor of filing."

Those incentives have been shaken in recent years with the expansion of CFIUS' caseload. According to the committee's most recent annual report, covering the 2015 calendar year, the number of cases it reviewed grew from 65 in 2009 to 143 in 2015. Separately the committee has reported that it received 172 filings last year.

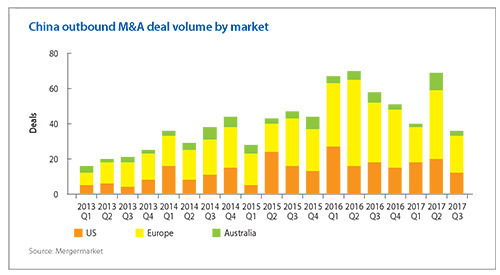

For the last several years, deals involving Chinese buyers made up the biggest share of transactions reviewed by CFIUS, accounting for 20% of total filings in 2015. Mergermarket data shows 58 M&A deals announced that year by Chinese groups. CFIUS specialists have noticed significant delays in receiving approval after the customary 30-day review period or receiving notification of an additional 45-day investigation.

While information on the inner workings of the committee is confidential, observers point to staffing as one obvious culprit for the slowdown. Many of the political appointees at the relevant agencies have yet to be named, a common complaint regarding the Trump administration. However, many buyers also suspect that the president's campaign rhetoric plays a role too.

"Currently we have a few deals where we're waiting for CFIUS clearance, but it is taking longer than usual – partly because of the change of government, but people do also believe that there is heightened scrutiny because Donald Trump and people in his government have been saying that they will particularly scrutinize Chinese investments in more sensitive sectors," says Judie Ng Shortell, a partner at Paul Weiss.

Such spotlighting of one country's deals would be considerably outside the norm. The majority of cases brought to CFIUS, no matter the nationality, result in approval, either as proposed or after negotiating mitigation measures to resolve any national security concerns. In 2015, the committee rejected just one notice outright, while only 13 cases were withdrawn from consideration by the deal parties, and nine of those were later refiled with mitigation measures.

Even if Chinese investors do not have to worry about heightened scrutiny, however, the fact of the CFIUS delay remains. While the customary advice for potential acquirers is to voluntarily engage with the regulator to show that they are operating in good faith and clear up any potential issues proactively, investors have begun to wonder whether the benefits of early filing are worth the increasing time commitments required to satisfy the committee.

In isolated cases, M&A advisors acknowledge, Chinese investors might get away with foregoing a CFIUS filing; such is the committee's current backlog that deals with limited national security exposure may go unremarked. But they caution that voluntary filing is still the best policy. Buyers that forego the voluntary process may still be called back by CFIUS to address issues in the deal, and may be forced to divest US interests post-closing. That is what happened to Ralls Corp.

Wider remit

Furthermore, even if target companies appear to have no national security relevance, CFIUS has significantly expanded its original remit. Where the committee's initial focus was on investments in defense, it now sees a much wider range of companies as falling under its purview.

"The CFIUS regulations don't expansively define national security or critical infrastructure – a great deal is left open to interpretation," says Joseph Falcone, a partner at Herbert Smith Freehills. "Obviously the traditional defense sectors will always be something that CFIUS examines, but beyond that you're seeing the committee closely examine other sectors, particularly telecom, IT, and even food and agriculture."

An example of the latter is Syngenta, the pesticide and seed developer acquired last year by China National Chemical Corporation (ChemChina) in a deal worth $43 billion. Though based in Switzerland, Syngenta's operations in the US prompted a CFIUS review to determine the merger's potential impact on the US food supply. The deal was approved last August.

Observers point to these situations as proof that even large Chinese acquisitions can make it past CFIUS. But navigating the process requires a knowledgeable advisor, ideally one who has served on the committee before. Such liaisons can provide essential points of contact with the relevant elected and appointed personnel.

"That is something that I think Chinese investors sometimes need a bit of education on, particularly those who are used to direct communication with the central government," says Paul Weiss' Shortell. "In places like the US, Australia, or Europe, the conveying of messages with these agencies are often done by lawyers. For state-owned Chinese investors that often comes as a bit of a surprise."

While observers are optimistic on the whole that CFIUS' current slowdown is only temporary, many admit to uncertainty on the future prospects of overseas investors in the US. Whether the current government will maintain the welcoming attitude of previous administrations remains to be seen.

"To be sure, CFIUS has viewed it as its role to protect national security, but ideally it wanted to be able to clear deals with necessary mitigation, operating against the background of an open investment policy," says Heifetz. "I think one thing that's different right now is that it's not clear that the Trump administration really is interested in maintaining an open investment policy."

SIDEBAR: Europe: The common front

The acquisition of German robotics company Kuka last year by Chinese home appliance maker Midea Group occurred over the vocal opposition of Sigmar Gabriel, Germany's economy minister. But Gabriel had no real power to stop the deal, absent a competing European bidder, and the EUR4.5 billion ($5 billion) purchase went through.

"I think to many people it was a great surprise," says Heiner Braun, a partner at Freshfields. "You would assume that when somebody so high up in the government comes out against a transaction they would have a means to block it, even if it is by phone to Beijing. But that didn't happen."

The proposed acquisition of computer chip maker Aixtron by a China-backed firm later the same year brought further embarrassment to Germany's regulators. The government had already given its approval to the deal, meaning that it did not endanger national security or public order. But in an unprecedented move it reopened the case after being notified by the US government that Aixtron's products were used in nuclear power plants.

In the end the deal was effectively blocked by US President Barack Obama's order that the acquisition of Aixtron's US subsidiary could not proceed. But the event indicated to many in Europe that a stronger regulatory approach was needed to protect against potential threats to national security.

A joint proposal by France, Italy and Germany before the European Commission would expand member countries' ability to block foreign acquisitions of companies handling sensitive national infrastructure. This would include traditional infrastructure such as the roadways and power grids, along with internet infrastructure, data security and critical intellectual property.

While this proposal, and similar measures in various countries, is in reaction to a wave of incoming Chinese investment, observers say China itself is not the target. Rather, policymakers' main concern is with preserving their domestic economies' ability to compete with companies from any country whose government privileges them over foreign rivals.

"The European market is still very foreign investor-friendly," says Christoph Louven, a partner in the Dusseldorf office of Hogan Lovells. "Most of the measures that have been introduced have nothing to do with Chinese investors as such, but have more to do with reciprocity, and how open the other country is to investment compared to Europe."

While the proposal before the commission is a step forward for regulatory unity, observers caution investors not to read too much into it. Nevertheless, moves like this may help to indicate where future developments lead.

"I'd be surprised to see a unified foreign investment review mechanism in the near future at the EU level, because that involves giving up a lot of sovereignty by member states," says Alexander Doorman, a partner in Freshfields' Amsterdam office. "The current proposal speaks much more of coordination, information provision and allowing member states to be informed of each other's processes. But definitely it is a change."

More on Greater China

Latest News

Asian GPs slow implementation of ESG policies - survey

Asia-based private equity firms are assigning more dedicated resources to environment, social, and governance (ESG) programmes, but policy changes have slowed in the past 12 months, in part due to concerns raised internally and by LPs, according to a...

Singapore fintech start-up LXA gets $10m seed round

New Enterprise Associates (NEA) has led a USD 10m seed round for Singapore’s LXA, a financial technology start-up launched by a former Asia senior executive at The Blackstone Group.

India's InCred announces $60m round, claims unicorn status

Indian non-bank lender InCred Financial Services said it has received INR 5bn (USD 60m) at a valuation of at least USD 1bn from unnamed investors including “a global private equity fund.”

Insight leads $50m round for Australia's Roller

Insight Partners has led a USD 50m round for Australia’s Roller, a venue management software provider specializing in family fun parks.